Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Equity compensation or stock compensation, is a non-cash payment representing partial ownership of the business and its profits. It offers a useful way to encourage employees to contribute to the long-term success of a company. In fact, a report from Morgan Stanley suggests that over 84% of employees believe a benefits plan inclusive of stock ownership and equity compensation can be effective motivators.

Startups often include equity compensation in their remuneration packages to incentivize and motivate their employees. Two common forms of equity award you can offer as a startup founder to eligible team members are Restricted Stock Units (RSUs) and Employee Stock Ownership Plans (ESOPs). While they may seem similar, RSUs and ESOPs have distinct features that can significantly impact an employee's financial situation and the company's capital structure.

This blog covers important aspects of RSUs, how they work, their advantages and disadvantages, accounting treatment and how they differ from ESOPs.

A restricted stock unit (RSU) is a form of stock-based compensation that companies often use to reward their employees. It represents a promise to grant shares of company stock in the future once certain conditions are met. These conditions typically include achieving specific performance goals or staying with the company for a certain duration.

RSUs are granted through a vesting plan, which outlines when the employee will receive the shares. The vesting schedule can be created as per duration, performance goals, or a combination of both. Until the vesting conditions are fulfilled, RSUs do not have any tangible value.

Once vested, the shares are assigned a fair market value (FMV), and they become taxable income for the employee. A portion of the shares is usually withheld to cover the payroll tax. The employee receives the remaining shares, which they can then hold or sell.

Here is the process detailing how RSUs work as a form of employee compensation:

1. Grant date: The process begins on the RSU grant date. However, at this stage, the RSUs are just a promise of shares, not actual shares. The employee does not own these units yet and, therefore, has no voting or dividend rights.

2. Vesting schedule: The vesting schedule outlines the conditions that the employee must meet to earn the right to the shares. These conditions often involve a period of service with the company. For example, your startup might require an employee to stay with the company for four years to fully vest the RSUs.

3. Vesting: Vesting refers to the process by which the employee earns the right to the shares. As the employee fulfils the specified conditions, the restrictions on the RSUs lapse gradually over the vesting period. For instance, 25% of the RSUs would vest each year under a four-year schedule with annual vesting.

4. Conversion to shares: Once the RSUs vest, they are converted into actual shares of the company. The employee now becomes a shareholder with voting rights and eligibility for dividends.

Let's illustrate this process with an example. Suppose your startup grants an employee 1,000 RSUs on January 1, 2024, with a four-year graded vesting schedule. Each year, 25% of the RSUs (250 RSUs) will vest. So, on January 1, 2025, the employee will earn 250 shares of the company. This process will repeat each year until all the RSUs have vested on January 1, 2028.

To fully understand the implications of RSUs, it is essential to learn more about their associated terms and conditions. Along with the vesting schedule, these elements shape the unique properties of RSUs and distinguish them from other compensations:

1. Performance conditions: You can attach performance conditions to RSUs, meaning that vesting could be contingent on meeting certain performance goals in addition to or instead of a time-based vesting schedule.

2. Clawback provisions: RSUs may come with clawback provisions, which allow you to reclaim vested or unvested shares under certain circumstances, such as misconduct or a restatement of financial results.

3. Dividend equivalents: Your company might provide dividend equivalents on RSUs, allowing employees to receive payments equal to the amount that would have been paid on the shares once they vest.

4. Voting rights: RSU holders do not have voting rights like actual shareholders until the units vest and convert into actual shares.

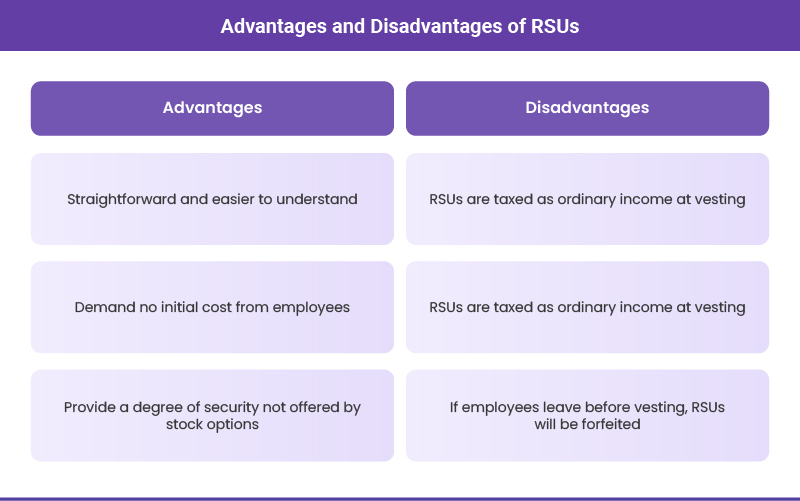

Restricted stock units come with a host of benefits that make them an attractive form of equity compensation for both companies and employees. Here are some of the key advantages on offer:

1. Simplicity: RSUs, representing a future promise of shares from the company to the employee, are straightforward. This is in contrast to stock options, which require an understanding of concepts like exercise price and time value.

2. No upfront cost: Unlike stock options which often necessitate an upfront purchase at an exercise price, RSUs demand no initial cost from employees. They simply receive the shares upon vesting.

3. Reduced risk: RSUs provide a degree of security not offered by stock options. They ensure ownership in the company, even if the stock price falls. Conversely, stock options risk becoming worthless if the stock price drops below the exercise price.

4. Performance alignment: RSUs create a direct connection between employee compensation and company performance. As the company's stock price rises, so does the value of the RSUs, encouraging employees to contribute to the company's success.

1. Delayed ownership: RSUs promise future shares, meaning employees don't own the shares or have voting rights or dividends until vesting. This can be a downside for employees who value these ownership perks.

2. Tax at vesting: RSUs are taxed as ordinary income at vesting, based on the shares' current market value. This could lead to a substantial tax liability, especially if the stock price has significantly risen since the grant date.

3. Tied to stock performance: The value of RSUs is directly associated with the company's stock performance. If the stock price falls, so does the value of the RSUs, potentially affecting the overall compensation received by employees.

4. Forfeiture risk: Employees risk forfeiting all unvested RSUs if they leave the company before vesting. This forfeiture risk, resulting in a loss of potential compensation and future appreciation, can be a significant disadvantage for employees considering a job change.

One question that often arises when discussing Restricted Stock Units (RSUs) is whether they carry voting rights. The answer to this question is typically no. When your startup grants RSUs to an employee, you are essentially promising future shares.

However, until these units vest and convert into actual shares, the employee does not technically own them. As a result, they do not have the voting rights that come with share ownership.

This lack of voting rights can have implications for employees who wish to have a say in company decisions. Voting rights allow shareholders to influence corporate policy and management issues through the voting process. Without these rights, RSU holders may feel they lack a voice in the company's direction until their units vest.

RSUs are typically recognized as compensation expenses over the requisite service period, which usually aligns with the vesting schedule. The fair value of the RSUs is determined at the grant date and is recognized proportionately over the vesting period.

For example, if you grant 2,000 RSUs with a four-year vesting schedule to an employee and the fair value of the stock at the grant date is $2.00 per share, you would recognize a compensation expense of $1,000 each year. The accounting entries for this would be:

On the grant date: No journal entry is required on the grant date because the RSUs represent a promise to issue shares in the future, not an immediate transaction.

On the vesting dates: The vesting period is four years, and the fair value of the RSUs at the grant date is $2.00 per share. Therefore, each year, 500 RSUs (2,000 RSUs / 4 years) will vest, and you would recognize a compensation expense of $1,000 (500 RSUs * $2.00 per share). The journal entry for each of the four years would be the same:

Debit: Compensation Expense $1,000

Credit: Additional Paid-In Capital (APIC) - RSUs $1,000

Accurate accounting for RSUs is crucial for compliance with financial reporting standards and for providing transparent information to shareholders and potential investors. It is also important for calculating key financial metrics, such as Earnings Per Share (EPS).

Here is a breakdown of how taxation works for RSUs, along with some examples and potential tax planning strategies:

1. Taxation at vesting: When the RSUs vest and convert into actual shares, the employee will need to report income equal to the value of the stock received. For example, if an employee's 1,000 RSUs vest when the FMV is $10 per share, they would report $10,000 (1,000 RSUs * $10) as ordinary income on the day of vesting.

2. Capital gains tax: Any subsequent profit from selling the shares is taxed as capital gains. If the employee sells the stock at a higher price than its FMV at the time of vesting, they will have a capital gain. For instance, if the employee sells the shares when the stock price is $15, their capital gain would be $5,000 (($15 - $10) * 1,000).

3. Short-term vs. Long-term capital gains: The duration for which the employee holds the shares after vesting determines the type of capital gains tax. If the stock is sold within one year of vesting, the gain is short-term and is taxed at the employee's ordinary income tax rate. If the stock is held for more than a year, the gain is long-term, and the employee will pay tax at the more favorable long-term capital gains rate.

Employees can leverage different tax planning strategies to minimize their tax liability. One popular option is to hold onto the shares after they vest to qualify for long-term capital gains treatment. However, this strategy comes with the risk that the stock prices could fall, reducing the potential value of the shares.

The experience of holding RSUs differs depending on whether a company is privately held or publicly traded.

Employees of public companies can typically sell their vested RSU shares immediately on the open market, subject to their company's trading policy. Some companies enforce blackout periods, windows of time during which employees cannot trade shares, usually around earnings announcements.

RSU holders at private companies face a more complex situation. Even after RSUs vest, employees cannot sell their shares freely because there is no public market for them. The ability to convert vested RSUs into cash is tied to a liquidity event such as an IPO, acquisition, or a company-led secondary transaction.

Here is a comparison between RSUs and stock options as two popular employee compensation methods:

Selecting the right form of equity compensation can be a complex decision as the answer can be different when considered from different perspectives:

1. Company perspective: Your company's choice between RSUs and stock options can depend on the stage of growth, financial situation, and the preferences of its employees. For instance, as a startup, you might lean towards stock options as they don't require a cash outlay until the options are exercised. Conversely, after becoming an established company, you might favor RSUs for their simplicity and lower risk for employees.

2. Employee perspective: From an employee's viewpoint, the choice between RSUs and stock options depends on their risk tolerance and financial goals. RSUs offer the security of knowing they will receive something of value, while stock options present a potentially higher upside if the company's stock price increases significantly.

Here is a comparison between RSUs and stock options as two popular employee compensation methods:

In recent years, companies have increasingly favored RSUs over stock options. Several factors drive this shift:

1. Less dilution: Since RSUs don't have an exercise price, the entire FMV of the share is passed on to the employee as a benefit. So, the company can meet a target dollar value of employee compensation with a lesser number of RSUs as compared to stock options.

2. No exercise cost: With stock options, employees must purchase the option at the exercise price to realize any gain. This can be a significant out-of-pocket expense. In contrast, RSUs do not require any investment on the part of the employee. They are granted for free and converted into shares at no cost to the employee.

3. Alignment with exit strategy: RSUs can be better aligned with a company's exit strategy, such as an IPO. This is because RSUs are typically granted after a private company goes public. They can be a more attractive form of equity compensation for employees in a company that is planning to go public or has recently done so.

Several companies have made the switch from stock options to RSUs. Here are two prominent examples:

1. Microsoft: In the past, Microsoft offered stock options to its employees. However, they switched to RSUs as they found them to be simpler and less risky. RSUs are easier for employees to understand as they represent a promise of future shares and do not require any upfront payment. This shift has made equity compensation more accessible and attractive to Microsoft's employees.

2. Nike: Similar to Microsoft, Nike also transitioned from stock options to RSUs. The company offers its employees a choice between stock options, RSUs, or a mix of both. However, RSUs have become a popular choice due to their simplicity and reduced risk. This change has helped Nike to attract and retain talent effectively.

RSUs are often perceived purely as a financial reward, but they represent something more fundamental, a structural alignment between the people building a company and the outcomes they are working toward. When designed thoughtfully, an RSU program does not just compensate employees for their time; it gives them a genuine stake in the decisions they make every day.

For founders, this means structuring RSU grants with fair vesting schedules, clear communication around liquidity, and transparency around tax implications. For employees, it means understanding that the value of an RSU is not fixed at the grant date, it is shaped by every contribution made between the grant and the day the shares are sold. That alignment, when communicated well, is worth more than the grant itself.

At Qapita, we understand the importance of equity compensation tools like Restricted Stock Units (RSUs) for both employers and employees. We know that as a startup founder, offering RSUs can be a strategic move to attract, retain, and motivate top talent. For your employees, RSUs represent a potential for significant financial gain and a direct link to your company's success.

Qapita is a leading equity management platform helping startups manage all equity matters from inception to IPO. Our platform is trusted by over 2,400 companies and 300,000 employee-owners. As a top-ranked Equity Management Software on G2, we offer all the tools and expertise you need to structure your company's equity compensation plan.

Contact us now to learn more about our services.

A vesting schedule is a timeline set by your company that determines when you receive your RSUs as actual shares. For example, if you are granted 1,000 RSUs with a four-year vesting schedule, you earn 250 shares each year over four years. Until the schedule is complete, you do not own the shares outright.

An RSU (Restricted Stock Unit) is a promise of shares delivered to you after vesting conditions are met. You do not own the shares or have any shareholder rights until they vest. An RSA (Restricted Stock Award) grants you actual shares immediately at the time of the award, meaning you own the shares from day one but they come with restrictions on selling until vesting conditions are met. The key difference is ownership timing, RSAs give immediate ownership, RSUs do not.

Any unvested RSUs are forfeited immediately when you leave the company, regardless of whether you resign, are laid off, or are terminated. You lose the right to any shares that had not yet vested at the time of your departure. However, any RSUs that have already vested and converted into shares belong to you and are not affected by your departure.

No, RSUs do not trigger the Alternative Minimum Tax (AMT). RSU income is treated as ordinary wage income at vesting and is subject to regular income tax. This is one area where RSUs differ from Incentive Stock Options (ISOs), where the spread at exercise can trigger an AMT liability.

Yes, RSUs are a component of your total compensation package and can be negotiated. You can negotiate the number of RSUs in your offer, particularly if the base salary is lower than expected. If you are leaving unvested RSUs at your current employer, you can also use this as leverage to request a higher RSU grant or a signing bonus from your new employer to compensate for what you are leaving behind.

Once RSUs vest you have two choices, sell the shares immediately or hold them. Selling immediately gives you cash and removes the risk of the stock price falling. Holding the shares for more than one year after vesting qualifies any gains for long-term capital gains tax rates, which are more favorable than ordinary income tax rates. The right decision depends on your financial goals, tax situation, and how much of your wealth is already tied to your employer's stock. Consulting a financial advisor before making this decision is recommended for large RSU grants.