Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

While returns define a fund’s success, the structure that supports that return is equally important. The management fee, often viewed as a standard percentage of committed capital, is in fact central to the fund’s operational stability and long-term effectiveness. Read on this blog to know more.

Most private equity funds follow the traditional “2 and 20” model:

While the 20% carry rewards performance is paid, the 2% management fee is paid regardless of fund returns. However, the actual numbers often vary, some include:

Let’s clarify what is typically included under “fees”. Most LPAs outline a management fee to cover the fund’s operational costs, along with separate charges for additional expenses incurred in running the fund or executing investments.

Management Fee: The percentage charged annually on a specified base (committed capital, invested capital, or NAV). This goes to the GP to cover salaries, overhead, and investment operations.

Separate Expenses: Legal fees, audit fees, tax compliance, insurance, custodian fees, and fund administration. These are billed directly to the fund and passed through to LPs pro rata.

Transaction Fees: Sometimes the fund or the GP charges deal advisory fees, monitoring fees, or operational fees when investing or selling. These may be offset against management fees or charged separately.

The total LP cost is management fee + expenses + transaction fees.

Myth: Generally, management fees cover everything. False, expenses are separate and can be substantial. Management fees might be 2%, but total costs could be 2.5-3.5% depending on expenses. In essence, the management fee compensates the GP for its professional services, whereas expenses are reimbursements for actual costs incurred during the operation of the partnership.

This section highlights the common approaches for calculating and applying management fees.

A common structure in private equity and venture capital funds, where fees are calculated on the total capital committed by the limited partners, regardless of whether it’s fully deployed. This model applies mainly during the fund’s initial “investment period,” which provides the general partner with a steady income.

Consider a fund with $500M in committed capital charging a 2% annual management fee:

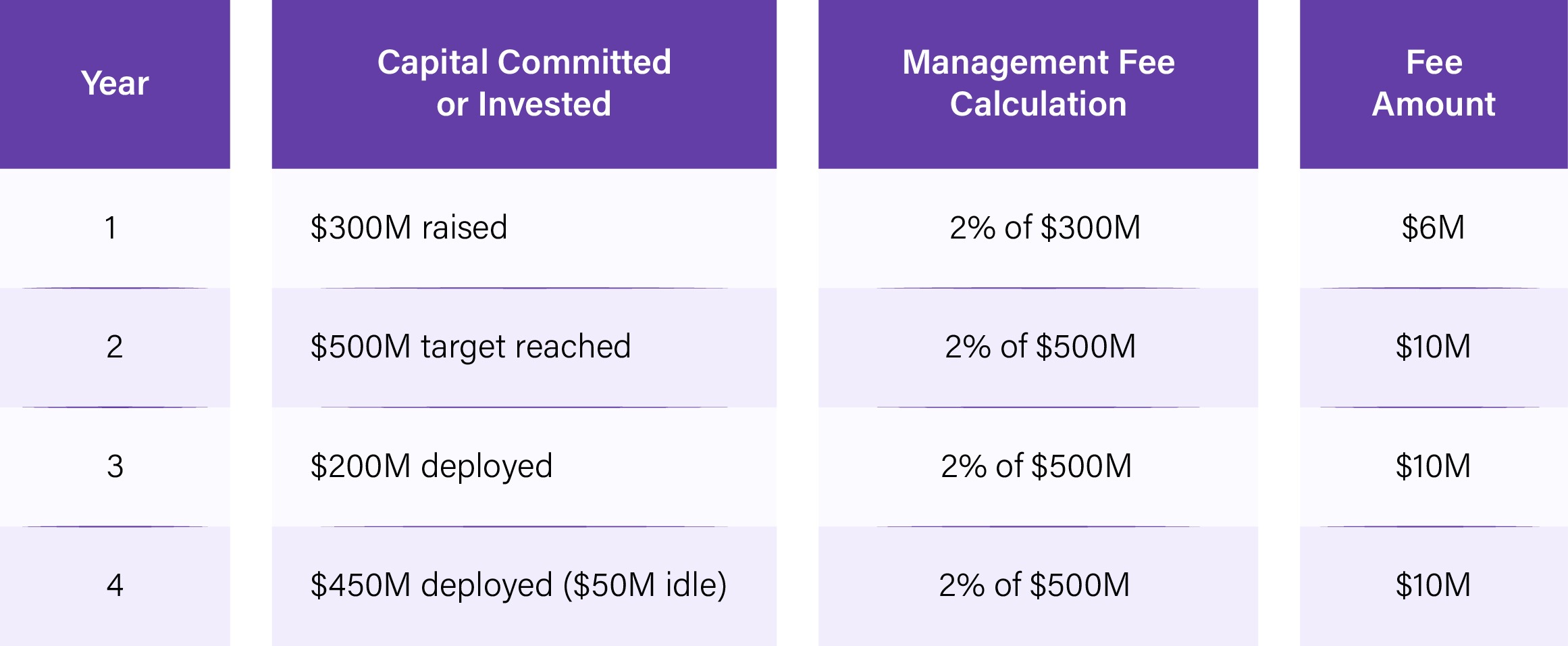

The invested Capital Model calculates management fees based solely on deployed and committed funds. Often starts by charging fees on committed capital during the early investment phase, then switches to invested capital after 4-5 years at a lower rate, typically 1-1.5%. This approach reduces fees over time and aligns costs with the money actively put to work, ensuring investors are not paying high fees on idle cash.

Example: Same $500M fund, 2% on invested capital.

Year 1: $200M is deployed. Fee = $4M.

Year 2: $350M deployed. Fee = $7M.

Year 3: $450M deployed. Fee = $9M.

Year 5: $450M deployed (no new capital deployed). Fee = $9M.

The hybrid fee model is designed for private equity, venture capital, or similar investment vehicles where investor capital is gradually deployed over time. Under this model:

Assume a fund with $100M committed capital, the fees for this are charged as below;

A NAV-based fee model is relatively uncommon in traditional private equity or venture capital. Under this structure, management fees are calculated based on the fund’s net asset value (NAV), rather than on committed or invested capital. The NAV is determined as the total value of the fund’s investments and cash, less any liabilities. In essence, it represents the current market value of the fund’s assets.

The Rule of Thumb for LPs: Committed capital during investment period, invested capital or step-down thereafter. If your LPA differs, understand why. There's usually a reason.

The fee step-down mechanism allows GPs to charge higher fees early and lower fees later. Such a structure exists because operations are expensive early (sourcing, due diligence, and deal closing) while portfolio management is relatively cheaper. Hence, it makes sense to taper down fees over time.

Typical structure:

Years 1-3 (Active investment): 2.0% on committed capital

Years 4-5 (Winding down investment): 1.75%

Years 6-7 (Portfolio management): 1.5%

Years 8-10 (Exiting): 1.0%

LPs should watch out for: Some funds specify the step-down in the LPA. Others leave it to "GP discretion." If it's discretionary, the GP might not actually step down if fund performance is weak. Hence, it is better to factor this in the LPA upfront.

This is where LPs lose money without realizing it. Your LPA says: "2% management fee." You think this covers everything, however it doesn't. Management fees cover GP salaries and basic overhead. But the fund also pays:

On a $100M fund, that's could potentially be an additional 1.3%-4% on top of the 2% management fee. Hence, your real cost is 3.3%-6%.

Are these expenses capped? Most LPAs say "reasonable expenses. However, some LPAs do cap expenses (e.g., "not to exceed 0.5% of AUM annually"). From an LP point of view, it’s better to agree on a cap to limit your expenses to a reasonable extent.

An offset is when the GP collects revenue from somewhere else and "offsets" it against management fees, reducing what LPs pay.

Common offsets:

How it works: GP collects a $1M advisory fee from a portfolio company. Instead of pocketing it, the GP applies 50% ($500K) against management fees. LPs pay less in management fees that quarter.

Why GPs do this: Shows alignment. GPs are sharing revenue with LPs and it is good optics at the annual meeting.

Why LPs should scrutinize this: The offset might be discretionary. The GP says "we'll offset 50%" but if fund performance is weak, they might offset only 25%. This could be a source of disputes.

A waiver is when the GP doesn't take the full management fee and instead converts it to a different form of compensation (usually carried interest or a profit allocation).

Example: GP is owed $10M in management fees for the year. Instead of taking $10M as cash income, the GP "waives" it and receives an additional $10M allocation of profits (if the fund succeeds).

Tax benefit: Management fees are ordinary income (taxed at marginal rate including self-employment tax). Profit allocations are capital gains. By converting fees to profits, the GP saves ~17% in taxes.

Why GPs do this: Tax optimization. If a GP can waive $10M in fees and receive it as a profit's allocation, they save $1.7M in taxes.

Why LPs should care: Technically, a waiver should align GP and LP interests (GP gets paid only if fund succeeds). But the waiver has to have real entrepreneurial risk. If a waiver is structured poorly, the IRS might recharacterize it as ordinary income, destroying the tax benefit.

For a waiver to be valid under IRS rules:

Most fund counsel structures waivers carefully to meet these criteria. But some don't. If you see a waiver in your LPA and you're the GP, make sure your tax counsel signed off.

Some funds offer reduced management fees for LPs who commit early.

Example: First $100M committed = 1.8% fee. Next $200M = 2% fee. After $300M = 2.2%.

This incentivizes early commitments and helps GPs reach "first close" faster.

For LPs: If you're a large investor with leverage, you can negotiate a custom fee rate. Some funds give 10-50 bps discounts for strategic LPs.

These fees are often embedded in the transaction itself, making them less visible to limited partners (LPs), who focus on reported fund returns.

Transaction fees are charges levied when the fund invests in or exits from deals. Common transaction fees:

These fees often don't get offset against management fees. They're pure GP profit. And they dilute LP returns.

Example: A $500M PE fund invests $100M in a platform company. The GP charges a 1% sourcing fee ($1M) + 1% annual monitoring fee ($1M/year for 5 years = $5M). Total extra GP take: $6M.

If the investment returns 4x, the PE fund gross profits are $300M. The GP's carry on that $300M is $60M (20%). But the GP also got $6M in transaction fees. Total GP take: $66M.

The LPs' net return is reduced by $6M because of transaction fees. That's material.

Here’s the comparison on fee norms between three different asset classes.

In some cases, funds price themselves into a corner.

A $50M seed fund charges 2% management fee = $1M annually. But the GP team is 3 people, rent is $300K/year, and they need $500K for operations leaving very little for GPs as compensation.

Most seed funds accept this and GPs accept that their carry is the real compensation. In some cases where they can negotiate, they raise a higher fee (2.5% or more) to justify the fixed costs.

A $500M buyout fund commits to 1.75% management fee = $8.75M annually. The management company (the entity receiving fees) employs 50 people with $6M in salaries. Plus $1.5M in overhead. Total: $7.5M needed. That leaves $1.25M for debt service, reinvestment, and distributions. It's tight. If a deal falls through and capital calls slow, the fund burns through the margin.

Result: Either the fund doesn't hold together, or the GP quietly increases fees or charges transaction fees to plug the gap.

A fund charges 1.5% management fee (below market). The GP is betting on high carry returns to make up for the lower fees. But if the fund underperforms (2x instead of 4x), the GP's total compensation is underwater. This creates perverse incentives. The GP might take excessive risk, or delay exits, or hold onto losers too long because they need the carry.

If you're a GP building a fund, here are the mistakes that destroy relationships:

Your LPA says "2% of committed capital" but doesn't define what counts as committed. Does co-investor capital count? Does GP capital count at full value or discounted value?

Result: Year 1 close. You have $300M from LPs and $5M from the GP. Is the base $305M or $300M? Your LPs think it's $300M. You think it's $305M. Now you've overcharged by $100K.

Fix: Define the base in crystal clear terms. Include GP capital or don't. Make it binary.

Your LPA says "the fund will reimburse reasonable expenses" but doesn't cap them. By year 3, you've run up $2M in expenses (including $500K for an offshore administrator). Your LPs are upset.

Fix: Cap expenses. Say "not to exceed 0.75% of committed capital annually" or "not to exceed $750K." This protects both you and the LPs.

Your LPA says "management fees may be stepped down" after the investment period. Your LPs assume they will be. In year 7, you haven't stepped down because you're still managing 50 companies. Your LPs are angry.

Fix: Either commit to a step-down schedule ("fees will be reduced to 1.5% in year 6") or explicitly reserve the right to maintain fees and explain why.

You charge 1% sourcing fees on deals but don't mention it in the fee summary. Year 1, you deploy $100M and collect $1M in sourcing fees. Your LPs see this in the K-1 and feel blindsided.

Fix: Disclose transaction fees upfront in the PPM. Explain the amounts, the method, and how they'll be offset (if at all).

You want to waive management fees to optimize taxes. You set it up without consulting counsel. The IRS later recharacterizes it as ordinary income. Now you owe back taxes plus penalties.

Fix: Have counsel review any fee waiver structure. Make sure it meets IRS requirements for "profits interests." Cost: $5K-$10K. Penalty if done wrong: $100K+.

If you're an LP evaluating a fund, here's the fee interrogation:

1. What is the management fee percentage, and on what base?

Get the exact number and the exact base (committed capital, invested capital, NAV, etc.).

2. When does the management fee step down?

Is there a schedule? Is it mandatory or discretionary? By how much?

3. What expenses are the fund's responsibility?

Audit, legal, fund admin, insurance, travel: understand what's included? What's capped?

4. What transaction fees does the fund charge?

Sourcing, monitoring, advisory: what are the rates? Are they offset against management fees?

5. Is there a fee cap or expense cap?

What's the maximum the fund can charge in total?

6. Are there any fee offsets?

If the fund collects advisory fees, how much is offset against management fees?

7. Is there a management fee waiver?

If yes, what's the structure? Has counsel signed off?

8. How do fees apply to co-invest vehicles and SPVs?

If you're co-investing through an SPV, what fees apply? Sometimes SPVs have 0% management fees.

9. What happens if the fund doesn't deploy capital?

If only $300M of $500M is deployed, does the GP still charge 2% on $500M? (Usually yes, but confirm.)

10. Can I negotiate a discount?

If you're a large investor, what's the GP's appetite for fee reduction? Some offer 10-50 bps discounts for strategic LPs.

The best GPs are now using tools to make fees transparent. Fund portals now let LPs see:

Transparency reduces disputes. If LPs can see the fee calculation and it matches the LPA, there's less friction. If the calculation doesn't match, they catch it immediately. More GPs are publishing "fee breakdowns" in quarterly reports. This builds trust. And trust is expensive to rebuild if destroyed over fees.

Management fees are the often-misunderstood cost of private investing. They're not negotiable after close. They're not optional. And they're not always what they appear to be in the headline.

The GPs who succeed at fee alignment are transparent, publish their calculations, and many times are ok to cap expenses. They also offset revenue and step-down fees when appropriate to build LP trust. LPs seek to protect themselves and hence scrutinize fees upfront, calculate the real total cost (management fe,e + expenses + transaction fees + carry), and negotiate where they have leverage.

And both understand that fees aren't the enemy of returns. They're the infrastructure that enables returns. But infrastructure should be lean, efficient, and honest. Get the fees right, and everything else becomes easier.

Rarely. Your LPA is locked at closing. However, some LPs with leverage have negotiated custom "side letter" rates where they pay a lower fee than other LPs in the same fund. This is rare but happens with anchor LPs or strategic investors.

No. A waiver is permanent (unless the LPA allows reversion in specific circumstances). The GP voluntarily forgoes the fee. In return, they typically receive a higher allocation of profits. The economics are meant to align GP and LP interests.

No. The waterfall specifies that management fees come first, then carried interest. Once you've paid management fees, the carry is on profits (not total proceeds).

Generally no. Management fees are considered investment expenses, which are subject to the "2% haircut" under IRS rules (they're deductible only to the extent they exceed 2% of your AGI, and the tax law has limited their deductibility in recent years). For most LPs, management fees are not deductible. Consult your tax advisor.

No. Management fees are independent of performance (unless the LPA has a performance adjustment clause, which is rare). Whether the fund returns 2x or 0.5x, management fees are the same. This is why some sophisticated LPs negotiate performance-based fee reductions in mega-funds with significant leverage and deal activity.

Yes, but it's rare. Some mega-funds with strong track records have negotiated performance-based fee adjustments. Example: If the fund returns less than 1.5x by year 5, the management fee drops to 1%. This aligns GP and LP interests more tightly.

Typically yes, but at different rates. The main fund charges you 2% management fee. The SPV might charge 0-1% (much lower). This is disclosed upfront. Some LPs negotiate a "blended" fee cap across all vehicles to avoid doubling-up.

Depends. A $500M fund at 2% = $10M annually. Maybe $7-8M covers salaries, rent, and ops. The remaining $2-3M is profit to the management company (often distributed to GP partners). This varies widely based on the firm's structure and scale.