Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

ESOP and ESPP look almost identical on paper, and the two acronyms get mixed up constantly. But they are very different tools. One is a benefit your employer gives you at no cost. The other is a chance to buy company stock yourself, usually at a discount.

If you're an employee trying to understand a benefit on your offer letter, or a founder or HR leader deciding what to offer, the distinction matters for who pays, how the shares are taxed, and what the plan is actually designed to achieve. This guide breaks both down in plain terms and lays out exactly how they differ.

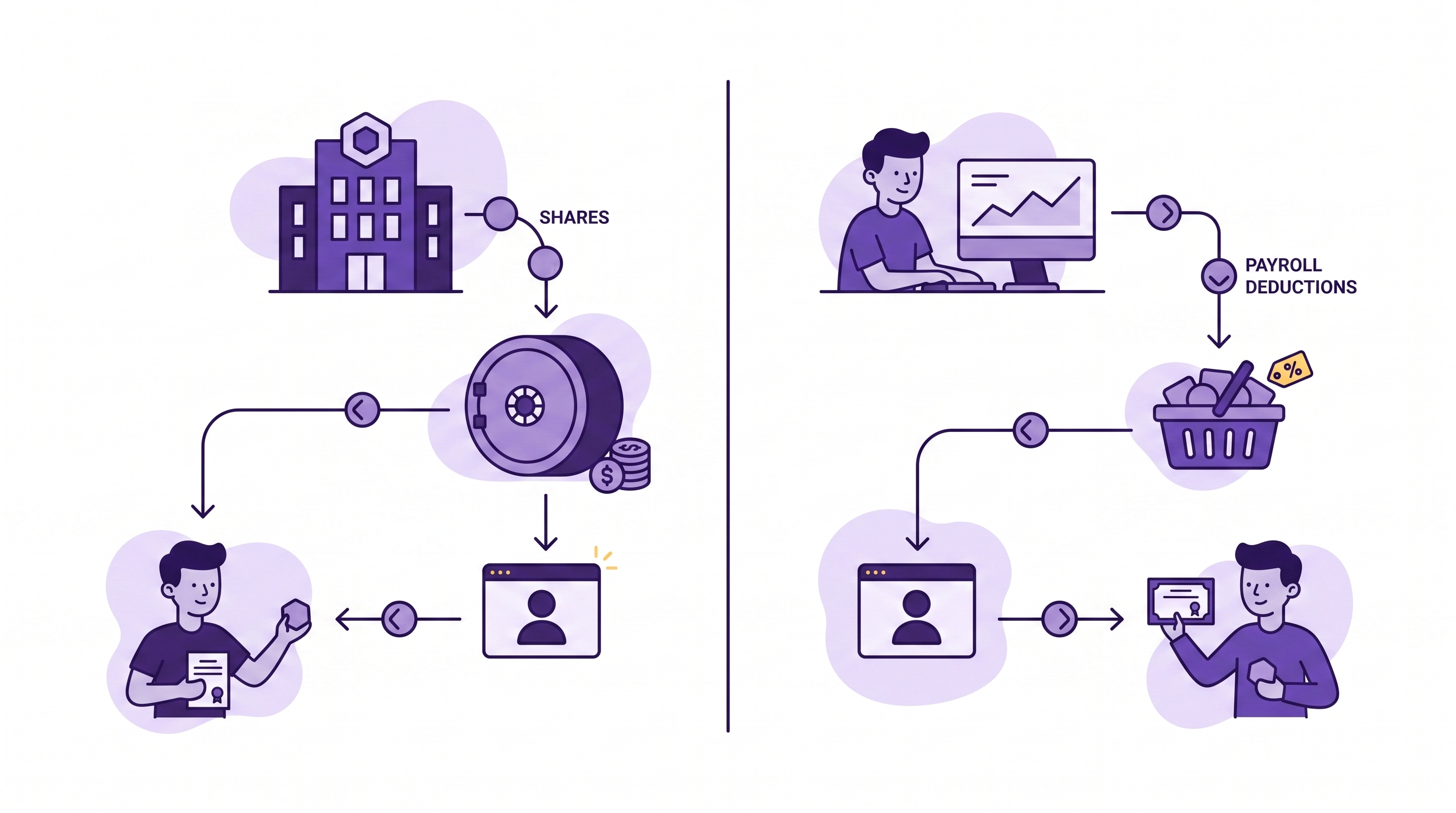

An ESOP is a way for a company to give its employees ownership in the business, without asking them to pay for it. The company sets up a trust, puts its own stock (or cash to buy stock) into it, and gradually assigns shares to employees' accounts over the years, usually based on how much they earn.

Your shares build up over time and become fully yours, on a set vesting schedule. Vesting follows Employee retirement income security act (ERISA) minimum standards, so you become fully vested within three years on a cliff schedule or six years on a graded schedule.

An ESPP is an employee-funded plan, that allows employees to buy company stock at a discount using after-tax payroll deductions. They enroll, choose a contribution rate (commonly 1% to 15% of pay), and the accumulated deductions buy shares on a set purchase date.

The mechanics follow a predictable cycle. During an offering period, which often runs 6 to 24 months, your payroll deductions accumulate. On the purchase date, the plan buys shares for you at a discount, commonly up to 15% off fair market value (FMV).

Both plans exist to solve the same underlying problem: companies want to attract, keep, and motivate good people, and employees want to build wealth and share in the value they help create.

Giving employees an ownership stake tends to align everyone around the same goal. People who own a piece of the business often feel more invested in its success, which can support retention, engagement, and long-term stability.

Here's how the two plans compare across the dimensions that matter most.

ESOP taxation: An ESOP is taxed much like a 401(k). You owe nothing while the shares sit in your account. When you take a distribution, it's taxed as ordinary income, and a 10% early-distribution penalty can apply before age 59½ unless an exception applies. Rolling the distribution into an IRA is a common way to keep deferring tax.

ESPP taxation: With a qualified §423 ESPP, you owe no tax at purchase. The discount and any gain are taxed when you sell, and the split between ordinary income and capital gain depends on how long you hold:

You usually don't choose between an ESOP and an ESPP. ESOPs are typically automatic once you're eligible, while ESPPs are opt-in, meaning you only participate if you elect a payroll deduction. The real questions are whether your company offers one or both, and how much you should participate given your other finances.

There's no legal rule forcing a company to pick one. A business can run both, though it's less common to see a classic ESOP and a broad §423 ESPP at the same employer, since ESOPs lean toward closely held firms and ESPPs toward public companies.

ESOPs work differently because you don't opt in. Read your annual ESOP statement to see your account balance, your vested percentage, and your distribution rights. If you're nearing age 55 with long service, ask HR about diversification rights, which can let you move part of your ESOP account into other investments.

Your choice depends on the outcome you want. An ESOP can serve as an ownership-transition and succession tool, common at closely held companies, while an ESPP is a broad-based engagement perk that's typical at public companies with liquid stock. Each carries real administrative weight.

An ESOP brings ERISA compliance, annual independent valuations, Form 5500 filings, and trustee coordination. An ESPP brings §423 design rules, securities compliance such as Form S-8 and blackout periods, payroll integration to respect the $25,000 cap, and Form 3922 reporting. Both demand clear employee communication so people understand the tax timing before they're surprised at sale.

The coordination across payroll, legal, valuation, and employee communication is what stalls even well-intentioned equity compensation programs.

That's the problem Qapita is built to solve. Whether you're designing your first equity plan or managing an existing one, Qapita's equity management software simplifies everything into one workflow so your team isn't stitching together spreadsheets, advisors, and compliance checklists.

If you're a founder weighing what to offer, or an HR leader trying to run a plan that already exists, see how Qapita’s equity management software helps companies manage equity plans with the software and support to do it right.

The "30% rule" comes from IRC §1042, and it's what lets a business owner defer capital gains tax when they sell stock to an ESOP. After the sale, the ESOP must own at least 30% of the company's stock. The owner who sold the shares then has to reinvest the sale proceeds into "qualified replacement property", generally stocks or bonds of other U.S. operating companies, within a set time window. Meet both conditions, and the tax on that sale gets deferred. This rule only applies to closely held C-corporations, not public companies.

For most employees, yes. A discount of up to 15% off the stock's fair market value is essentially free money, and if your plan has a "lookback" feature, which lets you buy at the lower of the price on the first or last day of the offering period, the effective discount can be even bigger. The tradeoff is concentration risk, meaning too much of your net worth tied up in one company's stock. So the order of operations matters: build an emergency fund first, capture your full 401(k) match next, and only then put money into the ESPP. A common approach is to buy at the discount and sell on a regular schedule rather than holding indefinitely, so you capture the gain without letting the risk pile up.

All three give you a stake in company stock, but they differ in who pays and when you're taxed. An ESOP is employer-funded: shares sit in a trust for you, and you don't pay anything to get them. An ESPP is employee-funded: you buy shares yourself, usually at a discount, using after-tax payroll deductions. An RSU works differently from both, since it's a grant rather than a purchase, you're given shares that vest over time, with no purchase required, and they're taxed as ordinary income the moment they vest. The core distinction to remember is funding and tax timing: who pays for the shares, and when the tax bill comes due.