Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

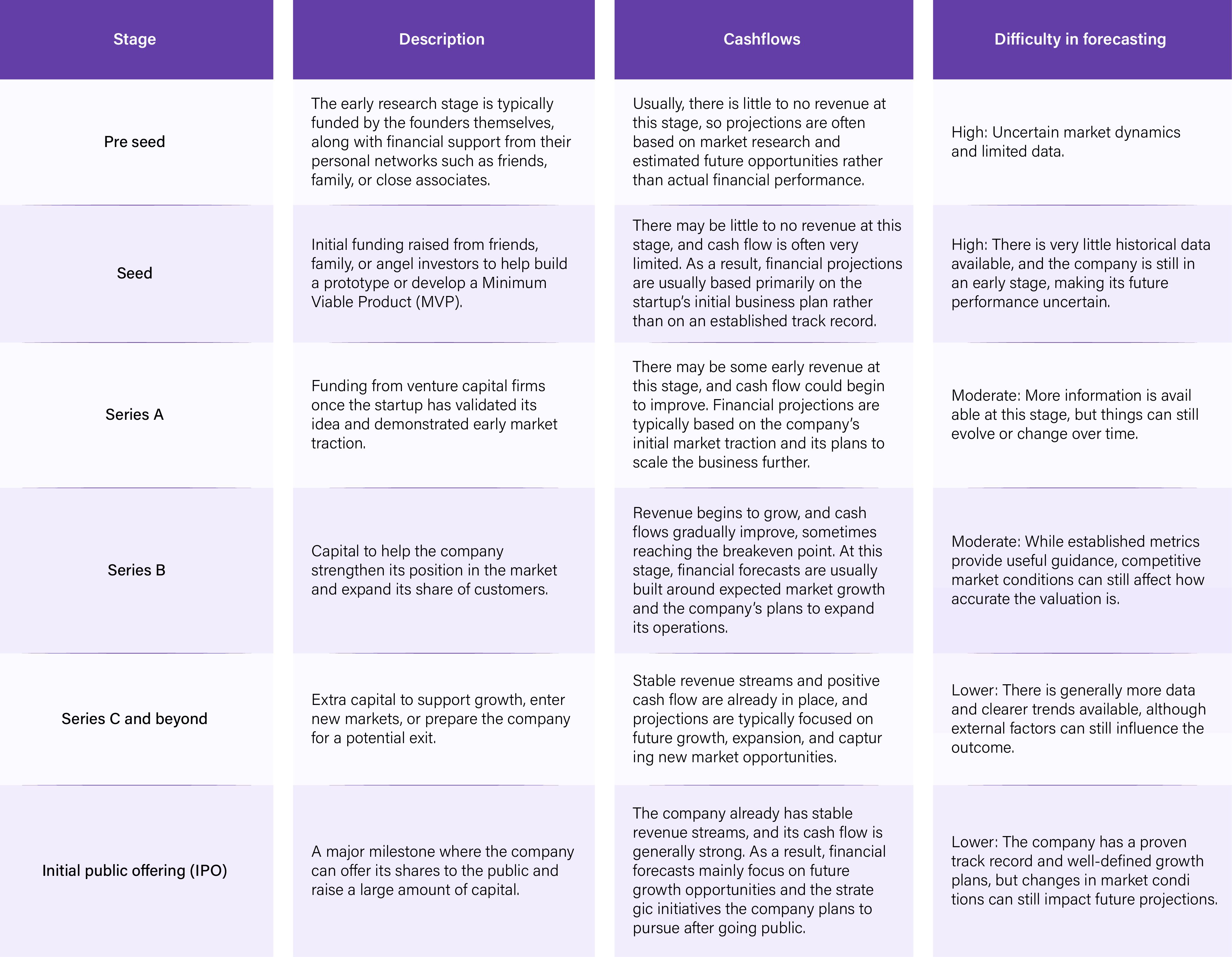

For startups, valuation plays a crucial role in facilitating the fundraising process. It forms the basis for the equity exchange that takes place during the fundraise. The equity that investors get for their money is decided by the startup's valuation. But how is the valuation of a startup calculated?

Valuation, simply, is the worth of a company if it were to be sold. This holds for most of the well-established businesses with positive cash flows and profits.

But, generally, startups have little to no revenue. So, putting a valuation on startups is very much different than for a large company for two reasons.

The first reason being startups valuation is mostly notional. Startups are considered risky investments because of their high failure rate. A startup valued at hundreds of millions could go bankrupt and become worthless.

Startup valuation is the process of estimating a startup's value at a given point in time. It plays an important role at every stage of a company’s growth, particularly when raising funds, bringing in strategic partners, or preparing for a potential exit.

Several factors are considered when determining a startup’s valuation, such as the size of the market opportunity, the stage of product development, the strength of the founding team, current revenue, and expected future growth. For investors, the valuation reflects how they assess the startup’s risk and potential return. In the end, a thoughtful and realistic valuation can help startups attract funding, build partnerships, and create opportunities for long-term growth.

This guide is designed to make startup valuation easier to understand. It provides a clear overview of what valuation means, the different methods used to calculate it, the market factors that influence it, and the key objectives behind it. It also highlights common valuation mistakes and explains the roles, motivations, and incentives of the main stakeholders.

Valuation always involves a degree of estimation and judgment, but the process becomes even more complicated when it comes to startups. Since early-stage companies often have limited data and unpredictable cash flows, selecting the right valuation approach is crucial to determining their value and building investor confidence.

For startups, valuation plays a key role during fundraising. It serves as the foundation for the equity exchange that occurs when investors invest in the company. In simple terms, a startup’s valuation determines how much ownership investors receive in return for their investment.

Understanding valuation is essential for founders who want to raise capital, investors who allocate funds, and advisors who help bring the two sides together.

Startups can be valued using several different methods, and founders and investors often use more than one approach to arrive at a reasonable valuation range. The method chosen usually depends on the startup’s stage of growth. Early-stage startups often rely on qualitative methods like the Berkus or Scorecard method, while later-stage companies use data-driven approaches such as market multiples, the VC method, or discounted cash flow (DCF).

Here are the 12 most used startup valuation methods.

This approach estimates a company’s future cash flows, usually over the next 5–10 years, and discounts them to their present value to estimate the company’s current worth.

The discount rate reflects the return investors expect. Higher risk means using a higher discount rate.

The Discounted Cash Flow (DCF) model helps determine a company’s intrinsic value based on fundamentals, rather than market sentiment.

However, applying the DCF model to startups can be challenging due to uncertainty in predicting future cash flows. Startups often lack a long operating history, face volatile markets, and may not have consistent revenue streams. These factors make it difficult to estimate future performance exactly, leading to many assumptions. Because of this, the DCF method is rarely used on its own when valuing startups.

A variation of this approach is the First Chicago Method, commonly used for startups that have already begun generating revenue. This method considers multiple possible outcomes, typically best-case, base-case, and worst-case scenarios. Each scenario is valued using the DCF approach, and then a probability-weighted average is calculated to estimate the startup’s overall valuation.

The market valuation approach, also called the comparable company approach, is based on the prices of comparable companies. It estimates a startup’s value by comparing it with other similar companies. As the name suggests, this method looks at how comparable startups are valued in the market. The result is a reasonable valuation for your own company.

This approach is common for early-stage startups. Analysts compare your company to similar startups that recently raised funds or closed deals.

When identifying comparable companies, several factors are considered. These include the startup’s business model, company size, stage of development, geographic presence, target customers, revenue levels, market size, and organizational structure.

Since every startup is unique, certain adjustments are usually required to arrive at a more accurate valuation. For example, adjustments may account for differences in the products or services offered, the geographic locations of operations, the company's profitability, growth rate, or customer acquisition strategy.

One advantage of this method is that it is relatively simple and relies on real market data, thereby making the valuation more realistic. It also reduces the need for subjective assumptions or predictions.

However, this approach can be problematic to apply in new or emerging markets, where there may not be enough comparable companies or reliable data available.

The VC valuation method lets founders quickly estimate their startup’s value without much data or research.

This method is popular for its usefulness with early-stage or pre-revenue companies, making it a standard tool for venture capitalists estimating pre-money valuations.

Under this approach, investors first estimate the company's potential exit value after 3–5 years. Based on that expected future value, they work backward to determine the valuation at which they should invest today, while also considering the return they expect given the level of risk. The exit value is the company’s estimated value at a future liquidity event, such as an initial public offering (IPO), merger, or acquisition, when investors can realize their returns.

However, one major limitation is that this method relies on neither detailed business fundamentals nor performance metrics.

It depends mostly on market expectations and assumptions about future value for investors using this method, the investor's expected return can be expressed as:

Investor’s Expected Return = Exit Value / Post-Money Valuation (assuming no future dilution)

For example, if the exit value is $20 million and the post-money valuation is $2 million, the expected return is 10x. If the investor seeks a higher return to account for greater risk or anticipated dilution, they might adjust the investment amount or negotiate a lower valuation accordingly.

Also read: The key to startup funding: Pre-money vs post-money valuation

Also known as the stage development method, the Berkus method was developed by angel investor Dave Berkus. It is a simple approach for estimating the value of very early-stage startups by evaluating five key factors that influence a company’s potential success.

The five factors are: the strength of the idea, prototype, or product development; the quality of the management team; strategic relationships; and product launch or early sales.

Each factor gets a set monetary value. If fully satisfied, a factor typically adds $500,000 to the valuation. Satisfying all five can bring a pre-money valuation up to $2 million.

The method also assumes that investors may aim to exit their investment after about 5 years at a valuation of $20 million, yielding roughly a 10× return on their initial investment.

The Berkus Method becomes less relevant once a startup generates revenue, but it remains useful in the earliest stages. It lets founders and investors estimate value and guide fundraising discussions.

This method primarily estimates a pre-revenue startup's median valuation by comparing it with similar companies. It is commonly used by angel investors when evaluating startups in their earliest stages.

As the name suggests, different scoring factors are used to adjust the estimated average valuation. While the specific criteria may vary from one investor to another, some commonly used factors include:

It is important to note that this method involves some subjectivity, as the final assessment depends on the judgment of investors or analysts evaluating the company. At the same time, applying this approach requires significant data, research, and careful analysis.

Key factors investors consider include management team strength and experience; market opportunity size; product or technology quality; competitive landscape; marketing, sales channels, and partnerships; and any need for additional funding.

The book value method estimates a company’s net asset value (NAV) based on its balance sheet.

A balance sheet lists a company’s assets, such as real estate, cash, stocks, equipment, and intellectual property (such as trademarks, copyrights, and patents), along with its liabilities. The difference between these two gives the company’s net asset value.

NAV = Total Assets – Total Liabilities

This approach can also help estimate a company’s liquidation value. While it’s simple and often used as a baseline valuation, it may not fully capture a startup's true value, especially in its early stages. As a result, it’s usually used as a starting point for deeper valuation analysis.

Precedent transaction analysis values a company by reviewing the prices buyers paid in recent acquisitions of similar businesses. By examining these comparable deals, you see what buyers actually paid for companies in the same industry. This approach establishes a practical benchmark for valuing your company by using the valuation multiples observed in those transactions.

The cost-to-duplicate method is a simple valuation approach that looks at the actual money and resources spent to build a startup, such as development costs, equipment, and other tangible investments. While it offers a clear starting point for valuing early-stage companies, it also has limitations because it does not account for intangible assets such as brand value, intellectual property, or the startup’s future growth potential.

The cost-to-duplicate method values a business based on the actual cost of recreating it from scratch. Here are the basic principles of this method.

The method is based on real, historical expenses rather than future projections. Therefore, it provides a clear and objective estimate of the company’s current invested value.

The cost-to-duplicate method is particularly useful for startups that have not yet generated revenue or built a strong market presence, as it offers a practical, often conservative valuation.

In simple terms, this method serves as a reality check by focusing on the actual money spent to build the business rather than its future potential value.

The risk factor summation (RFS) method is a simple way to estimate a startup's pre-money valuation. It starts with the average valuation of a comparable startup and adjusts it based on several risk factors.

Let’s explore how you can put this method into action.

To boost your valuation, look for risks in your venture and consider strategies to reduce them wherever possible.

Revenue multiples quickly estimate a startup’s value, especially for businesses with recurring revenue. Investors use revenue multiples as a relative valuation method, comparing a company’s value to how the market prices similar companies.

Investors typically apply revenue-based multiples to companies with negative profit margins, where they cannot use traditional valuation metrics like EV/EBITDA or EV/EBIT.

In general, analysts use revenue-based multiples only when other valuation methods do not suit the situation, such as when a company has not yet achieved profitability.

Are you curious about which revenue multiples are most common? The two you’ll see most often are: Enterprise Value-to-Revenue (EV/Revenue) = Enterprise value/Revenue and Price-to-Sales (P/S) Ratio = Market capitalization/Sales.

EBITDA multiples value mature startups with positive earnings. Applying an industry-standard multiple to projected EBITDA estimates the company value based on profitability, helping investors assess financial health and growth potential.

The EBITDA multiple compares a company’s enterprise value to its annual EBITDA, using historical or projected results. It estimates value and benchmarks the business against industry peers.

The EBITDA multiple can be calculated using this formula:

EBITDA multiple = enterprise value / EBITDA

To determine the enterprise value and EBITDA:

This method estimates valuation ranges based on a startup’s development stage.

Early-stage startups with only a prototype carry higher risk and usually receive lower valuations than those with validated products and customers.

A startup’s value hinges on its future growth. Since growth is uncertain, how do we reflect it in valuation?

Here are a few ways:

• Identify key growth drivers: For instance, increasing demand for sustainable products can support long-term growth for a green cleaning supplies company.

• Analyze market trends: Growth patterns from comparable companies offer benchmarks.

• Evaluate customer acquisition: This estimates how quickly revenue can scale.

• Review customer retention: Strong efforts show the ability to reduce churn.

• Assess scalability and expansion: This reveals if the business can grow rapidly or faces limits.

Here are the advantages of startup valuation.

• Connect your startup: Connect with its story, market, product, and vision to numbers, appealing to both narrative and data-focused investors.

• Map revenue, costs, funding needs, and dilution: Justify your fundraising ask and show how capital will be used.

• Show you understand your business and numbers: Highlighting professionalism and boosting investor confidence.

• Support your valuation: With clear methods, comparables, and KPIs. Build credibility and keep negotiations realistic.

• Share valuation analysis: Do this to reduce information gaps and build trust. Discuss assumptions for a fair, data-driven conversation.

Valuing startups presents several important challenges and drawbacks.

• Limited Data: Startups lack long financial histories, making future predictions tough.

• Uncertain Growth: Rapidly changing markets make growth hard to predict, and leadership changes quickly.

• Few Comparable Companies: Unique models or new markets make comparisons difficult.

• Subjectivity in Valuation: Valuations often depend on human judgment. Factors such as an investor’s experience, risk appetite, and market outlook can influence a startup's valuation.

• Multiple Funding Rounds: Each round brings different valuations, making tracking complex.

Our team of experts helps you select the best-suited valuation method for your startup, ensuring you're investment-ready for term sheet and negotiation stages. Qapita centralizes your cap table, investment documents, and stock options administration in one secure platform. Share precisely what investors need to advance confidently.

Book a demo to get started.

Seed valuation is the estimated worth of a company at the seed fundraising stage. It is based on factors such as the founders’ experience, market potential, early traction, and comparable startups. The final value is often set by negotiation or by analyzing the required fundraising amount and the equity offered.

The VC valuation method is an approach in which investors estimate a startup’s potential exit value, such as an IPO or acquisition, and discount it to its present value using expected rates of return. This method may also factor in comparisons to similar companies and projected financial results.

Pre-money valuation is what your startup is worth before new investment comes in. Post-money valuation is what it's worth after, calculated as pre-money valuation plus the investment amount. The difference between the two determines how much equity a founder gives up in a funding round.