Equity management

Equity management

ESOP Management

ESOP Management- Fund management

Liquidity Solutions

Liquidity Solutions - Fund managementESOP Consulting

- Fund managementFund Management

A Unified View Across Companies Act, SEBI Regulations, and Tax Laws. One of the most underestimated risks in ESOP design is not valuation, dilution, or vesting; it is misalignment of employee eligibility across laws.

As companies move through their lifecycle from unlisted to listed, and sometimes back to unlisted, the definition of who qualifies as an “employee” for ESOP purposes changes materially. Add tax treatment into the mix, especially where consultants or non-traditional roles are involved, and the risk multiplies.

This blog brings together company law, securities regulation, and tax into a single, connected framework, because ESOPs do not operate in silos, even though regulations often do.

An ESOP grant simultaneously touches:

Most implementation errors occur when companies optimise for one lens and ignore the others.

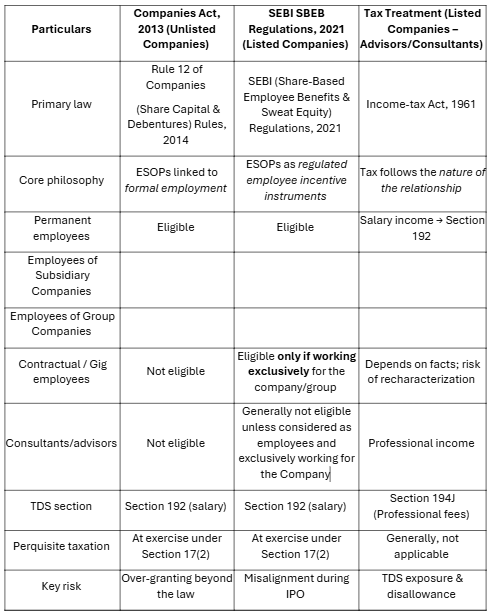

Before diving into the implications of listing or delisting, it is essential to clearly compare how each framework defines “employee”.

On paper, the table looks straightforward. In practice, these regimes collide during corporate transitions, especially listing and delisting.

Let us now connect the dots.

ESOP schemes are drafted when the company is unlisted, following the Companies Act framework. The problem arises because SEBI eligibility is not a continuation of the Companies Act, it is a reset.

IPO-ready companies should design ESOPs as if SEBI already applies, even when legally unlisted.

Delisting is often misunderstood as a compliance relief. From an ESOP standpoint, it is anything but.

Delisting plans must include an ESOP exit and liquidity strategy, not just a shareholder one.

This is where company law optimism meets tax reality.

If consultants are granted equity-linked benefits:

The question “Who is an employee?” is the question every Company Must Ask?

Defining who qualifies as an “employee” for ESOP purposes is no longer a drafting exercise; it is a strategic decision with legal, regulatory, and tax consequences that unfold over time.

As companies grow, list, delist, or reconfigure their workforce models, the real challenge is not whether ESOPs are offered, but whether the framework can withstand regulatory transitions and scrutiny.

Before finalising or continuing with any ESOP structure, it may be worth pausing to ask:

There are no universal answers. But asking the right questions early is often the difference between an ESOP that builds trust and one that has to be reworked under pressure.