Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Profits Interest Units (PIUs) have become a popular form of equity compensation, especially within Limited Liability Companies (LLCs) and partnerships. As a startup founder, you might be exploring various ways to incentivize and retain key employees while aligning their interests with your company's long-term success with limited funds. PIUs offer a unique solution by granting recipients a share in the future profits and appreciation of the company without requiring an initial capital investment.

This blog aims to provide you with a comprehensive understanding of profits interest units, their tax treatment, and their implications for startups. Keep reading to learn more.

A profits interest is a form of equity compensation offered by LLCs and partnerships to employees and service providers, granting holders a share in future profits. However, it often has a liquidation threshold, requiring the company to reach a specific level of profitability before the holder can receive proceeds.

As the company's value grows, so does the value of the profits interest, aligning the holder's interests with the company's success. By granting profits interest units, you are investing in your employees' future. This incentivizes them to contribute to the company's growth and greater profitability. Unlike traditional equity, profits interest units don't dilute existing owners' shares and can offer significant tax advantages.

A key feature of the profits interest grant is its focus on future benefits. Holders only receive a share of profits and appreciation generated after the date of grant. This means they have no claim to the company's existing assets or profits, making profits interest an effective tool for motivating employees to drive the company forward with their personal performance.

A key feature of PIUs is the liquidation threshold. This threshold determines the point at which profits interest holders start to receive distributions from the company. The liquidation threshold is usually established based on the company's valuation at the time the PIUs are issued. This means that the recipient of the PIUs will only start to receive distributions once the company's value exceeds this initial threshold.

The liquidation threshold has a significant impact on the value of the PIUs. Since the threshold represents the company's value at the time of the grant, any increase in the company's value beyond this point will be shared with the profits interest holders. This aligns employee interests with the company's long-term success, as they will only benefit if the company grows and becomes more valuable.

Let's consider an example to illustrate the concept of the liquidation threshold:

Suppose your startup grants PIUs to an employee when the company is valued at $10 million. The liquidation threshold is set at $10 million. Over the next few years, the company grew, and its value increased to $15 million. At this point, the profits interest holders will start to receive distributions based on the $5 million increase in value (i.e., $15 million - $10 million). In this scenario, the employee benefits from the company's growth and is incentivized to contribute to its continued success.

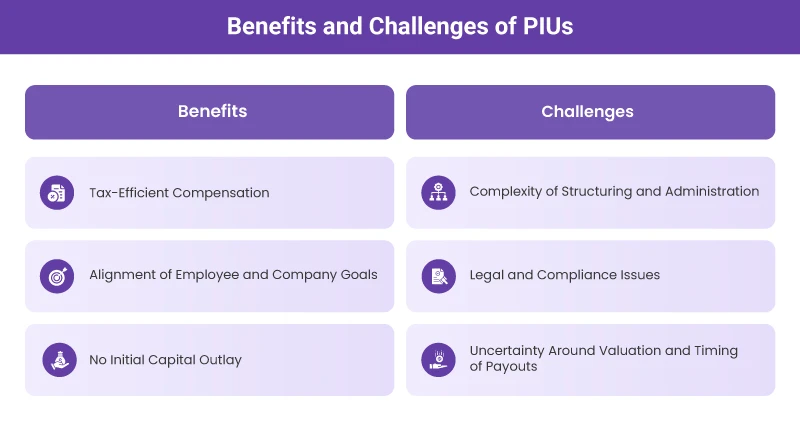

While Profits Interest Units (PIUs) provide several advantages, they also come with certain challenges. Let's explore their benefits and challenges further.

1. Tax-Efficient Compensation: Unlike traditional stock options, PIUs can be structured to avoid immediate payroll tax obligations on the grant date. Instead, taxes are typically deferred until there is an actual profit or sale, often qualifying for long-term capital gains treatment. This can result in lower taxation rates compared to ordinary income tax, making PIUs an attractive option for both companies and employees.

2. Alignment of Employee and Company Goals: PIUs align employee incentives with the company's long-term success. Since PIUs are tied to the future profits and growth of the company, employees are motivated to contribute to the company's success. This alignment creates a sense of commitment, as employees benefit directly from the company's financial performance.

3. No Initial Capital Outlay: PIUs do not require employees to make an initial capital investment, unlike traditional equity. This makes PIUs accessible to a broader range of employees, including those who might not have the financial means to purchase stock options upfront. This feature can help attract and retain top talent who may prefer equity compensation with no upfront cost.

4. Significant Upside Potential: Since PIUs are tied to the future appreciation of the company's value, employees can potentially realize significant gains if the company performs well. This potential for high returns, combined with the lack of initial investment, makes PIUs an appealing form of compensation for employees who are confident in the company's future.

1. Complexity of Structuring and Administration: One of the primary challenges associated with PIUs is the intricate process of structuring them. This includes setting appropriate liquidation thresholds, vesting schedules, and distribution mechanisms. Administering PIUs requires ongoing tracking and accurate accounting, which can be resource-intensive. Ensuring that all these elements are correctly implemented and maintained can be a significant burden for startups.

2. Legal and Compliance Issues: Issuing PIUs involves navigating a complex landscape of partnership and tax laws. Compliance with these rules is vital to stay clear of legal issues or unfavorable tax consequences. Companies must be diligent in understanding and adhering to the relevant laws, which can be challenging without expert legal and tax advice.

3. Uncertainty Around Valuation and Timing of Payouts: Valuing PIUs can be particularly challenging, especially for startups or private companies where market value is not readily available. This uncertainty can complicate the determination of the Fair Market Value (FMV) for accounting and tax purposes. Additionally, the timing of payouts can be unpredictable, depending on the company's financial performance and exit events. This unpredictability can make it difficult for both the company and the recipients to plan.

When considering equity compensation options for your startup, it is important to understand the differences between profits interest and capital interest.

1. Profits Interest: One of the key advantages of profits interest is that it typically requires no initial capital contribution from the recipient. This makes it an attractive option for employees who may not have the means to invest upfront. By granting profits interest units (PIUs), you can offer equity compensation without requiring employees to make a financial investment.

2. Capital Interest: In contrast, capital interest often requires a financial contribution from the recipient. This contribution represents a share of the company's current value or assets. Employees who receive capital interest are essentially buying into the company, which can be a barrier for those who do not have the financial resources to make such an investment.

1. Profits Interest: Profits interest holders generally do not have voting rights, as their interest is tied to future profits rather than actual ownership interest. This means that while they benefit from the company's growth, they do not have a say in company decisions.

2. Capital Interest: Capital interest holders typically have voting rights proportional to their ownership stake. This allows them to influence company decisions and participate in governance. The ability to vote can be an important consideration for employees who want to have a say in the company's direction.

1. Profits Interest: Profits interest holders only share in profits that accrue after the grant of the PIUs. This means they benefit from the company's growth rather than its existing assets. The distribution of profits is tied to the future success of the company, aligning the employee interests with the company's goals.

2. Capital Interest: Capital interest holders are entitled to a share of both current and future profits based on their ownership percentage. This means they benefit from the company's existing assets as well as its future growth. The distribution of profits is more immediate and comprehensive for capital interest holders.

1. Profits Interest: Profits interest is often treated as a capital gain upon sale, provided certain conditions are met. This can help ensure lower taxation rates compared to ordinary income tax. The tax treatment of PIUs can be advantageous for both companies and employees, making it a tax-efficient type of equity compensation.

2. Capital Interest: Capital interest may be subject to taxes as ordinary income or capital gains, depending on the circumstances. This can probably result in higher tax liabilities compared to profits interest. The tax implications of capital interest need to be carefully considered to avoid unfavorable tax consequences.

1. Profits Interest: Profits interest holders face less risk since they do not invest upfront and only share in future profits. Their downside is limited to not realizing potential gains if the company underperforms. This makes profit interest a lower-risk option for employees.

2. Capital Interest: Capital interest holders have more at stake, as their investment includes both current assets and future growth. This means they could lose their initial investment if the company underperforms. The higher risk exposure of capital interest needs to be weighed against its potential benefits.

The Internal Revenue Service (IRS) has particular rules governing the taxation of PIUs, and it's important to be aware of these to avoid unexpected tax liabilities.

When your employees sell profits interest units, the gains come under the purview of capital gains tax. The tax treatment depends on the holding period of the PIUs:

1. Short-Term Capital Gains: If your employees sell the PIUs within one year of receiving them, the gains will be regarded as short-term capital gains, taxable at the prevailing ordinary income tax rate. This rate can be significantly higher than the long-term capital gains rate.

2. Long-Term Capital Gains: If your employees hold the PIUs for more than one year before selling them, the gains are considered long-term capital gains. These gains are taxed at a lower rate, which can be advantageous for them. The long-term capital gains tax rate is generally lower than the ordinary income tax rate, making it beneficial to hold the PIUs for at least one year before selling.

Let's consider an example to illustrate the tax treatment of PIU gains on sale: Suppose your company grants PIUs to an employee when the company's value is $10 million. After holding the PIUs for two years, the company's value increases to $15 million, and the employee decides to sell their PIUs. The $5 million increase in value is considered a long-term capital gain, and they will have to pay tax as per the long-term capital gains rate on this amount.

The IRS has established safe harbor rules to protect the recharacterization of profits interest as taxable compensation. These rules help ensure that profits interest is regarded as a capital gain instead of ordinary income, provided certain conditions are met.

To qualify for safe-harbor protection, the following conditions must be met. By meeting these conditions, you can ensure that the profits interest is treated as a capital gain, which can result in lower tax rates for your employees.

1. No Capital Account: The recipient of the profits interest must not have a capital account associated with the interest.

2. No Distributions: The recipient must not receive any distributions related to the profits interest within two years of receiving it.

3. Substantial Risk of Forfeiture: The profits interest should be subject to the risk of forfeiture. This means that the recipient's right to the interest is contingent on future performance or other conditions.

To comply with the IRS safe-harbor rules, you should clearly document the grant of the profits interest, including the terms and conditions. You should also track and monitor any distributions related to the profits interest to ensure that they comply with the safe-harbor rules.

As a startup founder, it's essential to help your employees understand the tax implications of PIUs and provide them with practical tax planning strategies.

1. Hold for Long-Term Capital Gains: If the underlying assets of the PIUs are primarily long-term capital assets, holding them for more than one year before selling can qualify the employees for lower long-term capital gains tax rates.

2. Strategic Disposition: Your employees should carefully consider the timing of selling their PIUs to optimize tax consequences. Factors such as the overall tax bracket, the nature of the underlying assets, and the potential for future appreciation should be taken into account.

3. Qualified Small Business Stock (QSBS) Exclusion: If the PIUs represent ownership in a qualified small business, your employees may be eligible for a significant tax exclusion on the gain from the sale of those shares.

4. Plan for Liquidity Events: Help your employees plan for potential liquidity events, such as the sale of the company or an initial public offering (IPO). Understanding the timing and tax implications of these events can help them make informed decisions about when to sell their PIUs and how to manage their tax liability.

To understand the real-world implications of holding PIUs, let's consider a detailed example of how PIUs might be treated in the exit scenario of company sales.

Your startup, valued at $10 million, grants PIUs to an employee. The liquidation threshold is set at $10 million, which means the employee will only start to receive distributions once the company's value exceeds this threshold.

Initial Grant

Over the next few years, your startup will experience significant growth, and its valuation will increase to $20 million. During this period, the employee continues to hold their PIUs, which are now tied to the future profits of the company.

After a few years, your startup is acquired by a larger company for $20 million. Here's how the liquidation threshold and distribution of profits would work in this exit scenario:

Assuming the employee's PIUs represent a 10% share of the company's future profits, their distribution would be calculated as follows:

In this scenario, the employee receives $1 million from the sale of the company, which represents their share of the profits above the liquidation threshold. This distribution is a direct result of the company's growth and the value created after the grant of the PIUs.

Understanding both the benefits and tax implications of Profits Interest Units (PIUs) is crucial for making informed decisions about equity compensation in your startup. PIUs offer a tax-efficient way to align employee incentives with the company's long-term success, but they also come with complexities that need careful management.

At Qapita, we specialize in helping startups manage their equity compensation plans, including the administration of PIUs. Our platform is designed to simplify the process, ensuring legal and tax compliance while providing valuable insights into your equity structure. We are proud to be rated as the #1 Equity Management Software by G2, thanks to our commitment to innovation, trusted partnerships, and robust customer support.

If you need assistance with managing your equity compensation plans or have questions about implementing PIUs, our experts are here to help. Contact Qapita today to learn more about how we can support your company's equity management.

Profit before interest and tax (PBIT) is a company's earnings from core operations before deducting interest expenses and taxes. It's a broader measure of profitability that shows how well a business generates profit from its primary activities, regardless of its capital structure or tax obligations. PBIT helps founders assess operational efficiency and compare performance across companies.

A profits interest is a form of equity compensation in LLCs and partnerships, granting recipients a share in future profits and appreciation without requiring an initial capital investment. While it shares some characteristics with securities, its classification can vary depending on specific terms and regulatory context.

To profit from interest rate hikes, consider investing in assets like savings accounts, money market funds, and short-term bonds, which offer higher returns as rates rise. Additionally, bank stocks and financial institutions may perform better in a high-interest environment.

A profits interest in an LLC is a type of equity compensation that gives the holder a share in the company's future profits and appreciation without an upfront capital contribution. It typically has no claim on existing assets or past profits. This structure aligns recipients' interests with the LLC's growth, making it an attractive tool for startups to incentivize key employees or partners.