Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

%20-%20T%201.jpg)

With the rise in the startup industry, almost every startup recognises the importance of setting up an employee benefit structure in place so that they can adequately incentivise their people for the growth the company has achieved. Widely used share-based remuneration systems in companies are stock options and SARs. While both employers and employees acknowledge that employees should be adequately rewarded, there is a huge information gap at the hands of both parties, and they are not aware of which of these to use.

In this blog, we will cover what SARs are, how they work, how they compare to stock options and more.

Stock appreciation rights (SARs) are a type of equity-related compensation that allows employees to benefit when their company’s share price increases, without having to buy the shares themselves. Unlike stock options, SARs usually do not require payment of an exercise price. Instead, employees receive the value of the increase in the company’s stock price over a certain period, which may be paid out in cash or shares. Because of this structure, SARs can be an attractive incentive for employees while also helping companies limit the dilution of existing shares.

Companies often issue SARs to employees alongside their regular pay or in lieu of stock options. Sometimes, SARs come with stock options, too. When this happens, employees can use SAR proceeds to help pay for their stock options.

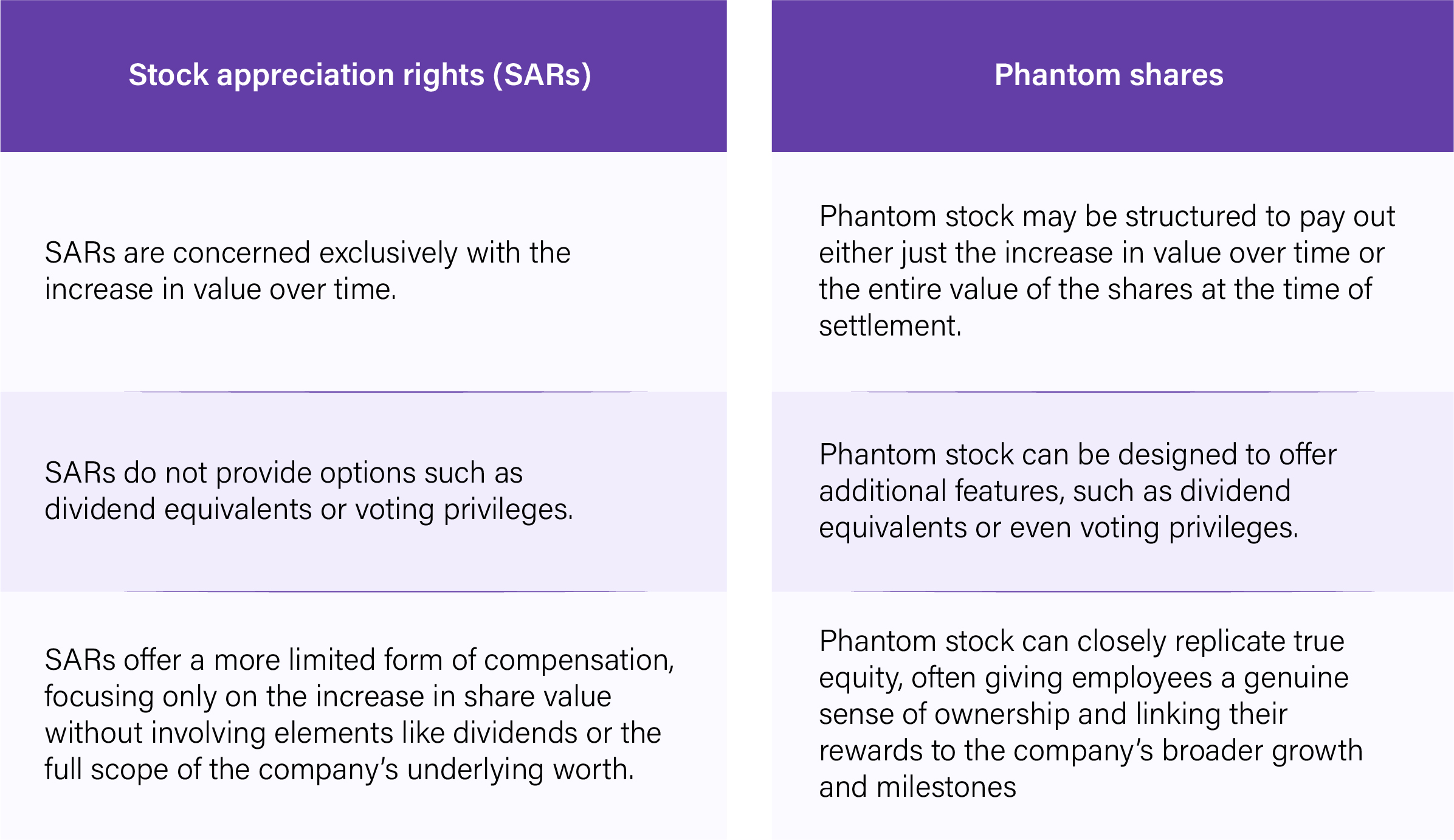

Phantom stock and stock appreciation rights (SARs) are often seen as similar, especially by those exploring equity compensation for the first time. Both are designed to reward and motivate employees without granting actual ownership in the company. However, despite these similarities, there are key differences in how they operate and are structured, making it important for companies to understand which option best fits their needs.

While they may seem alike at first glance, a closer comparison highlights the distinct features of Phantom Stock and SARs.

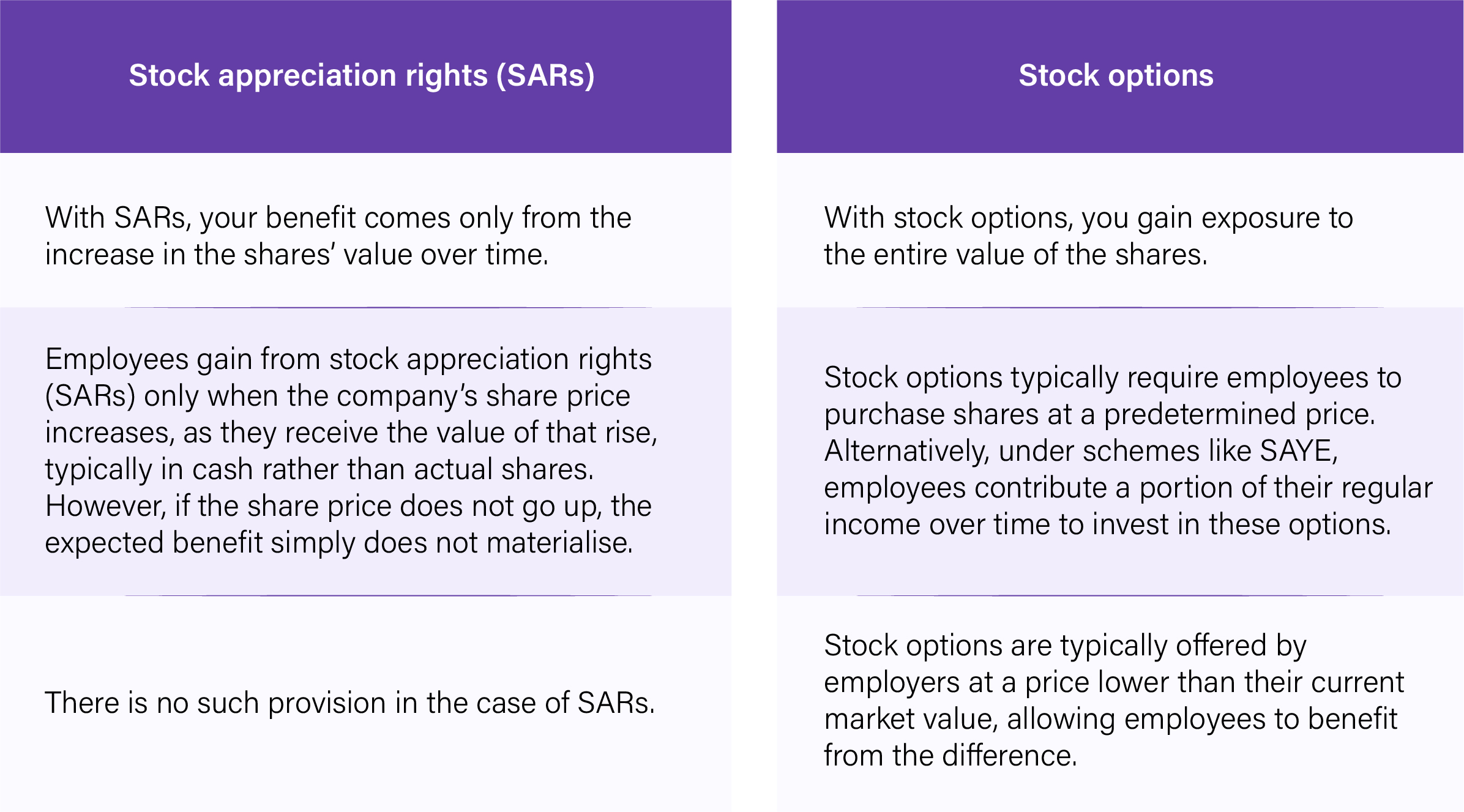

While both SARs and stock options are designed to incentivize and reward employees, they function in different ways and provide distinct advantages.

Here are the key differences between them.

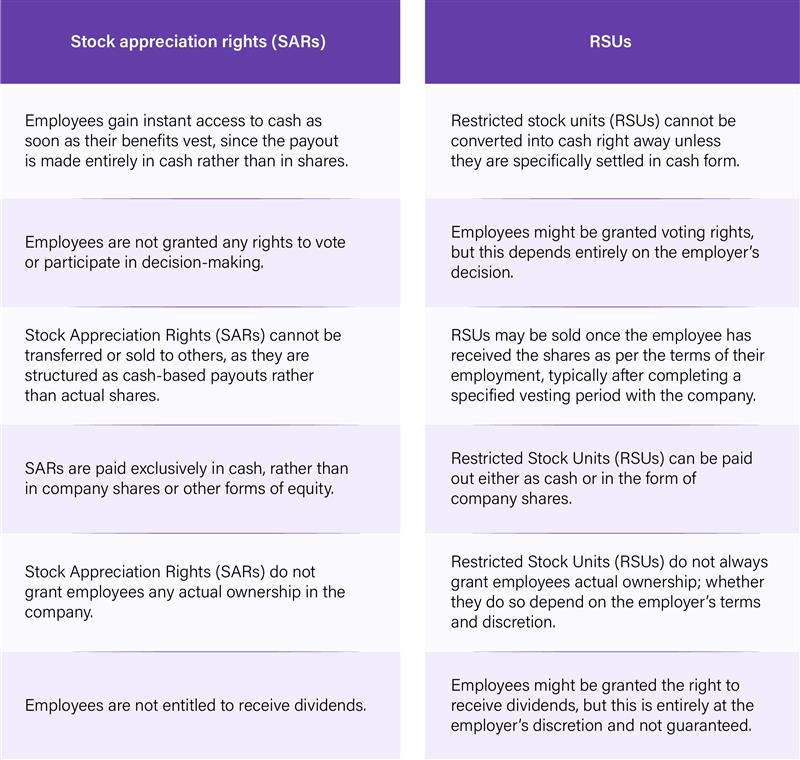

Here are the differences between SARs and RSUs.

In most companies, stock appreciation rights (SARs) are administered by the compensation committee (CC), a committee formed by the company’s board of directors. Here is the step-by-step process for implementing SARs.

To begin the SARs process, board approval is required. The company’s board of directors must first approve the plan, which includes determining eligible employees, typically based on factors such as role, performance, and tenure.

For unlisted (private) companies, the process is generally simpler and less regulated. These companies have greater flexibility in designing their SAR schemes, they can grant SARs not only to employees but also to third-party participants such as consultants and may offer them at different prices to different individuals. Unlike listed companies, unlisted firms are not required to set up a mandatory vesting period or establish a Compensation Committee; the board of directors can administer the scheme directly.

Stock appreciation rights are generally classified into two types.

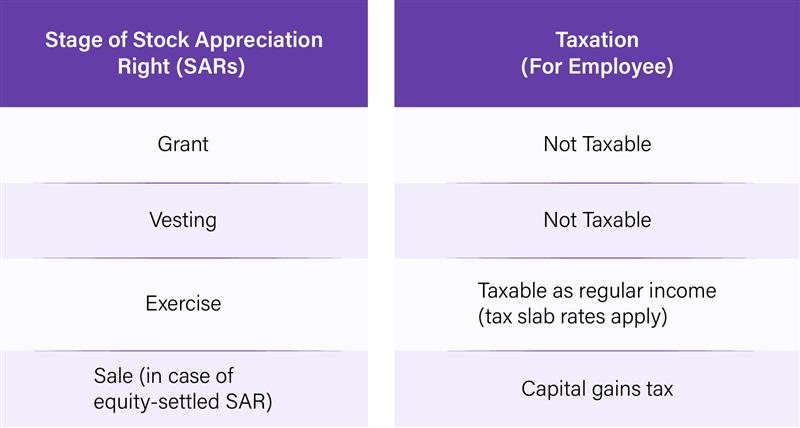

Getting a stock appreciation right (SAR) does not create a tax bill. Just like regular stock options, you don't have to report anything to the IRS when you first get the SAR.

When SARs are exercised, the difference between the market price at the time of exercise and the market price at the grant date is multiplied by the number of SARs exercised, and this amount is treated as ordinary compensation income. This amount is subject to income and payroll taxes.

In many cases, the plan’s terms require automatic withholding of taxes from the cash proceeds upon exercise of SARs. The employer calculates the required federal income and payroll taxes based on the compensation value realized from the SARs and directly withholds this amount before distributing the net proceeds to the employee.

XYZ Corporation granted stock appreciation rights (SARs) on January 1, 2012, when its share price was $15. The vesting date, when the employee becomes eligible to exercise these rights, is January 1, 2022.

Emma received SARs tied to 120 XYZ shares. On the vesting date, XYZ’s share price is $75. The value of Emma’s SARs is $7,200 [($75 – $15) × 120].

At this point, Emma has two choices: she can either receive the $7,200 as a cash payout or opt to settle the SARs in shares of XYZ stock, which would be equivalent to 96 shares ($7,200 ÷ $75).

Here are the advantages of stock appreciation rights.

Here are the disadvantages of stock appreciation rights.

With Qapita’s powerful equity management platform, you can design and issue digital SARs, manage grants seamlessly, and keep every stakeholder aligned through a single, transparent system. From grant creation to employee transactions, Qapita streamlines the entire SAR lifecycle, making employee rewards easier to manage and more transparent than ever. Book a demo today!

Stock options give employees the right to buy shares at a fixed price, so they benefit from both the appreciation and the full value of the shares. SARs only deliver the increase in share value, typically as a cash payment, with no requirement to buy shares. SARs are simpler and carry no upfront cost to the employee

While expiry periods vary by plan, SARs commonly expire 7–10 years from the grant date. If you do not use them before they expire, they become worthless. Leaving your job, retiring, or passing away can also change the timing of your benefits.

If you leave your employer, stock appreciation rights usually expire sooner. If you retire, you can keep any vested rights, but you may have less time to use them. Check your employer’s rules for exact details.