Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Right of first refusal (ROFR) and right of first offer (ROFO) are contractual rights written into a shareholder agreement (SHA) that control how an existing shareholder can sell their shares to an outside party.

The core difference comes down to timing and who sets the price, and that difference has a direct bearing on how much leverage a founder retains when they want to sell.

Let's break both down in detail.

Well as the name indicates, these are certain contractual rights given to shareholders that govern the transfer of shares by a set of shareholders to a third party.

Pre-emptive rights concern the issuance of fresh shares by the company for investment going into the company, while ROFR and ROFO apply to the transfer of shares by an existing shareholder to a third party. In this case, the consideration against the shares goes towards the selling shareholder.

ROFR is the right given to a shareholder (or a set of shareholders) to have an opportunity to buy shares of the selling shareholder at the same price and terms or higher as being offered by a potential third party buyer.

Key things to note:

1. In case a shareholder is looking to sell shares to a third party ROFR basically mandates this selling shareholder to offer their shares to the right holder on the same terms as the bid from a third-party potential buyer.

2. Hence, whenever ROFR is applied, it is assumed that the selling shareholder is supposed to receive a bid for the given number of shares from a potential third party buyer.

3. Shareholder(s) with ROFR can then choose to buy the shares at the same price and terms as the third-party bid, or 'Refuse' the offer. Hence the name: 'Right of First Refusal', only after they first refuse to buy the shares themselves can the seller proceed to sell to the third-party buyer at the same or a higher price

It's for the same purpose as ROFR, but with a slight difference in the process. Unlike ROFR where the selling shareholder has to first receive a bid from a third-party buyer before offering it to the ROFR shareholder

Key things to note:

In case of ROFO the selling shareholder needs to first offer the shares to the shareholder(s) with ROFO before soliciting any third party bids. Hence the term 'Right of First Offer

Before diving into the mechanics, here are a few key aspects about ROFR and ROFO that every founder should be aware of.

1. Intention of these rights: Both these rights ROFO and ROFR give a higher priority to shareholders with these rights (typically the investors) to potentially buy shares before they are sold to a third-party buyer. This provides an option for shareholders to not just acquire a larger share in the company but also prevent any unwanted shareholder to acquire shares by bidding a higher price. Hence strategic stakeholders in a company would prefer to have these rights.

2. Investor rights: In most cases, these rights are given by founders to the investors. So that founders do not sell their shares to third parties who the investors do not desire to bring on the captable. Also, investors feel they need to have the option of buying any shares that are being offered in the market pre-emptively to increase their stake further.

3. Promoter ROFO/ROFR on investor shares: While it is not very common, it would also make sense for promoters or founders to have transfer rights for transfer of shares by investor. Given their strategic interest and alignment with the company and the fact that mostly they also turn out to be a majority shareholder on the captable, it would make sense for Promoters or Founders too to have ROFO/ROFR rights on the investor's shares. This is to ensure; investors do not opportunistically sell to a third-party buyer which might jeopardize the company's future interest. (Eg: selling a significant stake to a competitor or a mis-aligned buyer etc.)

4. While the clause is quite generic and can apply to any category of shareholders, it is typically observed that these rights are given in favour of investors for transfer of shares by promoters and other shareholders.

A quick example for ROFR. There is no standard template as such.

If any of the founders (or other Shareholders) decide to Transfer ('Selling Shareholder') all or part of the Shares held by such Selling Shareholder ('Sale Shares') to any Person, then such Selling Shareholder unconditionally and irrevocably grants to the Investor a prior right (but not an obligation) to purchase all or a portion of the Sale Shares at the same price and on the same terms and conditions as those offered to a third party buyer.

A quick example for ROFO

If any of the Founders (or other Shareholders) intend to Transfer ('Selling Shareholder') all or part of the Shares held by such Selling Shareholder ('Sale Shares') to any Person, then such Selling Shareholder shall first serve a written notice ('Sale Notice') to the Investor specifying the number of Sale Shares and inviting the Investor to make an offer. The Investor shall, within the Acceptance Period, have the right (but not an obligation) to submit a binding offer specifying the price and terms at which it wishes to purchase the Sale Shares. The Selling Shareholder may, upon expiry of the Acceptance Period or upon rejection of the Investor's offer, Transfer the Sale Shares to a third party at a price no lower than the price offered by the Investor.

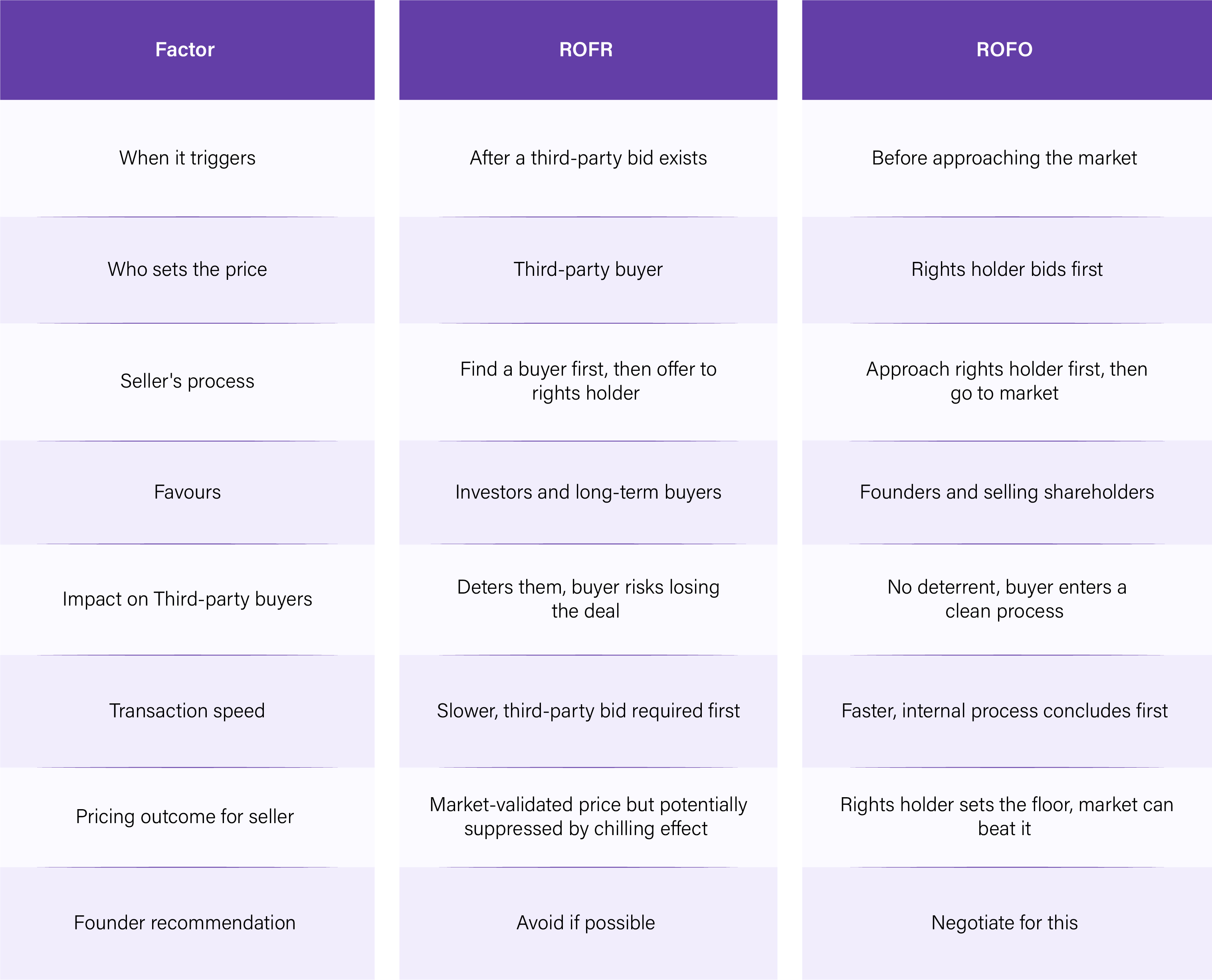

Both ROFR and ROFO serve the same purpose but operate very differently, here is how they compare side by side.

Understanding how ROFR and ROFO work, there are a few contractual details that can impact a founder's ability to sell shares when the time comes.

1. Acceptance period: ROFR and ROFO clauses come with an acceptance period which defines the duration the right holder has to respond to the offer. Typically, this duration is 30 days. Avoid having it longer than 30 days.

2. Lock-in clauses: Founders should be cautious of any promoter Lock-In clauses in SHA which will prohibit any full or part transfer of shares to a third party (we'll cover this in the upcoming series). This will play out even before ROFO/ROFR triggering! So prior approval from investors needs to be taken even before finding a third-party buyer. More on this soon.

3. Tag-along clauses: Along with ROFO and ROFR, Investors typically also have tag clauses which gives them the right to tag along their shares in sale of any shares by the promoters. This might impact the actual number of shares the promoters can sell. We'll cover this too shortly.

4. ROFR vs. ROFO: It is advisable for founders to negotiate giving investors a ROFO instead of ROFR as it also puts an onus on investors to determine a reasonable price instead of just accepting or rejecting a price given by a third party (in case of ROFR). This gives an option to the selling shareholder to either accept the price or go to the market in anticipation of a higher price. Thus, selling shareholders in case of ROFO might maximise a higher value.

5. Mind the language: While what is mentioned in this blog is assuming the usual clauses seen in SHAs, Founders should note that these are contractual rights, and the terms and language can be completely customized by the parties to suit their needs. So be careful of what you are signing up for. Avoid giving away these rights to all shareholders/investors. You can limit it to strategic or lead investors who have a significant shareholding.

This is one of the most practical questions a founder faces in a live secondary transaction, and the answer depends entirely on how the SHA is drafted.

If the acceptance period expires without a response:

If the rights holder declines or fails to respond within the specified timeframe, the selling shareholder is free to complete the transaction with a third party, usually under terms no more favourable than those offered to the ROFR holder.

In simple terms, silence is treated as a waiver. If a holder does not respond by the deadline, their right is gone for this specific sale.

The right does not disappear permanently:

Declining to exercise the right for a particular transaction does not permanently extinguish it, the ROFR reactivates for any future transfer. The rights holder simply loses the opportunity for that specific sale, not the right itself going forward.

What founders should watch for in the SHA language:

If a sale is not completed within a specified period from the date of expiry of the ROFR period, the right of first refusal is deemed to be revived, and the shares cannot be offered or transferred until they are first re-offered to the other shareholder in accordance with the agreement. This means if a founder fails to close the third-party deal within the window specified in the SHA after the ROFR lapses, the entire process resets from the beginning.

The practical implication:

Once the acceptance period expires and the rights holder has not responded, the founder must move quickly to close the third-party transaction. Delays beyond the SHA-specified window can revive the rights holder's claim, forcing the founder to restart the entire ROFR or ROFO process.

Most founders treat ROFR and ROFO as investor-protective clauses, something to accept, understand, and move on from. That is the wrong spectrum angle to look from. These rights are not just about who gets to buy shares first. They are a powerful signal of how your cap table will behave under pressure. An investor who holds ROFR on your shares controls the pace, the pricing, and the optics of every secondary transaction you attempt. The clause you sign today determines the conversation you have three years from now when a secondary buyer is at the table, due diligence is done, and an investor has 30 days to decide whether to step in.

Founders who understand this do not just negotiate which right to give, they negotiate the acceptance period, the threshold shareholding, the scope of shares covered, and whether the right is mutual. That level of precision at the term sheet stage is the difference between a clean secondary exit and one that stalls, suppresses price, or never closes at all. The SHA is not a formality. It is the rulebook that governs every share transfer your company will ever see.

When ROFR or ROFO rights are exercised, the impact lands directly on your cap table, ownership percentages shift, transfer records need updating, and compliance documentation follows. Managing that manually is where errors happen.

Qapita's cap table management platform keeps your ownership records accurate and audit-ready at every stage. From recording secondary transactions and share transfers to modelling how a ROFR exercise affects dilution across your shareholder base, everything is tracked in one place with a clear audit trail.

The platform supports the full spectrum of equity, founder shares, investor preferred stock, ESOPs, SAFEs, and warrants, with built-in workflows for board consents, investor updates, and structured governance. Trusted by over 2,400 fast-growing companies globally and rated the best in customer satisfaction on G2, Qapita is built for founders who want clarity over their equity at every stage of the company.

Book a demo to see how Qapita can bring structure and confidence to your equity management.

Both rights govern the transfer of shares to third parties but operate at different points in the process. Under ROFR, the selling shareholder must first secure a third-party offer and then present it to the rights holder to match or decline. Under ROFO, the selling shareholder must approach the rights holder before going to market. The fundamental distinction is timing, ROFR gives the rights holder the last opportunity to purchase, ROFO gives them the first.

If the rights holder does not respond within the defined acceptance period, typically 30 days, the right lapses for that specific transaction. The selling shareholder may then proceed with the third-party buyer at the same or a higher price. The right is not permanently extinguished, it remains in force and reactivates for any subsequent transfer of shares.

No. pre-emptive rights apply to the issuance of new shares by the company, they give existing shareholders the option to participate in a fresh round to maintain their ownership percentage. ROFO and ROFR apply to the transfer of existing shares between shareholders. They are triggered by a sale, not an issuance, and serve an entirely different purpose within a Shareholder Agreement.

ROFR is a contractual right that gives a designated shareholder, typically an investor, the opportunity to purchase shares from a selling shareholder before those shares are sold to an outside party. The rights holder can either match the third-party offer and acquire the shares, or decline and allow the sale to proceed. It is a protective mechanism designed to give existing shareholders control over who enters the cap table.

ROFO is generally the more favourable structure for a founder looking to sell shares. Under ROFO, if the rights holder's bid does not meet expectations, the founder can take the shares to market and seek a higher price. Under ROFR, the founder must find a buyer, negotiate terms, and then hold the transaction while the rights holder decides whether to step in and match. ROFO gives the founder more control over the process and a cleaner path to a secondary transaction.

Yes. Founders have a legitimate and often overlooked interest in controlling how significant investor stakes are transferred. An investor selling a large block of shares to a competitor, a misaligned strategic buyer, or a purely financial party with no sector alignment can pose a real risk to the company's direction and governance. Founders can negotiate for mutual transfer rights, applying ROFO or ROFR to investor share transfers as well as their own. This is not standard in most boilerplate SHAs but is entirely reasonable and increasingly common in founder-friendly deals.

It depends on how the Shareholder Agreement and ESOP plan documents are drafted. If the SHA covers all shareholders without specific carve-outs, ESOP participants who have exercised their options and hold shares may trigger ROFR or ROFO provisions when selling in a secondary transaction. Founders should review their SHA carefully to determine whether ESOP holders fall within the scope of transfer restrictions before structuring any employee liquidity programme.

-T.jpeg)