As a startup founder, understanding the W-2 form is vital for managing your financial responsibilities and ensuring tax compliance in the US. Without this form, it can be difficult for your employees to determine their correct tax liabilities, potentially leading to errors and delays. And for you, hefty penalties.

This blog covers everything about Form W-2, right from what information it includes, how to read it to its significance for your startup. Keep reading to know more.

What is a W-2 form?

The W-2, also known as the 'Wage and Tax Statement,' is a tax form that reports the annual wages and taxes withheld from the paychecks of your employees throughout the year. As an employer, you are required to send this to your employees, the Internal Revenue Service (IRS), and the Social Security Administration (SSA) every year. It allows these agencies to cross-check the income and tax information reported by both the employer and the employees, ensuring accuracy and compliance with tax laws.

The W-2 form provides a detailed breakdown of an employee's compensation from a specific job, including important information about gross wages or salaries, federal and state taxes withheld, and Social Security and Medicare taxes deducted. However, it is not issued to independent contractors or self-employed workers.

When to issue a W-2 form?

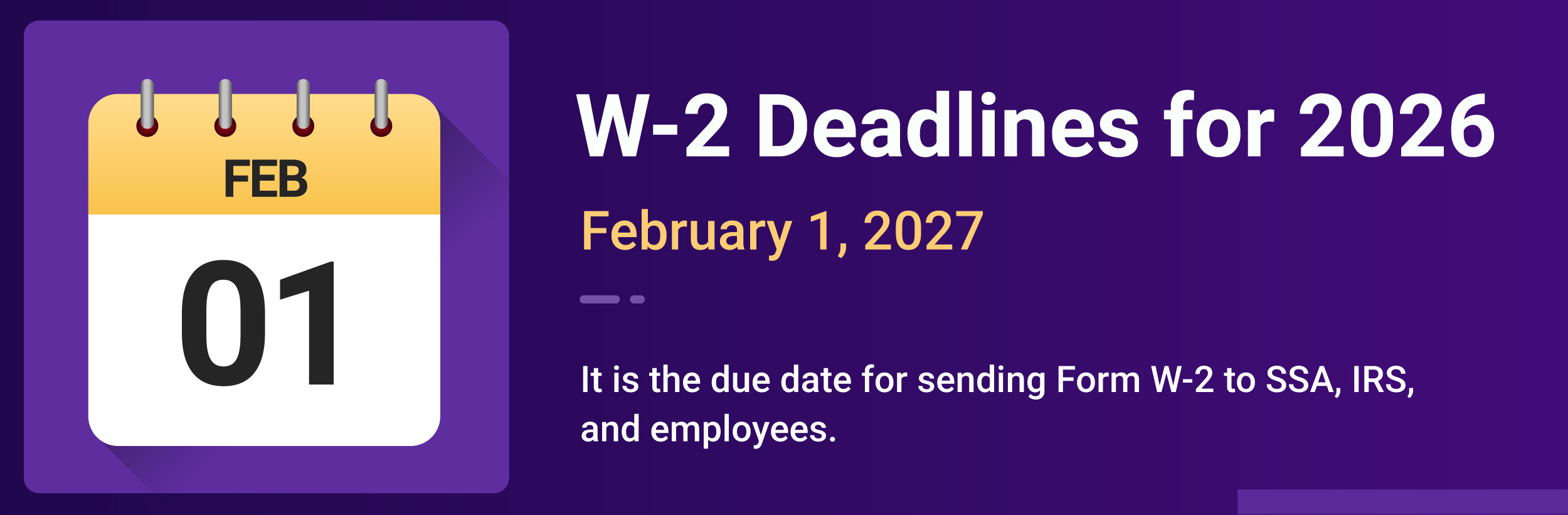

According to IRS regulations, you must send W-2 forms to your employees by January 31 every year. This timeline is applicable regardless of whether the employee is still employed or is no longer working with the company.

If you fail to distribute the W-2 forms by the deadline, you may face penalties and fines from the IRS

As of 2024, the penalties can range from $60 to $310 per form, depending on how late the forms are filed

In extreme cases, if the IRS determines that the delay in filing was because of deliberate disregard of the law, the penalty can be as high as $630 per form.

For employees who leave your company before the year ends, you can distribute their W-2s any time before but no later than the end of January of the following year.

If an employee requests their W-2, you must provide them with a copy within 30 days of the request or 30 days of their final paycheck, whichever comes later.

What are the important deadlines for filing W-2s?

Here are the deadlines for employers to submit W-2 forms to the SSA and state tax agencies:

SSA and IRS deadline: You must submit W-2 forms to the SSA and IRS by January 31st each year. This timeline applies to both paper and electronic filings. The SSA uses the information from the W-2 forms to calculate employees' Social Security benefits and track their income history

State tax agencydeadlines: In addition to the SSA, you must also submit W-2 forms to state tax agencies. The deadlines for state submissions vary, but most states follow the same deadline as the SSA. However, some states may have different deadlines, so you must check with your state's tax agency for specific requirements

Electronic filing deadline: If you are filing W-2 forms electronically, the deadline is also January 31. Electronic filing is mandatory for employers who file 250 or more W-2 forms. You can file electronically through the SSA's Business Services Online (BSO) portal or through a third-party provider

Extensions and penalties: If you need more time to file your W-2 forms, you can request a 30-day extension by submitting Form 8809 to the IRS by January 31. However, this extension does not apply to the deadline for furnishing W-2 forms to employees. If you miss the deadline, you may face penalties, as discussed in the previous section

What details does form W-2 contain?

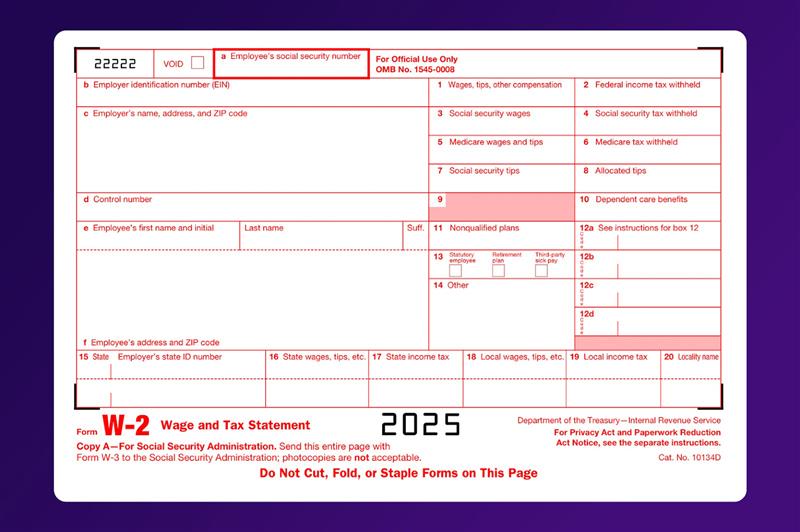

Form W-2 is available on the IRS website and features distinct boxes, each covering different details related to the employee's income and tax obligations. Here are the important sections of Form W-2:

Identifying information (Boxes A-F): These boxes cover essential details such as the employee and employer names and addresses, the employee's Social Security number, and the employer's Employer Identification Number (EIN) and state ID number

Federal tax withholding:

Box 1 details the employee's total taxable income, including wages, salary, tips, and bonuses

Box 2 shows how much federal income tax your company withheld from your employee's paychecks throughout the year

Social security tax details:

Box 3 covers the earnings subject to Social Security tax

Box 4 showcases the specific amount of Social Security tax deducted from the employee's pay

Medicare tax information:

Box 5 outlines the income subject to Medicare tax

Box 6 discloses the precise amount of Medicare tax withheld from the employee's pay, with the employee's share set at 1.45%

Tip income reporting (Boxes 7-8): These boxes describe any tip income reported and are subject to taxation

Dependent care benefits (Box 10): It reports any dependent care assistance you provided to the employee throughout the year, if applicable

Deferred compensation details (Box 11): This box specifies any deferred compensation received by the employee through a non-qualified plan

Miscellaneous compensation and adjustments (Box 12): It presents various forms of compensation or reductions from taxable income. Each is denoted by a single-letter or double-letter code, potentially including contributions to retirement plans like a 401(k)

Retirement plan and sick pay reporting (Box 13): This box comprises sub-sections to report pay exempt from federal income tax withholding for employer-sponsored retirement plans and sick pay administered by a third party

Additional tax insights (Box 14): Employers can include supplementary tax information not accommodated elsewhere on the W-2 form, such as state disability insurance taxes and union dues

State and local tax daata (Boxes 15-20): The final six boxes pertain to state and local taxes, detailing the income subject to these taxes and the corresponding withholdings

Related tax documents

Along with W-2, several other forms play an important role in the tax filing process:

Form W-3 (Transmittal of wage and tax statements): When filing W-2 forms with the SSA, you must also submit Form W-3. This form summarizes all the W-2 forms issued to employees, providing the SSA with a comprehensive overview of the total wages and taxes reported.

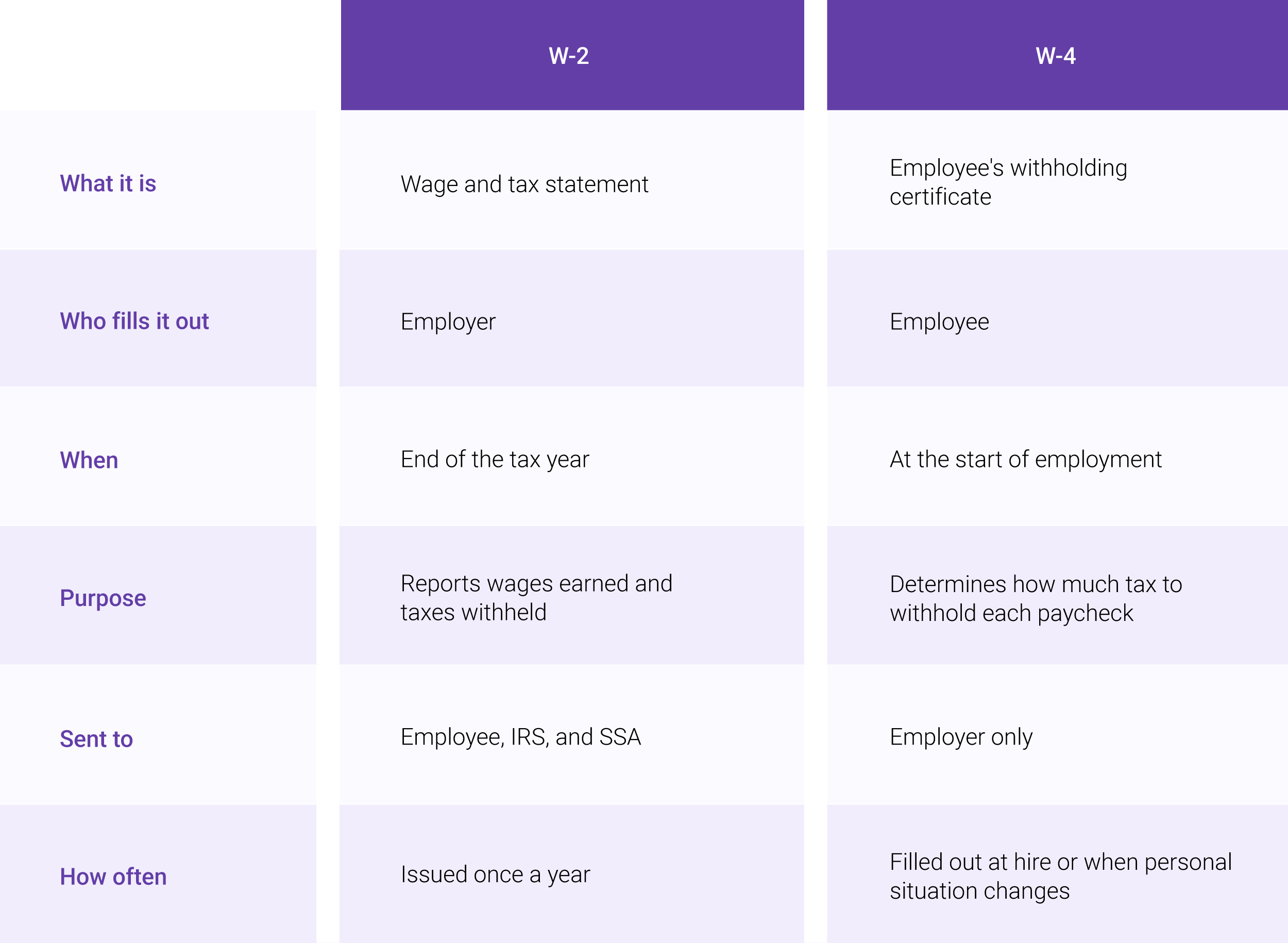

Form W-4 (Employee's withholding certificate): Employees complete Form W-4 when they start a new job. This helps employers determine the proper amount of federal income tax to withhold from their paychecks. The information on the W-4 is used in combination with the W-2 to ensure accurate tax withholding and reporting.

Form 1099 (Information returns): Form 1099 is used to report payments made to independent contractors and other individuals who are not considered company employees for tax purposes. There are various types of 1099 forms, such as the 1099-MISC for miscellaneous income and the 1099-NEC for non-employee compensation.

Who receives a W-2 form ?

As an employer, you are required to issue a W-2 form to every employee who was paid wages, salaries, or other compensation during the tax year. Not everyone who works for your startup will receive a W-2. Understanding who qualifies is important to avoid misclassification penalties.

You must issue a W-2 form to an employee if:

You paid them $600 or more in wages during the tax year

You withheld any federal, state, or local income tax from their paycheck, regardless of the amount paid

You withheld social security or medicare taxes from their wages

Understanding the copies of Form W-2

There are different copies of Form W-2 for different purposes. Each copy serves a specific function in the tax reporting process, ensuring compliance and transparency for you and your employees.

Copy A: Social security administration (SSA): Copy A of the W-2 form is the official copy that you, as the employer, must file with the SSA. The agency uses the information on this form to determine an employee's future social security benefits

Copy B: Employee's federal tax return: Copy B is for the employee's federal tax return. It provides the necessary information for employees to accurately report their income and calculate their federal income tax liability

Copy C: Employee's records: Copy C is for the employee's personal records. It serves as a reference for the employee to verify the accuracy of the information reported on their W-2 form and to keep track of their earnings and tax withholdings

Copy D: Employer's records: Copy D is for the employer's records. It should be retained for at least four years after the due date for filing the related tax return to help answer any questions from the IRS or the SSA

Copies 1, 2, and state copies: Depending on your state's requirements, you may need to provide additional copies of the W-2 form to your employees and state tax agencies. These copies are typically labeled as Copy 1, Copy 2, and State Copies

What is a W-2 employee?

Understanding the distinction between W-2 employees and independent contractors is crucial for you to ensure proper classification and compliance with tax regulations.

W-2 employees: W-2 employees are individuals who perform services for the company under your direction and control. They are considered employees for tax purposes and are issued W-2 forms at the end of the year. These employees have taxes withheld from their paychecks by your company. You are accountable for offering them benefits like health insurance and paid time off (where applicable) and adhering to labor laws

Independent contractors: Independent contractors are self-employed individuals. They provide services to your enterprises but are not considered your employees. These contractors must pay their taxes, including self-employment taxes. They receive Form 1099-NEC or other relevant 1099 forms instead of W-2 forms, provided they earned more than $600 in a year from you.

The key difference between W-2 employees and independent contractors is the level of control and independence in their work relationship with the company. W-2 employees work under your direct supervision, while independent contractors have more control over how they work and are not entitled to employee benefits.

What is the difference between 1099 and W-2 Forms?

Here is a comparative analysis of the W-2 and 1099 forms:

Purpose: W-2 forms are used to report wages and tax withholdings for employees. On the other hand, 1099 forms are used to report payments made to independent contractors and non-employees

Recipients: W-2 forms are issued to employees who work directly for the company. On the other hand, independent contractors and non-employees who provide services to the company receive 1099 forms

Tax Withholding: Employers withhold taxes from W-2 employees' paychecks and report these withholdings on the W-2 form. However, employers do not withhold taxes from payments to 1099 contractors, who are responsible for paying their taxes

Tax Reporting: Employees receive W-2 forms to file their income taxes, and employers must also submit copies to the IRS and Social Security Administration. At the same time, independent contractors use 1099 forms to report their income and pay taxes on their earnings

Difference between a w2 and w4

The W-4 (employee's withholding certificate) is filled out by your employee when they join your company. It tells you how much federal income tax to withhold from their paycheck based on their filing status, dependents, and personal tax situation. Employees can update their W-4 at any time if their financial situation changes.

Here is a quick breakdown:

Can an individual get both a W-2 and a 1099?

While it is uncommon, there are some situations where an individual might receive both a W-2 and a 1099 form within the same tax year.

Concurrent employment and contracting roles: One scenario is if an individual performs duties as both an employee and an independent contractor or freelancer simultaneously for your company. This situation can arise when employees take on additional work or provide services outside of their normal job description. For example, if you have an employee who also designs websites for your startup on the side, the payment for the website design would require a 1099-NEC (Non-Employee Compensation). The employee's regular wages would still be reported on a W-2

Separate employment and contracting roles: Another situation is where a worker held these two jobs at separate times during the same tax year for you. This could happen if you hired an individual as an independent contractor who then later transitioned to an employee role within the same year. In this case, the individual would receive a 1099 for their independent contractor earnings and a W-2 for employee wages

When an individual receives both a W-2 and a 1099 in the same year, they must report the income from both forms on their individual tax return. The W-2 income is reported first, just as if it were the only income. The 1099 income is then added as self-employment income, as independent contractors must pay portions on behalf of both the employee and the employer for Social Security and Medicare taxes.

Why correct worker classification is important for startups?

Misclassifying workers can lead to significant legal and financial implications for your startup. Here are the different aspects of proper worker classification:

Legal implications

Employee Rights: Employees are entitled to various rights and benefits, such as minimum wage, overtime pay, and access to programs like health insurance and retirement plans. Incorrectly classifying employees as independent contractors can result in violations of labor laws and potential legal action

Tax Compliance: The IRS and state tax authorities have specific guidelines for worker classification. Misclassifying workers can lead to tax penalties, fines, and audits, as well as potential legal liabilities for unpaid taxes and benefits

Financial implications

Tax Obligations: Employers must withhold and pay payroll taxes for employees, including Social Security, Medicare, and federal income taxes. Misclassifying employees as independent contractors shifts this tax burden to the worker, potentially leading to tax evasion charges

Benefit Costs: Providing benefits to employees can be a significant cost for startups. Misclassifying employees as independent contractors to avoid offering benefits can result in penalties, back pay for benefits owed, and damage to your company's reputation.

Role of W-2 and 1099 Forms

W-2 Forms: W-2 forms play a crucial role in documenting employee earnings and tax obligations, and ensuring compliance with tax laws

1099 Forms: Properly issuing 1099 forms helps track payments to contractors and ensures accurate tax reporting

Implications on W2 Form in case of employee equity

When employees exercise their stock options or vest their RSUs, the fair market value of the shares on the date of exercise is considered taxable income.

This amount must be reported on the employee's W-2 form as wages, tips, and other compensation (Box 1)

If the income is subject to Social Security tax, it is reported in Box 3 (Social Security wages), and if subject to Medicare tax, it's in Box 5 (Medicare wages and tips)

Employers often report this income separately in Box 14 (Other) to help employees understand how much of their reported income is attributable to equity awards

State and local income tax withholding is also reported in Box 16 (state wages) and Box 18 (local wages)

Deferred payout of an RSU award or RSU payout after retirement may be reported in Box 11

Nonqualified Stock Option (NQSO) exercise income is reported in Box 12 with code V

Compensation resulting from a Section 409A violation is reported in Box 12 with code Z

Former employees follow similar withholding and reporting requirements as current employees. Income recognized by former employees due to equity plan transactions should be reported on a Form W-2 and is subject to withholding if it results from a non-qualified arrangement

Transactions by nonemployees (Consultants and outside directors)

Compensation income recognized by consultants and outside directors related to equity awards is reported on Form 1099-NEC in Box 1 (nonemployee compensation)

The income is aggregated with any other payments made to the nonemployee during the year

Timing of reporting employee equity

The timing of when employee equity is reported on the W2 form depends on the type of equity compensation. For example, if an employee exercises non-qualified stock options (NQSOs), the income is reported on the W-2 form for the year in which the options were exercised. However, if an employee exercises Incentive Stock Options (ISOs), the income is not reported on the W-2 form until the employee sells or disposes of the shares.

What to do If W-2 is wrong or missing?

Maintaining accurate payroll records and double-checking employee details before issuing W-2s is the best way to avoid these situations altogether.

If the W-2 is incorrect: If an error is spotted, the employee should contact the payroll team immediately. If the original W-2 has already been filed with the SSA, you must issue a Form W-2c (Corrected Wage and Tax Statement) to both the employee and the SSA. If the employee has already filed their taxes using the incorrect W-2, they will need to submit Form 1040-X to amend their return

If the W-2 is missing: If an employee has not received their W-2 by February 2, they should first contact the payroll department to request a reissue. If it is still missing by the end of February, they can call the IRS at 800-829-1040 for assistance. As a last resort, they can file using Form 4852 (substitute for form W-2) to estimate their wages and meet the tax filing deadline

Conclusion

Most tax penalties come from gaps in knowledge and delayed action. Missing a W-2 deadline, misclassifying a contractor, or misreporting equity income are not minor until the IRS notices. By then, what could have been a simple process becomes expensive, time-consuming, and damaging to the trust you have built with your team.

For startup founders juggling a hundred priorities, W-2 compliance is easy to deprioritize, until it is not. The complexity only grows as you hire more employees, bring equity into the picture, and expand across states. What feels manageable at five employees looks very different at fifty. Understanding your obligations now puts you ahead of problems that are far costlier to fix than to prevent.

How Qapita can help your business stay compliant

Managing equity reporting and W-2 compliance can be overwhelming for startup founders, especially when stock options and RSUs add complexity to your tax obligations.

Qapita helps you design, manage, and communicate employee stock plans with clarity and confidence, while keeping your cap table and equity reporting audit ready. From 409A valuations to ASC 718 expense amortization and taxation, Qapita ensures your financial reporting is always compliant.

Qapita's platform is trusted by over 2,400+ companies and 300,000 employee-owners. We offer a comprehensive and configurable solution that is easy to set up with concierge assistance. Our platform provides accurate and secure equity management, making it a single source of truth for private and listed companies.

Your employer may provide your W-2 through a payroll portal or via email with a secure link. If your employer uses a payroll, you can log in to their self-service portal to download it. Or you can also access your W-2 through your IRS Online Account at IRS.gov.

What if I have multiple W-2s from different employers?

You must report income from all W-2s on your tax return. Simply add up the wages and withholdings from each W-2 and report the combined totals when filing. Your tax software or accountant can help you consolidate multiple W-2s accurately.

Is a 1040 the same as a w2?

No, they are two different forms that serve different purposes. A W-2 is issued by your employer and reports the total wages you earned, and taxes withheld throughout the year. A Form 1040 is your personal federal income tax return that you file with the IRS. Think of it this way, the W-2 is the input and the 1040 is the output. You use the information from your W-2 to complete and file your Form 1040.

What is the difference between 1099 and W-2?

The key difference comes down to your employment status. A W-2 is issued to employees whose taxes are withheld and paid by the employer throughout the year. A 1099-NEC is issued to independent contractors and freelancers who are responsible for managing and paying their own taxes. In simple terms, if you work for a company as an employee, you receive a W-2, and if you work as a contractor or freelancer, you receive a 1099.

About Author

Team Qapita

Try Qapita today!

Elevate your equity management with smarter solutions for growth and compliance.

Equity management

Equity management

Equity management

Equity management

Fund management

Fund management