Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

General Partners (GPs) are the driving force behind private equity (PE) funds. They structure, fundraise, manage investments, and execute exits. While Limited Partners (LPs) provide capital, GPs commit themselves to develop value and deliver returns.

These professionals are the active managers who transform capital into profitable ventures, distinguishing themselves from passive investors through their hands-on approach to portfolio management.

In this article, we'll explore the role of GPs in depth, examining who they are and what they do.

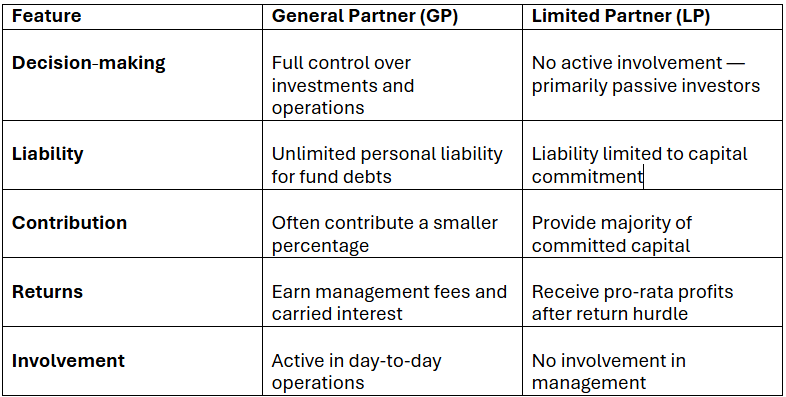

A General Partner is a individual or organization that oversees the management of a private equity or venture capital fund. GPs make all investment decisions, oversee the fund's operations, and assume full legal liability for the partnership's obligations. Unlike limited partners, GPs are actively involved in the fund's daily management and bear unlimited liability for its debts and actions.

The general partnership structure enables general partners to maintain control over investment processes. This setup attracts capital from limited partners who wish to gain exposure to private equity returns without the responsibilities of active management. It creates a distinct division of roles: general partners provide their expertise and management skills, while limited partners contribute the necessary capital.

General Partners (GPs) in private equity have extensive responsibilities that last the entire lifecycle of a fund. Unlike Limited Partners (LPs), whose involvement ends after contributing capital, GPs are accountable for all critical aspects of managing and growing the fund. Their work includes fundraising, investment decisions, portfolio value creation, and reporting.

One of the most demanding tasks for a GP is securing commitments from LPs. GPs rely heavily on their track record, credibility, and market expertise to attract investors in an increasingly competitive private equity and venture capital landscape.

GPs identify promising investment opportunities, conduct rigorous due diligence, and negotiate deals to secure favorable terms. Strategic judgment and risk management are central to ensuring that capital is effectively allocated across portfolio companies.

After investments are made, GPs actively monitor and support portfolio companies. This often involves mentoring founders, facilitating industry connections (e.g., potential customers, key hires, or strategic partners), and helping raise additional funding when needed. The GP's network and operational insight play a crucial role in driving company growth.

GPs determine when to participate in subsequent funding rounds to maintain or increase ownership stakes. This requires balancing pro rata rights, fund reserves, and the long-term potential of each company.

Transparency is vital in private equity. GPs keep LPs informed through regular performance updates, portfolio reviews, and detailed financial reports. Many GPs also host annual meetings and provide tailored updates for key LPs to strengthen relationships.

Beyond dealmaking, GPs are responsible for ensuring accurate tax filings, financial reporting, compliance, and other administrative obligations. These tasks ensure that the fund operates smoothly and meets regulatory standards.

General Partners (GPs) in private equity make their earnings from a mix of management fees, bonuses based on performance, and returns from their own investments. This structure is designed to ensure that the interests of the GPs align with those of the Limited Partners, while also covering operational costs and driving the overall success of the fund.

Typically, GPs work under a "2 and 20" fee arrangement. This means they get a 2% management fee on the total assets managed and also get 20% of the profits from investments. This compensation structure aligns GP interests with fund performance while providing predictable income for fund operations.

GPs typically receive an annual management fee, calculated as a percentage of the fund's total committed capital. This fee, often around 2%, is used to cover the day-to-day operations of the fund. It funds salaries, office expenses, legal and accounting services, compliance, and other administrative activities. While it does provide income to GPs, the primary purpose of the management fee is to ensure the smooth running of the fund over its lifetime.

Carried interest represents the GP's share of the fund's profits and acts as a performance-based reward. GPs usually earn about 20% of any returns generated by the fund that exceed the capital initially contributed by LPs. Importantly, this payout is only triggered after LPs have recovered their invested capital-often along with a preferred return, also known as a hurdle rate. Many funds also include clawback provisions, which require GPs to return a portion of their carried interest if future losses offset earlier gains.

GPs often invest their personal funds alongside LPs in the fund, typically contributing 1% to 5% of the fund's capital. This personal stake means they participate in distributions just like any other investor, further aligning their incentives with LPs and demonstrating their confidence in the fund's strategy.

General Partners have significant authority over investment decisions, fund operations, and portfolio company strategies. This level of control allows GPs to actively shape the fund's direction and make impactful decisions that drive growth and returns.

Through carried interest and personal investments in the fund, GPs stand to earn substantial rewards if the fund performs well. The structure allows GPs to benefit directly from the value they help create, offering potential for considerable financial upside beyond base compensation.

Serving as a GP offers unmatched opportunities to build networks, deepen expertise in dealmaking and operations, and enhance reputation in the private equity industry. The role provides continuous learning as GPs engage with diverse sectors, founders, and complex business challenges.

In a traditional general partnership structure, GPs face unlimited personal liability for the obligations of the fund. This means their personal assets could be at risk if the fund encounters legal or financial issues, though many modern funds mitigate this through structured entities.

Running a private equity fund demands intense commitment. From raising capital and closing deals to supporting portfolio companies and managing investor relations, GPs often work long hours across multiple responsibilities over a fund's decade-long life.

GPs are under constant pressure to deliver results. LPs closely monitor fund performance, and any underperformance can impact a GP's ability to raise future funds, damage reputation, or lead to legal and financial consequences (e.g., clawbacks).

GPs are expected to invest their own capital-typically 1% to 5% of the fund-which represents a significant personal financial commitment. This requirement ensures alignment with LPs but can place strain on personal finances, especially for first-time GPs or smaller firms.

General Partners are the central architects, operators, and risk-takers in private equity. Their responsibilities span capital raising, deal execution, portfolio management, and exit strategies. Through a well-structured compensation model of management fees and carried interest, GPs earn outsized rewards-but only with outstanding performance. Their role demands strategic thinking, legal and financial acuity, and steadfast alignment with LPs. A successful GP builds not only a fund, but also a reputation and future opportunity pipeline.

GPs benefit from pass-through taxation-fund income is reported on personal tax returns. General Partners are typically taxed on their share of profits (carried interest) as long-term capital gains. Management fees, however, are taxed as ordinary income.

No, General Partners have unlimited liability. In a typical limited partnership, general partners (GPs) are personally and jointly liable for the fund's obligations. Conversely, LPs enjoy limited liability.

GPs raise capital by designing an investment strategy, marketing it to potential LPs (such as pension funds, endowments, and high-net-worth individuals), and securing commitments through presentations, track records, and relationship-building.

GP duties include fund structuring, portfolio management, legal oversight, financial reporting, exits, and fiduciary responsibilities, along with establishing future fundraising credibility.