Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

During fundraising, various term sheets may be offered from different investors. It may be daunting for first-time founders who are unfamiliar with the terms listed in term sheets and not knowing which term sheets offer the "best" deal. While it may be tempting to go for the investor that offers the most capital at the highest valuation, it is crucial to take a step back and examine exactly what conditions the term sheet entails.

If you reach out to angels or venture capitalists for the purpose of fundraising, and if they are interested in investing in your business, they will communicate the terms through a term sheet

These general terms include things, such as:

1. how much money they are going to invest,

2. what ownership they want in your company in return for this money,

3. the company valuation,

4. Other rights and so on.

The term sheet is a document that outlines these terms. Although term sheets may seem complicated, understanding the basic terms and knowing what to expect will minimise this complexity. This will help you to make more informed decisions.

A term sheet is a non-binding agreement that lays out the basic terms and conditions to be agreed on by both founders and investors during fundraising. The term sheet will include details such as the amount of investment, type of security, rights and preference of security.

Founders can negotiate with investors on what terms should be included that would benefit both parties in exchange for the investment. With open discussions, this builds a healthy relationship between founders and investors that can potentially last a long time. This also helps to prevent any potential misunderstanding and misalignment of interests between founders and investors.

When both parties have agreed on the terms and conditions in the term sheet, a formal contract will be drawn up in accordance with the details listed on the term sheet.

We've compiled a list of items you should look out for in your term sheet.

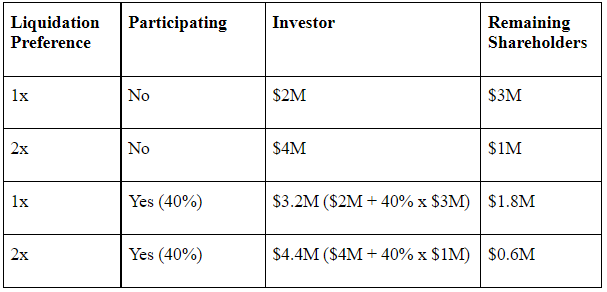

Liquidation preference refers to how the startup's proceeds will be distributed in the event of sale, liquidation, dissolution or winding up. It guarantees the return of investor capital before any distributions are made to common shareholders.

Liquidation preference is usually set at 1x, hence investors will receive their full investment back from the proceeds.

For example, if an investor invests $2M in preferred shares and the company gets sold for $5M, the investor will receive $2M first. The remaining $3M will be distributed to the remaining shareholders.

If an investor wants more than 1x liquidation preference, it may impact the payouts to the remaining shareholders.

Building on the previous example, if the investor gets a 2x liquidation preference, he will receive $4M ($2M x 2), and only $1M will be left to distribute to remaining shareholders

If the company gets sold for a lower valuation of $4M, this would mean that there is nothing left for the remaining shareholders.

Hence, founders have to be wary of the liquidation preference required by the investor as they could potentially receive nothing in return for years of hard work.

You can use Qapita to run various scenarios to determine what level of liquidation preference with which you may be comfortable.

In addition to the liquidation preference, investors may also have a participating right called "double dips".

This means that after receiving the initial liquidation preference distribution, the investor will also receive a pro-rata share of the remaining proceeds, together with the other shareholders on an as converted basis

Let's suppose an investor invests $2M for 40% of the company. If the company is sold for $5M, the investor receives $2M for 1x liquidation preference, and an additional $1.8M (40% of the remaining $3M). So, the investors will get a total of $3.2M and only $1.8M will be left for distribution to the rest of the shareholders.

In a double dip, the investor will get a return on capital in most cases.

You should be wary of participating preferred shares in addition to liquidation preferences, especially when the liquidation preference is already more than 1x!

Let's see how much the common shareholders get in different cases.

Investor has 40% shares and the company is sold at $5M

Anti-dilution provision serves to protect investors in the event of a down round, where the valuation of a current fundraising round is lower than the previous round. This means that when new shares are sold at a lower price during a down round, the existing ownership of the investor will not be overly diluted.

There are two main types of anti-dilution provisions:

1. Full Ratchet: Full ratchet anti-dilution will give the full benefit of lower valuation to the past investor i.e., it reprices the shares of existing investors at down round price.

2. Weighted average: Weighted average is more commonly used, which tones down the adjustment taking into account the number of shares issued in the down round.

A full ratchet anti-dilution provision would usually allow investors to receive much more additional shares compared to a weighted average anti-dilution, which would place founders in a precarious situation during an unexpected down round. Founders have to understand how the different anti-dilution provisions would potentially affect the ownership structure of the company before agreeing to the terms.

Pro-rata rights give investors the option (but no obligation) to invest in future financing rounds in proportion with their ownership. This allows investors to maintain their ownership percentage which otherwise would have been diluted in subsequent funding rounds.

For example, if an investor had 200 shares out of 1000 shares (20% ownership) with pro-rata rights, it will give the investor the option to purchase 1000 shares (20% x 5000) if an additional 5000 shares are being issued now.

An investor would want to have pro-rata rights as they have priority to purchase more shares when the company is doing well, and at the same time, maintain their ownership percentage.

Founders should understand if their existing investors intend to exercise their pro-rata rights to give a correct picture to the new investor.

Fundraising can be intimidating for first-time founders. VCs who craft term sheets regularly will often have the upper hand during negotiation, especially when founders are cash strapped.

Before signing the term sheet, ensure that you go through every terms and conditions listed and clarify any doubts you have. Negotiating better terms may not always be successful when both parties cannot find a middle ground.

Founders need to understand what exactly they are looking for as compromising to unfavorable terms will inevitably lead to their downfall.

Thank you for reading.

If you are drafting a new ESOP plan document, please contact us and we can assist you.