Equity management

Equity management

ESOP Management

ESOP Management- Fund management

Liquidity Solutions

Liquidity Solutions - Fund managementESOP Consulting

- Fund managementFund Management

Cancelling shares isn't something most companies think about-until they have to. Whether it's cleaning up after a forfeiture, restructuring capital, or wrapping up a buyback, cancellation of shares is a common but often misunderstood process.

Share cancellation is treated as a routine compliance step, but mistakes in the process can create larger problems later, from cap table inconsistencies and failed due diligence checks to regulatory disputes and shareholder conflicts.

In India, cancelling shares involves a defined legal and procedural framework under the Companies Act, 2013, along with additional compliance obligations for listed companies.

Knowing when and how to cancel shares can save you from costly mistakes if you're a founder, finance lead, or someone handling compliance.

In this blog, we'll explain share cancellation, when companies typically do it, and how the process works, and the key legal, financial, and operational considerations involved.

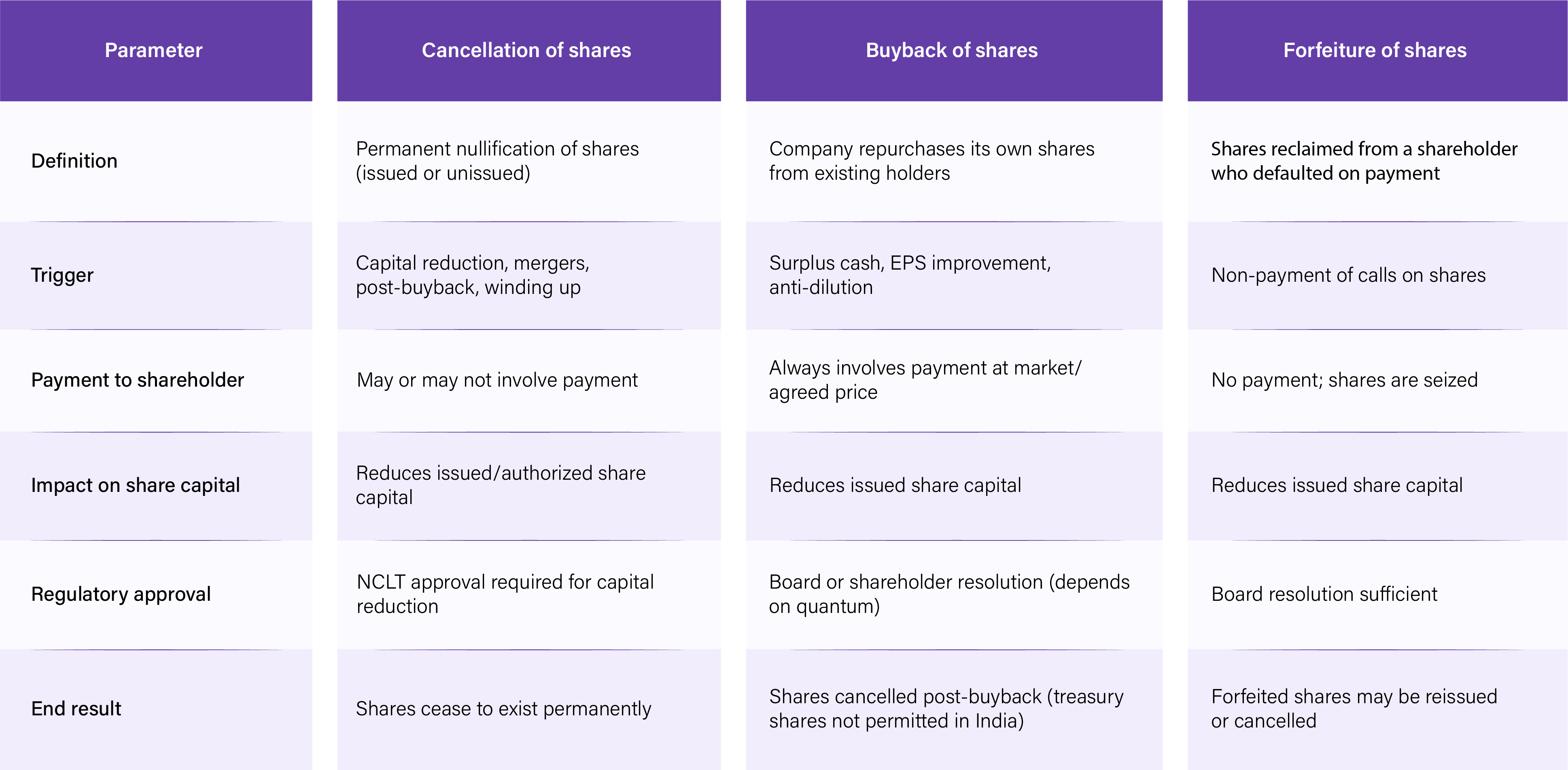

Cancellation of shares refers to the process where a company nullifies its issued or unissued shares, effectively reducing its share capital. When shares are cancelled, they cease to exist, and the rights associated with those shares are terminated. Cancellation of shares can occur due to various reasons such as share buybacks, capital restructuring, mergers, or regulatory compliance.

Companies cancel shares for different legal, financial, and operational reasons depending on the type of corporate action involved.

When a company repurchases its own shares through a buyback, those shares are typically cancelled after the transaction is completed. This reduces the total number of outstanding shares in circulation.

Companies may cancel shares as part of a capital reduction exercise to reorganise their financial structure or eliminate excess capital. In India, this process generally requires approval from the National Company Law Tribunal (NCLT).

During mergers or amalgamations, the shares of the absorbed entity may be cancelled and replaced according to the approved share exchange arrangement between the companies involved.

A company may cancel authorised but unissued shares to reduce its authorised share capital. This limits the number of shares that can be issued in the future without affecting existing shareholders.

During the winding-up process, shares may be cancelled as part of the company’s dissolution and final settlement of assets and liabilities.

Cancellation of shares affects more than just the number of shares a company has outstanding. It also influences compliance, ownership records, financial reporting, and future corporate actions.

1. Capital structure management: Companies may cancel excess, inactive, or repurchased shares to keep their share capital aligned with the company’s current ownership and funding structure.

2. Enhancing shareholder value: Reducing the number of shares in circulation can improve metrics such as earnings per share (EPS) and increase the relative ownership stake of existing shareholders.

3. Supporting corporate restructuring: Share cancellation is commonly used during mergers, acquisitions, capital reduction exercises, and other restructuring activities to reorganise equity efficiently.

4. Maintaining regulatory compliance: Certain corporate actions, including buybacks and capital reductions, require shares to be formally cancelled to comply with applicable legal and regulatory requirements.

5. Managing dilution: Companies may cancel shares to offset dilution arising from stock options, convertible instruments, or historical share issuances.

These three terms describe related but distinct situations:

The process for cancelling shares in India depends on the reason for cancellation, the type of company involved, and whether the cancellation affects issued or authorised share capital. In most cases, the procedure includes the following steps:

1. Authorization: Ensure that the company’s Articles of Association permit share cancellation or reduction of share capital.

2. Board resolution: Conduct a board meeting to approve the proposed cancellation and authorise the necessary corporate actions, filings, and shareholder approvals where required.

3. Shareholder approval: Certain buybacks and capital reduction exercises require shareholder approval through a special resolution under the Companies Act, 2013.

4. Regulatory filings: File the prescribed forms, resolutions, and supporting documents with the Registrar of Companies (ROC) within the applicable timelines.

5. Application to NCLT (if applicable): For reduction of share capital involving cancellation of shares under Section 66 of the Companies Act, 2013, the company must apply to the National Company Law Tribunal (NCLT) with the required documents, including creditor lists and auditor certificates. The NCLT may issue notices and consider objections before granting approval.

6. Cancel & update records: Cancel the relevant share certificates or extinguish the shares through the depository system, and update the company’s register of members and other statutory records to reflect the revised share capital structure.

The tax treatment of share cancellation depends on the structure of the transaction and parties involved.

For shareholders, cancellation of shares may trigger tax liability if consideration is received in exchange for the cancelled shares. The applicable treatment differs based on how long the shares were held, whether the shareholder is a resident or non-resident, and whether the shares are listed or unlisted.

Following amendments introduced under the Finance Act (No. 2), 2024, certain buyback proceeds may be treated as dividend income and taxed in the hands of shareholders under the Income Tax Act, 1961. Companies may also be required to deduct tax at source (TDS) on such payments in accordance with applicable provisions.

In some cases, shareholders may also need to evaluate the capital loss implications arising from the extinguishment of shares, particularly in buyback transactions.

Where shares are cancelled without any payout, such as cancellation of unissued shares or internal restructuring exercises, the immediate tax impact may be limited.

Since the tax treatment varies based on the nature of the transaction and the status of the shareholder, companies and investors typically seek professional tax and legal advice before proceeding with share cancellation.

Share cancellation directly affects existing shareholders. Here is what changes and what to watch out for:

1. Impact on ownership percentage: When shares are cancelled, through a buyback or capital reduction, the total number of outstanding shares falls. Every remaining shareholder owns a larger slice of the company without buying a single additional share.

Example: A company has 1,00,000 shares. A shareholder holds 5,000 shares (5%). The company cancels 10,000 shares. That shareholder now holds 5,000 out of 90,000 shares, approximately 5.56% ownership, with no action on their part.

2. Impact on earnings per share (EPS): With fewer shares in circulation, the same net profit is distributed over a smaller base. This mechanically increases EPS and is one of the primary financial motivations behind buybacks and subsequent share cancellation.

3. Impact on share price: Markets generally read post-buyback cancellations as a positive signal, it usually means management believes the stock is undervalued and the company has surplus capital. The price impact depends on the reason for cancellation, though. Cancellations tied to capital losses or financial distress carry a very different signal than those from a healthy buyback.

4. Impact on ESOP holders: If cancelled shares were part of an ESOP pool, the company must revisit its ESOP plan. Unexercised options tied to cancelled shares typically lapse. Founders and HR teams should notify employees before the cancellation is executed, not after. Finding out after the fact is one of the most common causes of disputes in unlisted companies and startups.

The approval process and regulatory filings are the same regardless of how shares are held. What differs is the mechanics of how the shares are actually extinguished.

For physical shares, the shareholder must surrender the original share certificates to the company or its registrar and transfer agent (RTA). The certificates are verified against company records before the cancellation is processed.

Once verified, the certificates are marked or stamped as “cancelled” to prevent further use or transfer. The company then updates its register of members and statutory records to reflect the revised share capital.

For shares held in demat form through National Securities Depository Limited (NSDL) or Central Depository Services Limited (CDSL), the process is completed electronically through the depository system.

After the required approvals and filings are completed, the company instructs its registrar and transfer agent (RTA) and depository participant to extinguish the relevant shares from the shareholder’s demat account. The depository records the cancellation electronically and updates the company’s outstanding share capital accordingly.

Since dematerialised transactions are digitally recorded and timestamped, they generally provide a clearer audit trail for regulatory filings, due diligence, and compliance reviews.

Share cancellation is not just about removing shares, it is about making sure the capital structure reflects where the company is going, not where it has been. Every stage of a company's growth brings changes, new investors, new ownership arrangements, new financial targets.

A capital structure that has not been cleaned up along the way can quietly work against those goals. It can complicate the story you tell investors, slow down due diligence, and create gaps between what the register says and what the business actually looks like today. The companies that get this right are not doing anything extraordinary, they are simply keeping their capital structure honest as the business evolves.

Share cancellation changes your ownership structure, and your cap table needs to reflect that accurately the moment it happens. Any missed update can create discrepancies later.

Qapita's cap table management platform gives founders and finance teams a single source of truth for all equity events, including buybacks, capital reductions, and ESOP pool adjustments. Over 2,400 companies across 60+ countries trust Qapita to keep their equity records accurate, audit-ready, and up to date.

Book a Demo to see how Qapita can help you manage your cap table after a share cancellation.

A private company cancels shares by first checking that the articles of association permit it, passing the required board or shareholder resolution depending on the type of cancellation, filing the necessary forms with the ROC, and updating the Register of Members. For unissued shares, an ordinary resolution is enough. For capital reduction, NCLT approval is required. For post-buyback cancellation, shares must be extinguished within seven days of the buyback closing.

The shares stop existing. The shareholder loses all rights attached to those shares, voting rights, dividend entitlement, and ownership claim. The company's total share count reduces, and the Register of Members is updated to reflect the change. If the shareholder received consideration for the cancelled shares, a tax event may be triggered.

Cancellation of shares means permanently removing shares from a company's capital structure. Once cancelled, those shares cannot be traded, transferred, or reissued. It is different from a share transfer, where shares move from one person to another. Cancellation ends the existence of the share entirely.