Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Every private equity fund awaits the moment when one of their investments sees exits. It could be in the form of an acquisition, a secondary deal or the company going public. Suddenly, there's cash realized on the table, yet to be allocated back to the fund’s stakeholders. It belongs to a mix of investors and managers, in proportions that are governed by the fund agreements. The question that follows is deceptively simple: Who gets paid first? This is where the waterfall comes in.

A waterfall isn't just plumbing; it's the core of your fund’s incentive design. It determines whether your GP will hunt for 2x returns or coast after 1.5x. Whether early winners or late bloomers will trigger disputes.

Waterfalls usually take two fundamentally different shapes: American and European. Read along to understand how waterfalls work, the pros and cons of each waterfall method, and the profit split between LPs and GPs.

Before we talk waterfalls, we need to talk incentives.

Limited partners write cheques. Their job is to contribute capital and wait to reap the returns. General partners manage the capital. Their job is to maximize returns. But GPs also need to pay staff, cover office rent, and eventually make their own profit. This creates immediate tension.:

LPs want to maximize their returns. They want their capital back first. They want a baseline return (the "hurdle" or "preferred return") before anyone celebrates. Only after LPs have made their money, GPs get a chance to participate in the profits.

GPs want to get paid for their work. They want to see profits sooner rather than later, especially important for emerging managers who don't have big balance sheets They want to be especially important for emerging managers who don't have big balance sheets. rewarded for successful exits, even if the overall fund isn't doing well yet. They want enough carry to fund the team.

These two viewpoints are not compatible. A waterfall is the compromise, i.e. a formula that tries to satisfy both. But the shape of that formula reveals everything about the relationship.

A distribution waterfall is a predetermined order for allocating fund proceeds between LPs and GPs. The term “waterfall” comes from the way money moves through each layer, one must be filled before the next gets anything.

In most cases, a waterfall has four tiers:

LPs get their original investment back first, dollar by dollar. For example, if a fund invested $100 million, LPs must receive $100 million before anyone else gets paid.

LPs receive an agreed return on that capital. Typical rates to be paid are 6%, 8%, or 12% annually, depending on risk and asset class. This is usually cumulative, i.e., if you have invested for 5 years and didn't get your annual preferred return, it compounds until it is received back.

Once LPs have their capital plus preferred return, GPs get an "accelerated" slice of profits until they reach their agreed carry percentage. This gets complex quickly.

Everything remaining is split between LPs and GPs according to the agreed ratio (typically 80/20, meaning LPs remaining profits).

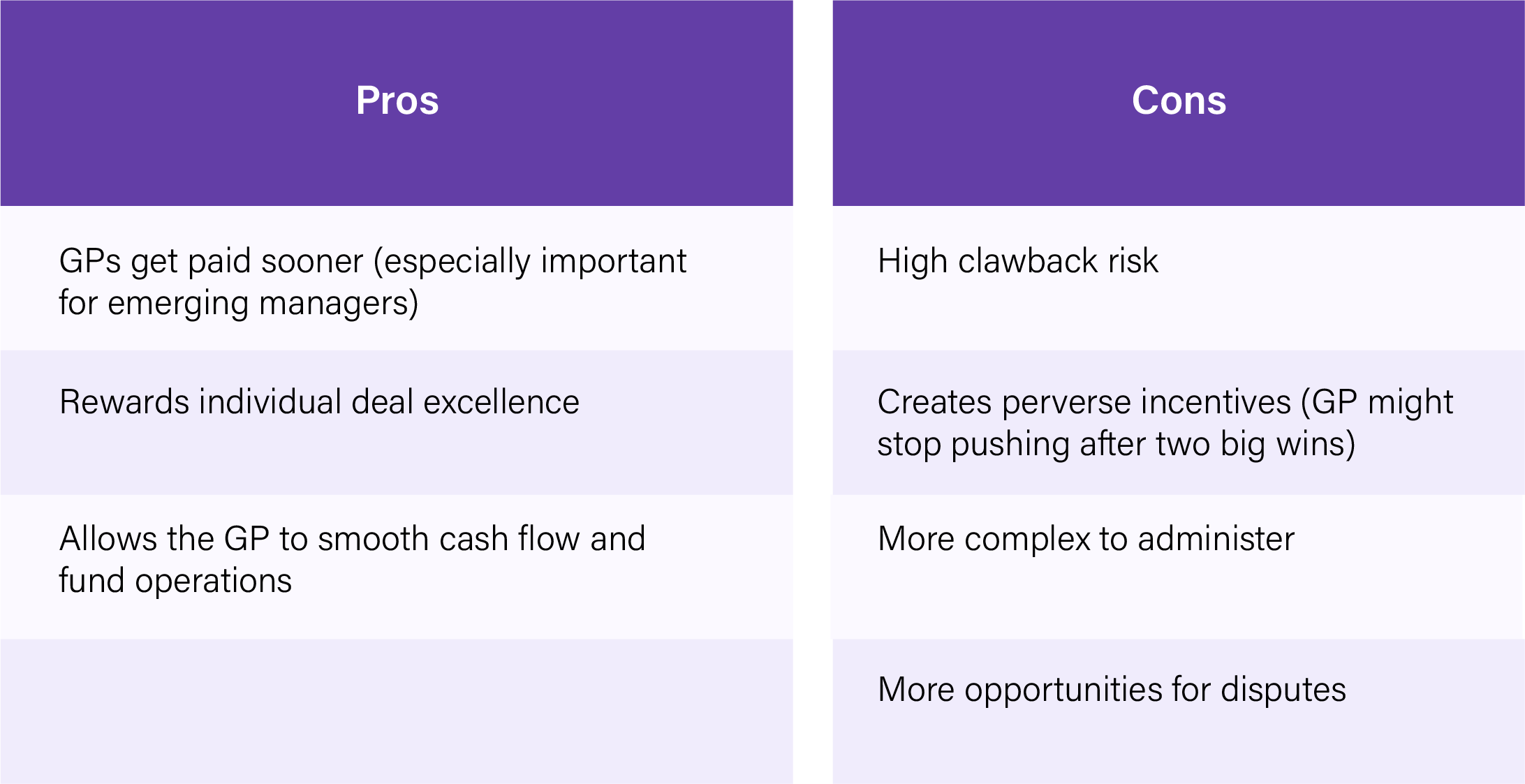

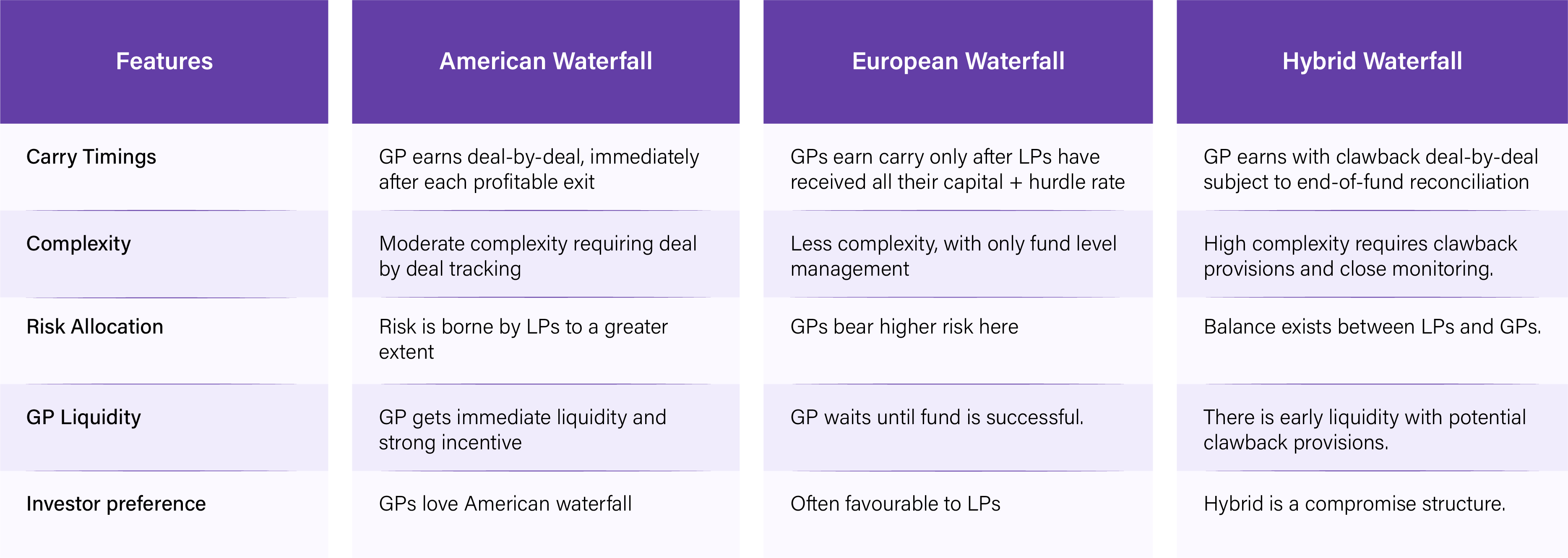

American Waterfall: Deal-by-Deal Reality

The American waterfall is the "deal-by-deal" model, making the GP's job easier. This schedule is beneficial to the general partners of the fund, as it diversifies the risk across several deals. GPs receive carried interest before Limited Partners receive their initial investment.

An important feature included under the ‘American Waterfall’ is the clawback provision. A clawback provision includes is an obligation of the General Partner to return the carried interest previously distributed to the Limited Partners making sure that throughout the fund life, the LPs get paid according to the predetermined profit-sharing ratio.

Here's how it works: every time the fund exits an investment, the four tiers apply immediately.

Example: A $100M fund exits Deal #1 for $160M in proceeds

The GP just earned $21.6M on a single deal. They can show this to their team. They can use it to cover overhead. They can feel good about the exit.

But here's the trap: The fund isn't done yet.

The fund invested $100M total. Deal #1 was $70M. Deal #2 is still worth maybe $40M on the books. But what if Deal #2 underperforms? What if it gets written to zero? What if by year 10, when the fund is winding down, the final tally shows:

But LPs only received $138.4M from Deal #1, plus whatever they get from the remaining deals. They're short. They never made their hurdle rate across the fund.

The GP, however, already took $21.6M in carry from Deal #1. This is when clawback comes in.

The American model puts GPs at risk. If they take carry too early, they may have to give it back. This is why clawback provisions are essential in American waterfalls and why they're so painful when triggered.

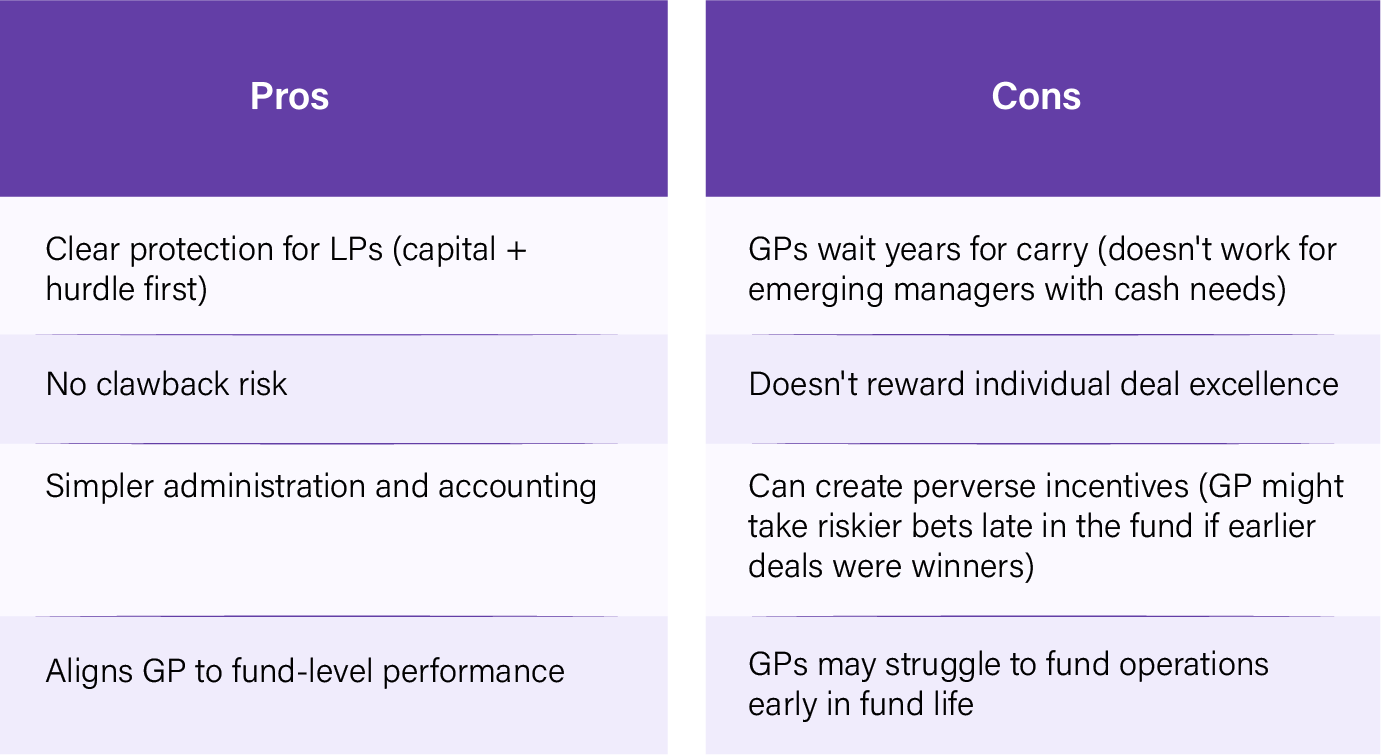

Under the European waterfall model, LPs are prioritized over GPs’ carried interest; it applies to all four tiers once, at the end of the fund's life, when the entire fund is liquidated. The European waterfall is a standard model for large buyouts and M&A, ensuring that GPs do not earn when the overall fund is underwater.

Instead of asking "Did Deal #1 make its hurdle?" you ask "Did the fund as a whole make its hurdle?"

Same example, but European model:

The fund invests $100M total, exits everything over 7-10 years, and realizes $190M total.

Notice: Under the European model, the GP earned only $2M. Compare that to the American model, where they earned $21.6M. This is why GPs usually hate the European model.

But also notice: There's no clawback risk. The GP doesn't get paid until the whole fund is done. They don't have to give money back. The administration is simpler. The risk to LPs is much clearer.

By now you understand what the American and European waterfall is, their pros and cons. Hybrid waterfall is the middle ground of both these waterfall models, where the GP can receive the carried interest but also includes and safeguards to protect limited partners (LPs).

Here’s how the hybrid waterfall works:

Soon after a single deal exits, the GPs can receive the carried interest sooner. In most cases, GPs receive their carry soon after the hurdles are met on individual deals. However, if certain deals underperform later, the general partners should return the same carry to provide the agreed return to the LPs.

Preferred return, often called the “hurdle rate,” is the return LPs should receive before any GP carry kicks in. Hurdle rate shapes the entire fund’s economics, so this is critical.

Common preferred return rates in the industry:

Here's the critical detail that most LPs miss:

Does the preferred return reset on each new close?

Imagine a fund has two closings:

In year 4, the fund exits a deal, and the second-close limited partners are late to catch up, as they invested only for 3 years, not 4. This is where equalization comes in. Note: Remember to ask whether your preferred return resets, as this will significantly change your actual return.

The catch-up is one of the most misunderstood parts of waterfalls. Catchup tranche exists to make sure that the GP receives a large share of profits after LPs get their preferred rate. This rate allows general partners to catch up on the promised carried interest before sharing the profit, as per the agreed LPA.

This is how the catch-up tranche works. Imagine a fund having 20% carry. A GP will not participate in any profits until the entire preferred return is paid, in case of no catch-up. However, when the profits start flowing, the GP should jump to 20% than slowly ramp up.

The catch-up is the mechanism that makes this happen.

Simple numerical example:

Assume:

In Year 5, if a deal exits with $200M proceeds. The calculations are:

Now, without a catch-up: If the GP gets 20% of the remaining $60M, they'd get $12M. But what if there's an earlier deal that didn't make its hurdle? The GP shouldn't get carry on that one at all.

With a catch-up: The GP gets accelerated distributions until they reach 20% of total profits across all deals so far. This protects the LP if early deals underperformed.

The catch-up can be:

Most funds use 100% catch-up. This is the negotiation point between LPs and GPs.

After paying the hurdle and catch-up tranche, the leftover amount is supposed to be split between the limited partners and general partners; this split is usually 80:20. This portion of the profit that the GP receives is called the ‘carried interest’.

A clawback provision allows limited partners to recover carried interest if the fund is underwater. It is the safety net for the American Waterfalls.

Here’s how the clawback provision works:

After the fund pulls the plug, the final books of account are closed. If the total return on the fund to the LPs falls short,

The total fund returns falls short of the LP's preferred return, so the GP has to return some or all the carried interest they’ve received earlier.

Real example:

A $500M fund exits Deal #1 for a big win in Year 3. The GP takes $50M in carry (20% of $250M profit, simplified). Their team celebrates. Half gets distributed. Half gets put in escrow.

By Year 8, the remaining deals underperform. The fund's total return: $600M on $500M invested. That's 3.6x gross, roughly 12% IRR, which misses the 20% IRR hurdle the LP expected.

At closeout, the accounting shows: LPs are entitled to $250M more than they received. The GP's carry of $50M is clawed back (or partially clawed back). This is brutal.

This is why clawback provisions are contentious. GPs argue they should only claw back realized proceeds (not paper losses). LPs argue all underperformance should trigger clawback. Most disputes happen here that often lead to litigation.

In practice, waterfalls get messy. Here are the complications that actually cause problems:

Some funds allow GPs to recycle distributions i.e., take distributed carry and reinvest it in the fund at reduced fees. This creates a secondary waterfall within the waterfall.

When a main fund and an SPV co-invest in the same deal, how do waterfalls cascade? Each vehicle has its own waterfall, but the underlying asset only exits once. This creates reconciliation nightmares.

An anchor LP negotiates a custom carry percentage or preferred return. Now you have two sets of economics. When does one apply vs the other? The LPA usually loses.

Most LPAs require GPs to commit capital (usually 1-5% of the fund). If the fund tanks, the GP loses money too. But when does the GP's capital enter the waterfall? Before other LPs or after? This affects returns dramatically.

If a fund has multiple closes, does the preferred return reset for late-closing LPs? If not, they have a compounding disadvantage. This is where equalization comes in.

When does clawback actually happen? At fund termination? Or can it be triggered mid-fund if performance dips? The LPA language is critical here. Bad wording leads to disputes about whether clawback is even owed.

If you're an LP signing into a fund, don't skip the waterfall section. Here are 10 questions to ask:

1. Is this American or European waterfall?

Know which model applies. It determines carry timing and clawback risk.

2. What is the preferred return percentage?

6%, 8%, 12%? And does it reset on subsequent closes or compound continuously?

3. When does preferred return stop accruing?

Some LPAs cap preferred return at a certain point. Others let it compound indefinitely. This affects your base return significantly.

4. What is the GP carry percentage?

20% is the standard, but verify that it doesn't have side letter exceptions that get hidden.

5. Is there a catch-up? And is it 50% or 100%?

This determines how aggressively the GP participates in early profits. Crucial to understand this number.

6. Is the catch-up realized or "soft"?

Some LPAs make catch-up contingent on the fund making its overall hurdle. Others don't.

7. What is the clawback trigger?

Understand if clawback apply realized proceeds or does mark downs count as well. Make sure to check if, it applies mid-fund or only at the termination.

8. Is there an escrow mechanism for carry?

Ensure you know how much of carry is held back? and for how long. This determines clawback risk.

9. How do subsequent closes affect the waterfall?

Look for equalization adjustments and its rate, make sure if it applies on late-closing LPs. This is where the fund accounting gets complex.

10. Are there any exceptions in side letters?

Don't assume the LPA is the final word. Ask if any GP-LP side letters modify the waterfall. This is where surprises hide.

A waterfall looks simple on the surface. It's just a distribution formula. But in practice, it embodies a fundamental negotiation about trust, risk, and incentives.

The American waterfall says: "I trust you to manage yourself. Take your carry when you earn it. But if it doesn't work out, you'll pay it back."

The European waterfall says: "I'll trust you, but not until I've made my money. Then you can participate in the upside."

Most funds land somewhere in the middle, with escrows and side letters and catch-up provisions that muddy the line.

The takeaway: Don't ignore your fund's waterfall. It shapes your actual returns more than most GPs realize. Read it. Understand it. Question it. Because a waterfall designed poorly doesn't just confuse accounting, it also misaligns incentives for a decade and often costs real money.

Because they get paid sooner. In an American waterfall, a GP can see carry distributions within 3-5 years. In a European waterfall, they often wait 7-10 years. For emerging managers, this is existential as they need cash to fund operations and prove themselves for Fund II.

An escrow is money held back from carry distributions. Typical escrow: 30-50% of carry is held. At fund termination, if clawback is triggered, the escrow is used first. The remaining carry is typically not clawed back. This reduces clawback litigation risk.

Yes, unless there's equalization. Late LPs didn't invest during early deals that may have already appreciated. Equalization charges late LPs an "interest" payment (usually 8-12% annualized) to make them whole. But this is often disputed.

In theory, no. LPs won't sign without clawback. But in practice, the structure of clawback (what gets clawed back, what stays in escrow, timing of clawback) is heavily negotiated.

This is the real risk. If a GP has already distributed carry to partners, and then clawback is triggered, the GP needs to have cash or capital available. Some LPAs require GPs to post a performance bond or maintain capital reserves for this reason. In practice, if the GP can't pay, litigation often follows.

Yes. The structure of the waterfall affects when income is recognized for tax purposes. Carried interest has different tax treatment than return of capital. GPs should consult tax counsel. And clawback creates basis adjustments that complicate later distributions.

It doesn't. The preferred return is contractual and fixed. If you agreed to 8% and inflation spikes, you still get 8%. This is why some institutional LPs negotiate for inflation-adjusted hurdles in high-inflation environments.

Critical. The fund administrator calculates the waterfall. They track catch-up across deals. They monitor clawback risk. They produce K-1 forms that reflect waterfall allocations. Bad admin work leads to incorrect distributions and LP disputes.

Generally, no. The waterfall is locked at closing. But if a side letter exists, it might have provisions for renegotiation under specific conditions (e.g., if fund performance hits certain milestones). Otherwise, you're locked in.