Startups and Individuals tax payers had many expectations from the Budget (now the Finance Act). The Finance Act was able to meet some while it missed a few. The recognition of the Digital Assets, capping of Long Term Capital Gain Surcharge and setting up of the Expert Committee to regulate venture capital (VC) and private equity (PE) investments are some of the positives. The startup community is also eagerly waiting for the RBI to launch the Digital Rupee.

Let's look at the important points affecting startups, investors, and employees:

Direct Tax

Virtual digital asset-defined and taxed

Presently there are no laws or regulations defining cryptocurrencies in India.

Virtual Digital Assets (VDA) have found a place and definition in the Finance Act. They are defined as any information or code or number or token (not being Indian currency or foreign currency), generated through cryptographic means or otherwise, non fungible tokens and other digital assets to be notified by the Central Government.

Both Long Term and Short Term Capital Gain on VDA will be taxed at a flat rate of 30%. No deductions and exemptions will be allowed in computing Capital Gains from Virtual Digital Assets.

Losses from virtual digital asset can't be set off against any other income. Carry forward of these losses won't be allowed. Only the cost to transfer these assets would be allowed as deduction.

Moreover, Loss from the transfer of VDA will not be allowed to be set off against income from another VDA

Gifting of virtual digital assets will be taxed in the hands of the recipient (person receiving the gift).

Transfer of VDA to a resident would attract TDS of 1% on the payment consideration from 1 July 2022

However, the taxation of VDA for the FY2021-22 is still a grey area with experts holding different views

VDA will be taxed at 30% irrespective of the head under which it is covered -- business or profession, capital gain, or other sources.

Writer's Take

The Government is moving cautiously with VDA. As per the latest news, India will frame Cryptocurrency Law after there is a global consensus on regulating these assets.

Till then India is treating Cryptocurrency as an asset and not a Currency since it has not been issued by the RBI.

Income from VDA will be taxed at the same rate income from horse racing and betting is taxed- at Maximum Marginal Rate of 30%. To track every transaction made in cryptocurrency, 1% TDS has been imposed.

The Finance Act allows losses from Speculative Business to be set off with gains from the same. The provision of not allowing losses from VDA to be set off with gains, this goes out to show how the Government treats it as an unattractive instrument.

These changes would entail a drop in Cryptocurrency transactions, especially by small investors and an increase in finding alternatives in grey markets and offshore havens.

The Government is also planning to introduce GST on Cryptocurrency. The stringent laws introduced to tax Crypto give an uncertain environment to Crypto exchanges.

The only plus side is that Cryptocurrency has found a place in the Act and has not been considered illegal.

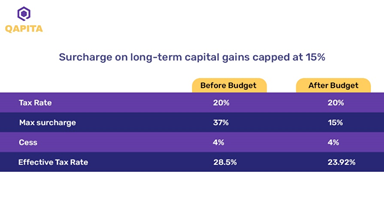

Long term capital gain surcharge capping at 15%

Surcharge is extra tax on income earned by a person exceeding a certain limit.

For Individuals, Long-Term Capital Gain Surcharge on listed equity shares and mutual funds is 15%. On Other assets and unlisted securities this can reach a maximum of 37%. This is because surcharge on unlisted securities on LTCG between Rs.2 crore and Rs.5 crore is 25% and Surcharge on LTCG exceeding Rs. 5 crore is 37%

The Finance Act has now capped surcharge on long term capital gains arising on transfer of any type of assets at 15%

This would treat listed and unlisted securities on a uniform basis. This amendment will benefit investors, startup founders and ESOP holders.

Writer's Take

There were many expectations from the Government to change the basic tax rates, especially in lieu of COVI. The Government has kept the basic tax rates unchanged. With the capping of surcharge on LTCG at 15%, means a 4.6% reduction in the maximum effective tax rate (from 28.5% earlier to 23.92% now).

Bonus stripping to be made applicable to securities and units

Bonus stripping is a mechanism to reduce Capital Gain Tax.

The investor could do so by buying shares when he knows that the company is about to make bonus issue to existing shareholders. The investor then books losses by selling shares of companies' right after bonus issuances.

The Income Tax Act has a provision, to curb this practice in mutual funds. The Finance Act has extended this curb to all securities.

Tax holiday clause for eligible startups

Startups incorporated between 01.04.2016 and 31.03.2022 can qualify as eligible startups and are entitled to certain Income Tax Benefits.

The Finance Act has extended the period of incorporation of startups (eligible for tax holiday by one year unto 31.03.2022

This provision would be beneficial for very few startups as out of 62,000 Department for Promotion of Industry and Internal Trade registered startups in India, only 400 are IMB (Inter-Ministerial Board) certified.

This provision would be beneficial for very few startups as out of 62,000 Department for Promotion of Industry and Internal Trade registered startups in India, only 400 are IMB (Inter-Ministerial Board) certified, i.e. availing the Tax Holiday provision.

One year extension to new manufacturing units

New Domestic manufacturing companies are eligible for an optional concessional rate of tax of 15% under Section 115BAB.

The eligible domestic manufacturing company must be set up and registered on or after 01.10.2019 and commenced manufacturing or production of an article or thing on or before 31.03.2023.

The last date for commencement of manufacturing or production is now extended to 31.03.2024

Withdrawal of concessional rate of dividend from specified foreign companies

At present, dividends received by Indian Companies from their Foreign Subsidiaries are taxed at a concessional rate of 15%.

From Assessment Year 2023-24 onwards, dividends received by Indian companies from their foreign subsidiaries is proposed to be increased to the rate of 30% instead of the current rate of 15%.

10% TDS on benefit or perquisite

A new section has been introduced to include benefits and perquisites received during business and profession

Any benefit or perquisite, whether convertible into money or not, like gift, travel, hospitality, etc., business or profession is to be charged as business income in the hands of the person receiving it. TDS at 10% on such amount will be applicable if the value of such benefits exceeds Rs. 20,000 during the financial year.

Writers Take The new provision has been introduced to widen and deepen the tax base, by covering recipients of these perquisites not reporting these in their ITR.

Policies

Central bank digital currency (CBDC) to be launched

The Reserve Bank of India (RBI) will soon issue a central bank-backed digital currency (CBDC) in FY 2022-23

CBDC is a digital currency issued by the central bank, i.e. the Reserve Bank of India (RBI), and it will be based on "Blockchain and other technologies".

Setting up Digital Banking Units (DBUs)

75 digital banking units (DBUs) in 75 districts across India would be set up through scheduled commercial banks.

In 2022-23, all 1.5 lakh post offices will be connected to the core banking system, enabling financial inclusion and access to accounts through net banking, mobile banking, and ATMs. It will also allow online transfer of funds between post office accounts and bank accounts.

Expert Panel for PE/VC investments

The Government would set up an Expert Panel to suggest measures to review the regulatory framework for the venture capital and private equity industry

Govt. allocated Rs. 283.5 CR to startup India seed fund

The Startup India Seed Fund Scheme (SISFS), set up in April 2021, aims to provide financial assistance to startups for proof of concept, prototype development, product trials, market-entry, and commercialization.

The scheme aims to provide startups with financial assistance at their early stages such as proof of concept, prototyping, product trials, market entry and commercialization.

Rs. 283.5 Cr has been earmarked for the Startup India Seed Fund Scheme (SISFS) in the Union Finance Act 2022 from the Revised estimate of Rs. 100 crore.

Aayushi is a Chartered Accountant by qualification working at Qapita. She is building the Compliance Product at Qapita, to ease the lives of Chartered Accountants and Companies Secretaries. Qapita is a Captable and ESOP Management Platform

Disclaimer: The Article is based on the Relevant Provisions and as per the information existing at the time of the preparation. In no event the author or Qapita will be liable for any direct and indirect result from this Article.

This is only a knowledge sharing initiative. The Author can be reached at aayushi.ajmani@qapitacorp.com

Thank you for reading

About Author

Aayushi Ajmani

Try Qapita today!

Elevate your equity management with smarter solutions for growth and compliance.

Equity management

Equity management

ESOP Management

ESOP Management

Liquidity Solutions

Liquidity Solutions