Equity management

Equity management

ESOP Management

ESOP Management- Fund management

Liquidity Solutions

Liquidity Solutions - Fund managementESOP Consulting

- Fund managementFund Management

For high-growth companies, ESOPs have become one of the most strategic tools for retention and long-term value creation. But in India’s private-market context, the real success of ESOPs depends on a company’s ability to offer liquidity. Grant design may bring people in, but liquidity is what keeps them invested, literally and emotionally.

According to our Qapita Survey 2025;

India:

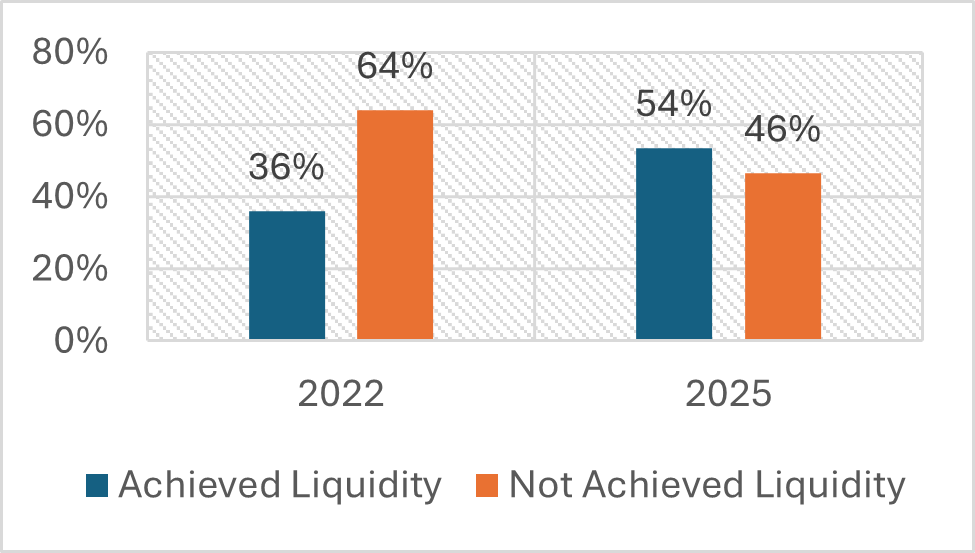

54% of unlisted companies in India reported achieving liquidity, indicating a favourable environment for secondary transactions and employee exits. This reflects growing market confidence and the maturation of equity ecosystems that supports broader participation and value realization.

Over $1.8 billion in employee liquidity across 100+ Indian startups since 2020 signals a clear shift – ESOP liquidity is becoming mainstream. No longer limited to unicorns or IPO-bound firms, even Series B+ startups are structuring secondary sales and buybacks to drive retention and reward.

Southeast Asia:

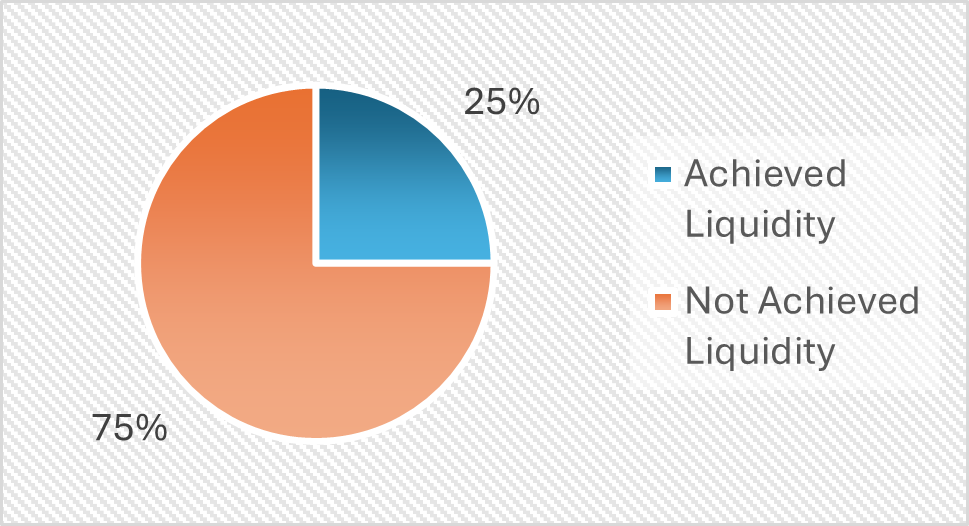

75% of companies in Southeast Asia have yet to offer any form of liquidity to their employees - highlighting a major gap between equity grants and actual value delivery. Only 1 in 4 companies across their lifecycle have enabled liquidity, but that figure is rising sharply from just 13% in 2022. More startups – even as early as Series A and B – are beginning to explore ways to provide employees with tangible cash outcomes from their options.

This article outlines how companies actually deliver liquidity today, why it matters, and what the best companies in India and Southeast Asia are doing.

For employees, ESOPs are meant to be wealth-creating. However, in an unlisted environment, shares cannot be freely sold. Liquidity matters because it:

Our Survey 2025, as stated by ‘Grisha Rathod’ on – Why Unlisted Companiesare linking exercise of options to Liquidity?

By deferring the exercise until the occurrence of a liquidity event, Companies are able to maintain a cleaner cap table, an outcome often preferred by promoters and investors, which in turn supports smoother execution of future funding rounds due to a simplified ownership structure. This mechanism also helps in maintaining maximum number of shareholders as per the Companies Act, while extending the ESOP benefit across the organisation as well.

This structure addresses one of the most significant challenges faced by employees in Unlisted Companies i.e., the illiquidity of equity holdings. In the absence of an active market for such shares, employees are often left with potentially valuable options that offer limited scope for actual value realisation. By linking the exercise of options to a clearly defined liquidity milestone, companies create a structured and time-bound mechanism for employees to unlock the value of their equity, thereby converting notional gains into real, tangible financial outcomes.

Companies increasingly recognize that recurring liquidity events deliver

Today, investors themselves encourage recurring liquidity because it reduces pressure on salaries and ensures stability in senior leadership retention.

Going public remains the cleanest ESOP exit route, but the probability of IPO within the typical employee tenure is low.

Why?

Therefore, companies increasingly accept that IPO cannot be the only exit mechanism for employees.

However, when companies do list, ESOP outcomes are significant. Examples include:

- Zomato: Employees who exercised options at a nominal price (often ₹1 – ₹10 per share) saw massive upside when shares listed at ₹76 and later appreciated further;

- Nykaa: Exercise prices were a fraction (approx. 40 to 50 rupees) of the IPO listing price (approximately 185 to 190 rupees post adjustment for bonus issue), resulting in a multi-fold returns for long-term employees;

- Aditya Info-tech: ESOPs granted just one year prior to IPO, exercise prices were a fraction of the IPO price, resulting in multi-fold returns for long-term employees. The IPO listing price was Rs. 675 and still growing at a staggering rate to now priced at Rs.1645 (13th Nov 2025)

Yet the timeline to listing is too long for most startup employees.

Secondaries have become the default liquidity mechanism for high-growth companies, especially Series C and beyond.

A secondary occurs when:

Market Trend:

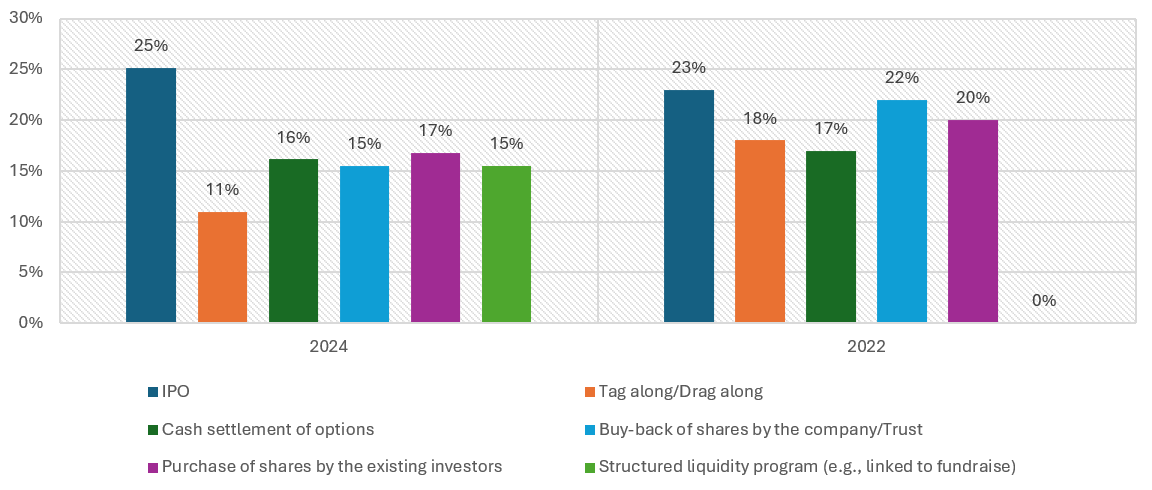

In 2025, IPO emerged as the most cited liquidity alternative (26%), slightly up from 23% in 2022. Tag along/Drag along saw a notable decline from 18% in 2022 to 11% in 2025. Cash settlement of options remained consistent across years at around 16-17%. Buy-back of shares by the Company/Trust decreased from 22% in 2022 to 15% in 2025.

Purchase of shares by existing investors also slightly declined to 17% from 20%. Interestingly, 15% of companies in 2025 introduced structured liquidity programs, a new trend not observed in 2022.

Practical Examples:

1. Flipkart: Prior to Walmart's acquisition, early investors including employees holding ESOPs sold shares to new investors like SoftBank and Tencent, providing liquidity to stakeholders without diluting the company anew.

2. Dream11: Kalaari Capital’s partial exit via a secondary sale also allowed employees to benefit from liquidity events from their stock options.

3. Swiggy and Byju’s have also facilitated secondary transactions where employees holding ESOPs secured liquidity by selling shares to new investors during funding rounds or investor exits.

These structured secondaries are clear, compliant, and well-governed—exactly what the modern market demands.

When fundraising or IPO timelines extend, companies proactively organize liquidity events.

Typical models include:

Why companies do this:

Example:

Souled Store: Qapita facilitated liquidity events for ‘The Souled Store’ through its employee share surrender and platform. The Souled Store's ESOP Liquidity event was conducted on Qapita's Liquidity Module.

Buybacks are governed by Section 68 of the Companies Act and are subject to:

Because selective buybacks for only ESOP holders are generally not permitted, most unlisted companies avoid statutory buybacks unless they are late-stage or profitable.

Beyond rewarding employee loyalty, it’s a strategic move that reflects financial stability and enhances a company’s market credibility.

Examples from India:

1. Swiggy: Conducted a $65 million ESOP buyback in July 2024, enabling employees to convert options into real wealth amid slowing funding activity.

2. Urban Company: Executed a $24 million buyback in May 2024 for vested-options holders.

These companies signal a strong employee-first culture by doing repeated programs.

To avoid statutory complications, many companies adopt cash settlement clauses in ESOP schemes.

Benefits include:

Example:

Flipkart: Cash settlement of options in ESOP schemes, such as those adopted by Flipkart, is a practical and clean liquidity mechanism that helps avoid statutory complications like buyback tax and cap-table dilution. The benefits include controlled liquidity, flexibility to use an internally determined Fair Market Value (FMV), and direct payouts to employees rather than requiring share transactions.

In 2013, Red Bus, India’s largest online bus ticketing platform, was acquired bythe Ibibo Group for $135 million. While the deal was lauded as a milestone for the Indian startup ecosystem, it became a textbook example of the need for transparency and robust structuring in ESOP (Employee Stock Option Plan) agreements.

RedBus had reserved about 10% of its equity for ESOPs, but only around 22 of 150 employees in core roles were actually granted options by the time of the acquisition. Their ESOP vesting followed a Back-ended vesting schedule.

The acquisition, however, led to turmoil. Many employees and even senior managers found themselves disappointed, as they discovered that their ESOPs did not trigger accelerated vesting at the moment of the sale. Some believed they would receive a windfall, but instead, only vested options were honoured, and in some cases, unvested options were converted to those of the acquirer (Ibibo), often with restrictions.

The resulting dissatisfaction led to a wave of resignations and criticism of how ESOPs were managed and communicated. The Red Bus acquisition underlined the importance of:

From our experience across India, Singapore, the Middle East, Australia, and growth markets, successful ESOP programs share four characteristics:

1. Liquidity is planned upfront

Best-in-class ESOP schemes clearly articulate the company's liquidity framework. Liquidity is not an afterthought.

2. Liquidity is recurring

Companies run annual or biennial employee liquidity windows regardless of fundraising cycles.

3. Communication is constant and transparent

Employees understand value creation, valuation methodology, taxes and exit mechanisms.

4.Cap-table discipline is maintained

Companies use structured secondary events, cash settlements, and controlled windows to ensure stability.

5.Conclusion: Liquidity Is No Longer Optional

In today’s talent market, liquidity is the core of the ESOP value proposition, not an ancillary consideration. Companies that deliver liquidit

Share value with the people who create it

Whether via IPO, strategic sale, secondaries, buybacks, or cash settlement, the goalremains the same: turn equity into real, meaningful wealth for employees.