Equity management

Equity management

ESOP Management

ESOP Management- Fund management

Liquidity Solutions

Liquidity Solutions - Fund managementESOP Consulting

- Fund managementFund Management

These days, startups are increasingly making use of ESOPs to lure talented individuals to their venture. ESOPs imbibes a sense of ownership in the employees and enhance their retention. However, ESOPs are liable to taxation. As a company founder, you want your employees to understand the legalities and taxes associated with ESOPs and perform their duties accordingly.

This blog gives a clear understanding of ESOP taxation guidelines in India.

Before going into the taxation, we recommend that you understand the basic terms related to ESOPs.

The primary law governing ESOP taxation in India is the Income Tax Act, 1961. The provisions of the Act vary for both Salary Income and Capital Gains arising from ESOPs.

In India, ESOPs taxation happens at two points from employees perspective:

The perquisite value earned upon exercising of ESOPs is treated as the salary income. The regular taxation rates are applied based on the income level and deducted by the employer as TDS.

Income from perquisite = Market value of shares on the exercise date - Total exercise amount

If the company is not listed on the share market, the market value is determined by FMV (fair market value) based on the valuation certificate given by a merchant banker. Note that the valuation certificate should not be older than 180 days from the date of exercise.

If the company is listed, the share value is calculated as the average of opening and closing on the exercise date on a recognized stock exchange that records the highest volume.

Capital gain = Sales value of shares - Market value of shares at the time of exercising

Capital Gains Tax on ESOPs/ESPP vary based on factors like:

The short-term or long-term nature of the gains varies for listed and unlisted shares.

For listed companies: If the employee holds the shares for less than 12 months, it is considered short-term capital gains(STCG). Short-term capital gains tax is taxed at a flat rate of 20%.

But, if the shares are held for more than 12 months, the gains arising from the sale of the shares are considered long-term capital gains (LTCG). Long-term capital gains are taxed at the rate of 12.5% if they reach of Rs. 1,25,000 in a fiscal year.

For unlisted shares: If the employees of a company hold the shares for less than 24 months before selling them, it becomes a short-term capital gain. Short-term capital gains are treated as any other income and taxed at the applicable income tax slab rate.

However, if shares are held for more than 24 months before their sale, the gains are taxed as long-term capital gains. Sec 112 A of the IT Act says that long-term capital gains arising from the sale of unlisted shares are taxed at a rate of 20% with indexation.

Or, you can choose to pay a tax at a flat rate of 10% without any indexation benefits.

Note: Non-payment of advanced Capital Gains Tax can attract penal interest under sec 234 C & 234B.

Employees must file Income Tax Returns Form 1 (ITR Form 1) to report the perquisite. The employee needs to file Income Tax Returns Form 2 (ITR Form 2) to report the capital gain tax.

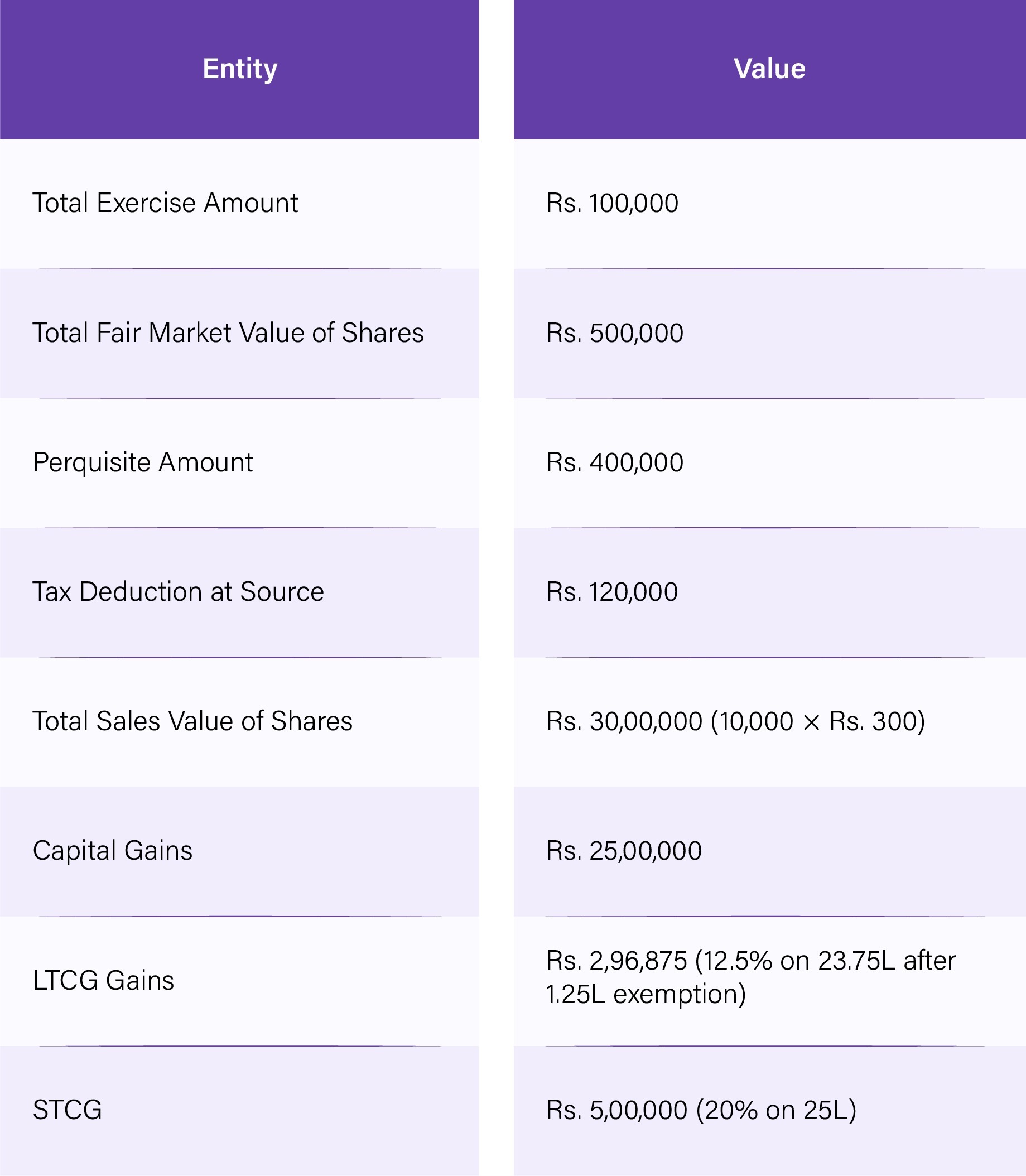

Let's see through an example of how ESOPs are taxed.

Imagine you allot 10,000 ESOPs to an employee at a particular date (grant date). And let's say you are a listed company.

The grant price/exercise price = Rs. 10/ share

Total amount to be paid by the employee to get all the shares = 10 * 10,000 = Rs. 100,000

After two years, the employee chooses to exercise all the options. Suppose, at that time, the FMV of a share is Rs. 50.

Now, let's calculate the taxes at the time of exercising the option.

Here, the perquisite = No. of shares (FMV - Exercise price) = 10,000* (50-10) = Rs. 400,000

Suppose the employee falls under the 30% tax slab,

The TDS deducted by employer = 400,000*(30%) = Rs. 120,000

After a while, if the employee chooses to sell the shares, they have to pay the capital gains tax.

Here, capital gains = No. of shares (sale price of the share - FMV)

Imagine the sale price is Rs. 300.

Capital Gains = 10,000(300 - 50) = Rs. 25,00,000

If the holding period is less than or equal to 12 months, an STCG (Short-Term Capital Gains) tax of 20% is applicable = (Capital Gains * 20%) = Rs. 5,00,000

If the holding period is more than 12 months, LTCG (Long-Term Capital Gains) tax of 12.5% is applicable on 23.75 lakhs = (Capital Gains in access of 1.25 lakh * 12.5%) = Rs. 2,96,875

Let's summarise the above discussion in a tabular format.

Note: Budget 2020-2021 changed the taxation regime for budding startups (provided exemption under sec 80 - IAC). These guidelines were put forth by the DPIIT (The Department of Promotion of Industry and Internal Trade).

Here, employees of the budding startups are exempted from paying taxes for a particular period under certain circumstances:

The tax deduction due to the above reasons will be taken care of by the company within 14 days of fulfilling the conditions.

The advantage of the budgetary changes is that:

While calculating ESOP taxes, there are other considerations, like the residential status, loss incurring ESOPs, disclosures, and more.

Residential Status: If you reside in India or outside India, your ESOP transactions are liable to taxation. As an employer, be aware if there is a double taxation avoidance agreement (DTAA) signed between two countries, your employees can avoid being taxed twice: one in India and one abroad.

Disclosures for Foreign Assets: When employees receive shares from a parent, foreign company, the shares are treated as foreign assets. Employees need to show these assets by filing ITR-2 or ITR-3. Also, the disclosures need to be made in the IT Act's schedule FA (Foreign Assets).

Taxation of Loss Incurring ESOPs: If the sale of an ESOP results in a loss, an employee can carry it forward for the next eight financial years. The loss can subsequently be adjusted with the gains as and when it takes place.

Thank you for reading.