Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

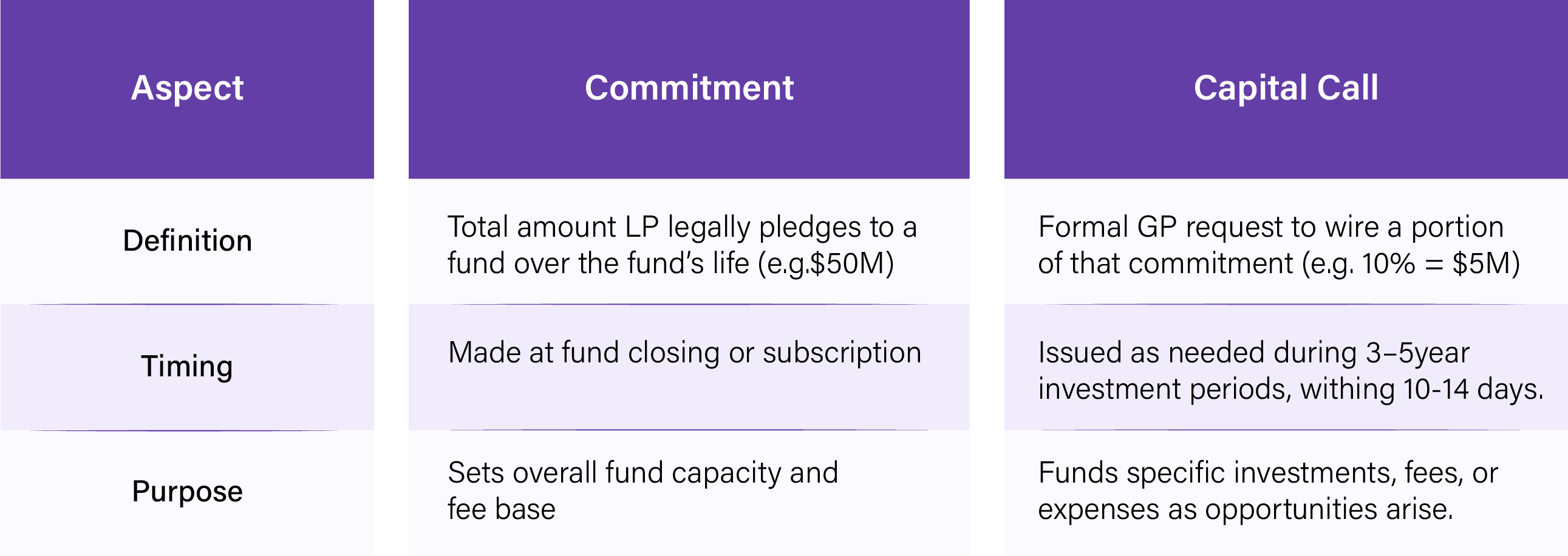

Every limited partner relationship starts the same way: you commit to a fund. Say $50 million. You confirm it to your GP, sign a Limited Partnership Agreement, and... wait. That commitment isn't deployed immediately. In fact, capital is called during the investment period as and when the fund requires it for investments, management fees, and fund expenses.

A capital call notice is a formal communication from the General Partner (GP) to Limited Partners (LPs), requesting that they transfer a specified portion of their committed capital to the fund. They send a notice: "We need $X million from you, by [date]."

Before moving further with Capital calls, it is crucial to understand the distinction between your commitment and the capital calls. This is the first thing that confuses new LPs.

The distinction matters because:

Let's look at how a capital call flows.

A fund's General Partner (GP) evaluates available cash against upcoming investments and determines how much capital to request from Limited Partners (LPs).

Maybe they've identified a deal they want to invest $100M in, and they have $40M cash in hand. They need $60M more. So, they calculate how much to call from LPs.

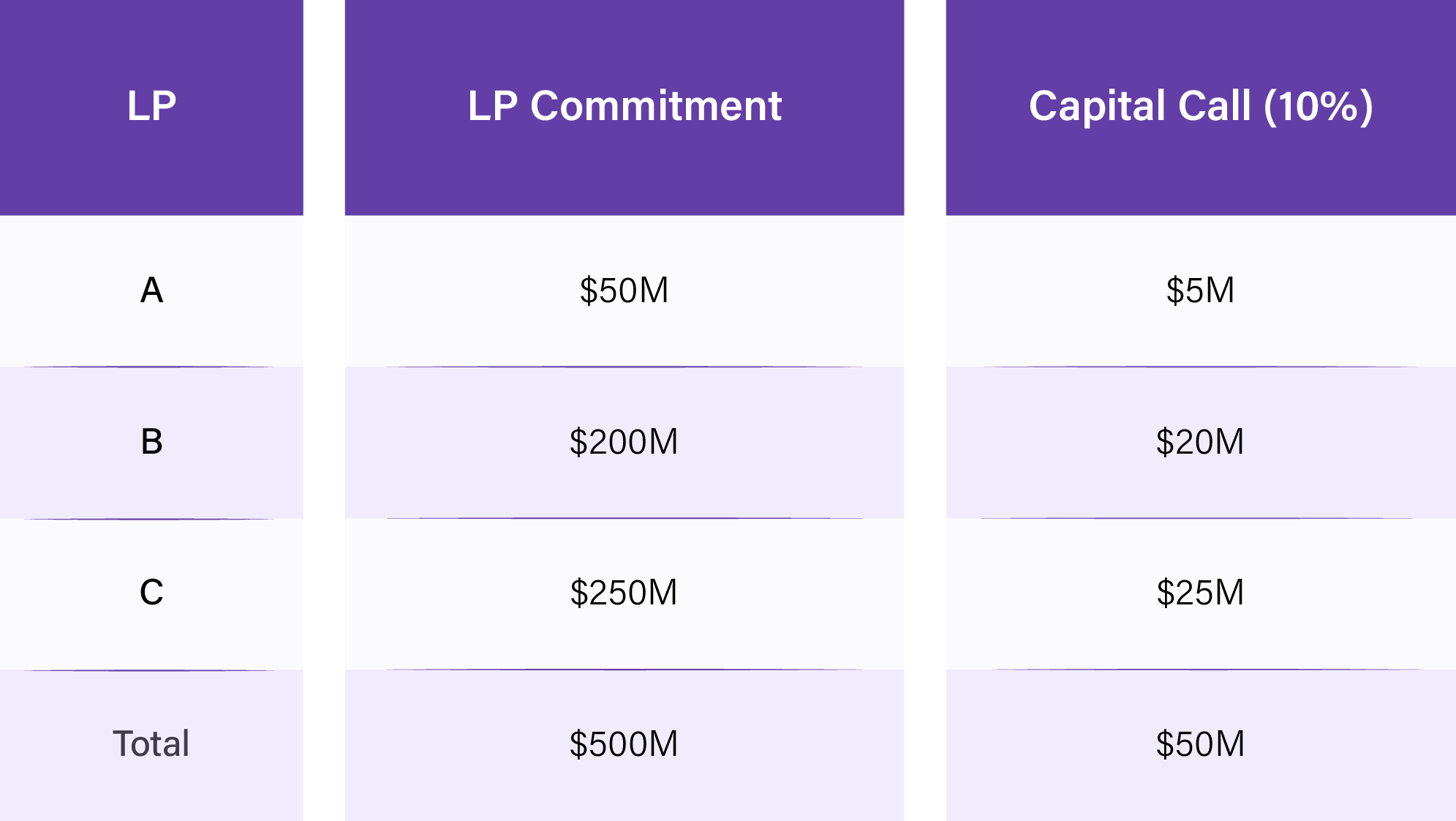

If the fund has $500M committed capital, and they need $60M, that's 12% of the fund. Each LP gets called for 12% of their individual commitment.

If you committed $50M, you get called for $6M (12% × $50M).

Other triggers for capital calls:

The capital call notice needs to be precise. It typically includes:

The ILPA (Institutional Limited Partners Association) has published templates for capital call notices. Most sophisticated GPs use these templates, which reduces errors and confusion.

Once the GP sends notice via fund portal or mail, it is the LP's responsibility to review it before wiring the funds.

Here’s what to inspect:

Now your team needs to get a $6M in cash to your GP. Ensure that sufficient liquidity is available to meet the capital call obligation in a timely manner. If necessary, the LP may:

Some GPs use "capital call lines," a short-term credit facility that help them bridge capital calls. This solves the liquidity timing issue by deferring calls to LPs. LPs can use “LP financing” later, which is rare and distinct.

This is the moment. You wired $6M to the GP's designated account. It is a crucial step; being extremely careful with all the details is necessary.

Common Pitfalls:

Modern fund administrators now use automated portals that allow LPs to wire funds directly, reducing manual errors. Qapita is one such portal that provides a seamless experience for your fund management.

The GP receives the wire. The fund administrator reconciles the payment against the capital call notice. Once everything matches, they send a confirmation to the LP: "We received your $6M capital call payment on [date]."

Now the fund has the cash and can deploy it.

Everything about capital calls is governed by the Limited Partnership Agreement.

Your LPA spells out:

The GP's right to call capital:

Your (the LP's) obligations:

Default consequences:

A side letter is a separate legally binding agreement between the fund (or GP) and a specific investor that modifies or supplements the terms of the LPA as they apply to that investor.

It is important to note that:

Common provisions in Side Letters:

The GP needs to decide: how much to call, and from whom? Here’s the simplified process:

Fund committed capital: $500M, 10% of the fund is needed, i.e. $50M.

Each LP pays their share based on the total commitment, this is fair and standard across the industry.

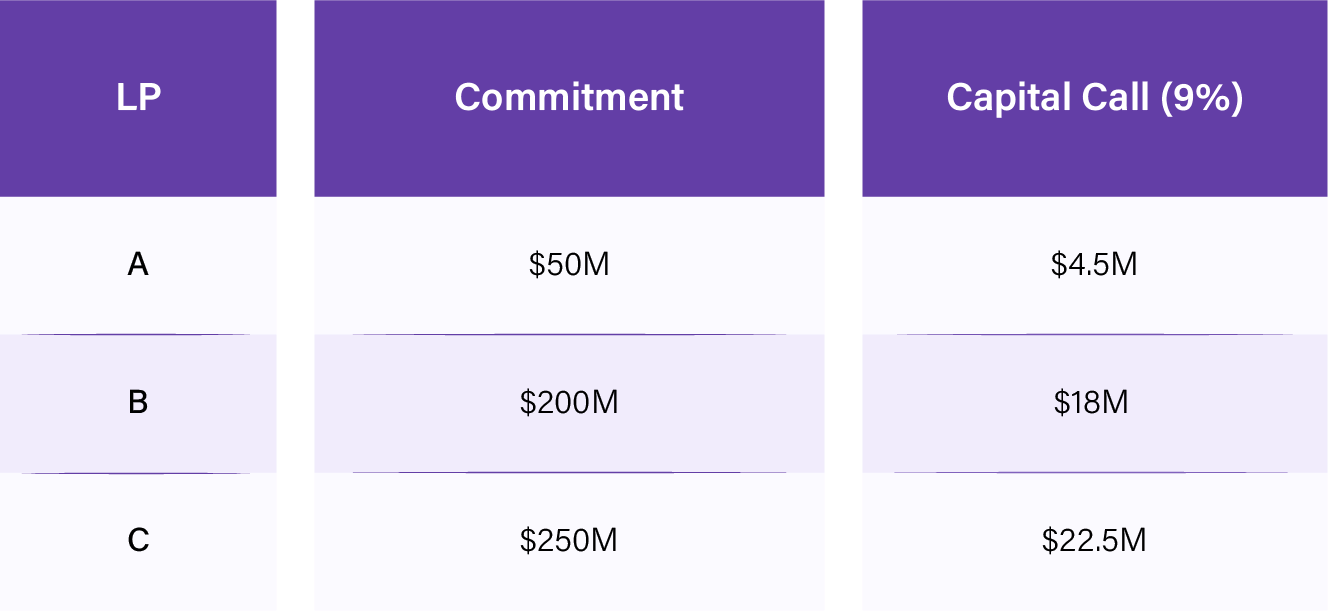

Let’s take the same fund and say this time it needs $40M in investment and owes $5M management fees for the year. The total need is $45M, which is 9% of the fund.

The fees will be allocated on a pro-rata basis; no separate notices will be sent.

Imagine an LP (investor A) is part of two investment vehicles:

Main fund: $400M total commitments, this deal requires $80M.

SPV (Special purpose vehicle): $100M total commitments, this deal requires $20M.

How capital calls work:

Main fund: $40M which is 10% of $400M

SPV: $10M which is 10% of $100M

Many private equity funds raise capital in multiple closings over time. Early investors fund deals and begin earning returns, while later investors join after some capital has already been deployed. This timing difference can create inequity, since late investors did not participate in earlier investments.

Equalization is the mechanism used to ensure fairness. It adjusts the capital contributions of late investors, so they are treated as if they had been part of the fund from the beginning. This includes:

Through equalization, all investors regardless of when they joined receive proportional returns, and early investors are compensated for deploying their capital sooner. In essence, equalization maintains equity, transparency and consistency across multiple fund closings, preventing disputes and ensuring all investors are treated fairly.

This is complex and is a major source of disputes. Fund administrators spend a lot of time getting equalization calculations right. Even small errors (wrong interest rate, wrong dates) lead to LP complaints.

If you're a global LP investing in a US dollar-denominated fund, you face FX risk on capital calls.

Scenario: You're a UK pension fund. You committed £50M to a US fund. The fund makes a capital call in USD: $6M.

When you need to convert £50M to USD to fund this call, the exchange rate might have moved. If GBP has weakened against USD, you now need more GBP to buy the same $6M. This effectively increases your capital call costs.

Additionally:

Most global funds ask LPs to fund from USD accounts directly (if they have them) to avoid FX friction. The LPA might even specify that "capital calls are due in USD, and all FX conversion costs are borne by the LP."

Despite best intentions, capital calls frequently go sideways.

Issue 1: Email lands in spam

The capital call notice is marked as spam because the GP's email domain isn't configured properly. The LP doesn't see it. By the time they notice, the deadline has passed.

Fix: GPs should use confirmed, whitelisted email addresses. LPs should add the GP's email to their contacts. Both should use portals, not email.

Issue 2: Wrong wire instructions

The LP copies the bank account number from the email. But there's a typo, a missing digit, or a wrong digit. The money goes to the wrong account. Now the LP has $6M sitting in a random bank account. Recovering it is a nightmare.

Fix: Use a portal. Never copy/paste bank account numbers. Verify with the GP before wiring. Some funds require LPs to call to confirm wire instructions.

Issue 3: Timing delay in fund transfer

The LP intends to wire on Day 8. But they're not in the office that day. They wire on Day 11. The wire takes 2 business days to clear. It arrives on Day 13. They're now 3 days late.

Fix: Wire earlier than you think you need to. Leave buffer time. Some LPAs have automatic grace periods; don't count on yours.

Issue 4: Equalization disputes

During the second close, the GP applies an equalization charge. The LP may dispute the interest rate applied or the calculation of the amount they were deemed to have contributed to the first call.

Fix: Get clarification upfront on equalization mechanics. Ask for the detailed calculation. If it doesn't match your understanding of the LPA, push back immediately.

Issue 5: Multi-currency calls

The fund calls capital in both USD (main fund) and EUR (European fund). The LP must coordinate multiple wires, multiple conversions, and multiple timing considerations. One wire is clear, the other isn’t.

Fix: Consolidate if possible. Some LPs establish accounts in the fund's preferred currency to reduce conversion hassle.

The LPA specifies what counts as a "default" and what the consequences are.

Common default definitions:

Common consequences (in order of severity):

Real example:

An LP commits $100M. They fund $40M on the first call. They miss the second call for $30M.

After the grace period, the fund applies $30M + interest + any distributions owed to settle the default. The LP's ownership is diluted because the fund reduced their equity stake as penalty.

If the LP had received distributions during this time, those are withheld and applied against the default.

If the LP continues to refuse, the GP invokes the forfeiture clause. The LP loses the entire $40M already invested.

Most defaults don't go this far. LPs understand the stakes and fund when called. But the penalties are severe enough that defaults are rare.

If you're a GP managing capital calls, here's what matters:

1. Use a standardized template

The ILPA publishes a template. Use it. It reduces LP errors and shows professionalism.

2. Include all necessary information

3. Give notice early

Don't surprise LPs with capital calls. Provide advance notice. Some GPs give LPs a "notice of intent" 30 days before the actual capital call notice. This gives LPs time to prepare.

4. Use a portal

Email is for backup. Use a portal as primary too for automated reminders, dashboard visibility and reconciliation. This helps in reducing errors.

5. Follow up on non-payment

Have a process: Day 5 check-in, Day 10 reminder, Day 12 escalation, Day 15 enforcement. Don't be passive.

6. Communicate

If an LP misses a deadline, call them. Ask why. Maybe the notice got lost. Maybe they have a legitimate issue. Most can be resolved with a conversation.

7. Document everything

Keep records of notices sent, payments received, dates, amounts, any waivers or grace periods granted. This protects you in disputes.

If you're running a fund, capital call management directly impacts:

Best practices:

Capital calls form an operational backbone of private funds. They're where the commitment becomes real and if overlooked, errors can cascade quickly.

For LPs, the takeaway is simple: Treat capital call notices with the urgency they deserve. Set up systems to catch them. Coordinate internally so your CFO knows when they're coming. Build relationships with your GP's operations team. Ask questions if the math doesn't look right.

For GPs, it’s important to make capital calls frictionless for LPs. Use portals. Provide notice. Over-communicate and seek to reduce errors. The administrative effort is small compared to the relationship damage when a capital call goes wrong.

Capital calls aren't glamorous. But they're the plumbing that keeps the whole system working. Get them right, and everything else flows smoothly.

No. If you've signed the LPA and committed to the fund, you must fund when called. Refusal is a breach of contract. The consequences are severe.

Contact the GP immediately. Explain your situation. Most GPs will give a short grace period (7-14 days). Some allow you to use capital call lines (short-term loans against your commitment). Don't just miss the deadline and hope.

Rarely. Most LPAs don't allow commitment reductions. You're stuck with your commitment for the fund's life (usually 10 years). That said, some LPs have negotiated custom terms allowing limited reductions in certain circumstances.

This is a question about LPA terms. Your LPA may have caps (e.g., "maximum annual capital call is 50% of commitment"). If the GP exceeds these, you can dispute it. But most LPAs are written to give GPs broad calling power.

In theory, yes. In practice, no. Each LP has their own commitment and their own capital call. You can't combine. (Though you might coordinate the wire with other LPs going to the same GP to reduce operational hassle.)

Yes, typically. Management fees are usually called as part of regular capital calls. The notice will break down: "Investment capital: $X, Management fees: $Y, Total capital call: $X+Y."

Yes. The interest rate is typically specified in the LPA (often 8-12%). But it's negotiable at closing. Some LPs with strong bargaining power negotiate lower equalization rates.

Not permanently removed, but your interest can be forfeited (per the LPA). Other LPs can overcall and take your stake. You lose your investment.

Ask the GP for a cap table. Your capital call should match your pro-rata ownership percentage. If it doesn't, push back.

Typically, no. Once the investment period closes (usually 5-7 years), the fund stops making new investments. The GP can call for follow-on investments, portfolio company support, fees, and reserves, but not for new company investments. Your LPA specifies this.

That's the GP's problem to solve (through dilution, interest, forfeiture, etc.). It doesn't directly affect you, but it might dilute your ownership percentage if the fund reduces total AUM due to non-payments.