Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

409A valuation acts as the benchmark for establishing the Fair Market Value (FMV) of a startup's common stock when offering ESOPs (Employee Stock Ownership Plans). This valuation methodology is named after the US Internal Revenue Code (IRC) Section 409A.

It directly impacts the equity allocation and tax obligations for employees of private enterprises. When employees receive stock options, the taxes owed to the IRS (Internal Revenue Service) are calculated based on the 409A valuation.

To ensure accuracy, 409A valuations are conducted annually or after significant events, such as new funding rounds or major acquisitions. This blog covers the importance of 409A valuation for employees, its impact on different stock options, and accompanying tax liabilities. Read on!

For an employee, stock options represent a right, but not an obligation, to purchase a company's stock at the strike price (predetermined price of a share) on a future date.

When you are granted stock options as an employee, you are essentially being given an opportunity to be a part of the company's success. It is an important incentive that aligns your interests with the company's growth and prosperity.

However, these stock options do not become available all at once. They are subject to a vesting period, which is a predetermined timeframe during which the options gradually become exercisable. This period can span several years, encouraging employees to be a part of the enterprise for the long term.

As discussed above, a 409A valuation is important to determine the fair market value of the company's common stock. The IRS requires this valuation to prevent enterprises from undervaluing their options, which is otherwise seen as concealing their income. If the valuation of the company is too low, the authorities might consider it as an under-reporting of the profits, and as a result, the company and the employees could face severe IRS penalties.

The company's valuation can be conducted using any of the following 409A methodologies:

This method analyzes recent funding rounds of similar companies in the same stage and industry. Appraisers consider the price per share that potential investors are willing to pay for those companies to estimate the FMV.

This method forecasts the future cash flows of the enterprise and then discounts them to their present value. The valuation provider considers factors like growth potential and risk to arrive at the FMV.

This method is often used for early-stage companies that don't have a significant revenue stream yet. Here, appraisers determine the value of a private company based on the FMV of tangible assets (like equipment) and intangible assets (like intellectual property).

When conducted by a qualified third-party appraiser using any of the above IRS-approved methods, the valuation gains safe harbor status. The safe harbor requires the IRS to prove the FMV determined as 'grossly unreasonable' before initiating any audit. This status protects employees from any potential tax issues arising due to the grant of stock options.

The 409A valuation is of significant importance for employees in deciding the strike price of stock options and the tax payable. Here is an analysis of these two reasons.

The 409A valuation sets the minimum strike price for ESOPs. This means that the enterprise cannot offer the stock to employees at a price lower than the current value. The strike price defines the price at which employees can buy the company's stock in the future. It is set at the time the options are granted and is usually equal to the FMV of the company's stock as determined by the 409A valuation. Let's consider an example to understand the concept of strike price.

Being a star employee, XYZ Enterprises offers you 3,000 stock options with a strike price of $4 per share based on a 409A valuation. After four years (vesting period), the company stock price climbs to $30 per share. Now, you can exercise your options and buy those 3,000 shares for $4 each (the strike price), even though they are now worth $30 each. This allows you to potentially make a significant profit by selling the shares at the current market value.

A higher 409A valuation can potentially benefit employees by lowering their tax liabilities at the time of exercising the stock options. When employees exercise the ESOPs (i.e., buy the stock at the strike price), they must pay the tax on the difference between the stock's FMV and the strike price at that time. Let's continue with the example of XYZ Enterprises.

When you exercise the 3000 stock options at the strike price of $4 (compared to $30 market price), you make a profit of $78,000. The tax amount you must pay to the IRS depends on the holding period of the options and your taxation bracket.

Companies usually offer two main types of stock options to employees, i.e., statutory and non-statutory stock options. Here is a brief analysis of both these variants:

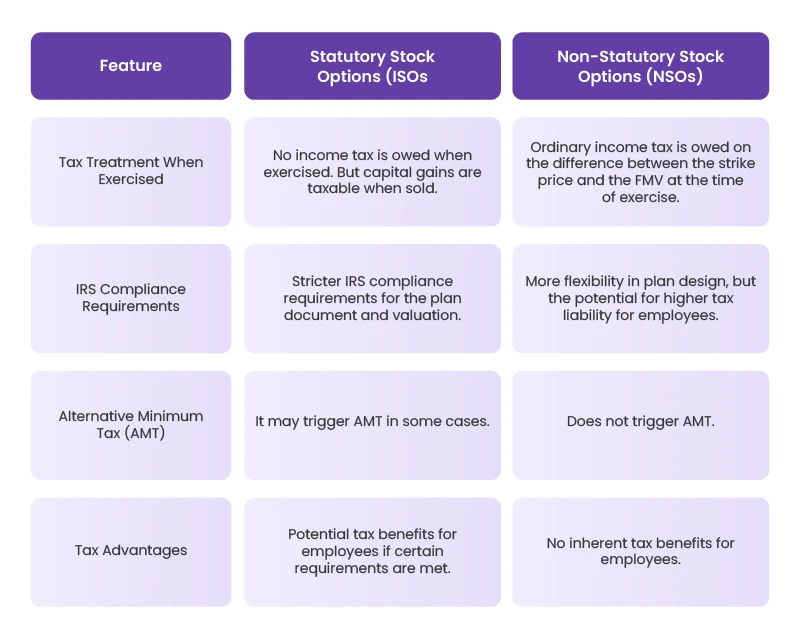

These options, also known as Incentive Stock Options (ISOs), are typically offered to top management and key employees as part of a compensation package designed to retain them. When employees hold ISOs, they can purchase a given number of common shares at a pre-defined price on a future date, regardless of the market price.

When statutory stock options are issued, their strike or exercise price must not fall below the market price of the stock at the time of issue. Taxation rules for these options can be complex. While exercising statutory stock options does not immediately create taxable income for the employee, capital gains tax is applicable upon the eventual sale of the shares based on the profit made.

They are also known as Non-Qualified Stock Options (NQSOs or NSOs) and can be offered to employees as well as independent contractors. NSOs are more flexible for companies to set up, but they come with different tax implications for employees. When employees exercise NSOs, they must pay ordinary income tax on the gap between the FMV and the exercise price of the stock on the date they exercise these options. This may result in a larger tax liability compared to the taxes on ISOs.

A critical factor to remember with ISOs is their impact on the Alternative Minimum Tax (AMT). The AMT is an independent tax framework designed to guarantee that specific taxpayers contribute a minimum amount of Federal Income Tax. It factors in the bargain element (difference between the strike price and FMV) of ISOs.

One advantage of the bargain element is that it is exempt from regular Federal Income Tax. However, it is added to your AMT income when you exercise ISOs and retain them beyond the end of the calendar year.

Let's illustrate this with an example. Suppose you have 15,000 ISOs with a strike price of $20. When you exercise the ISOs, the stock price is $80. The variation between the strike price and the stock price is $60. Multiply this by the number of ISOs exercised (15,000), and you get the bargain element ($900,000). Assuming a flat 28% AMT tax rate on the $900,000 bargain element, the total AMT due would be $252,000.

Non-compliance with 409A valuation can lead to significant tax penalties for employees. If the IRS determines that a company's 409A valuation was not conducted properly or that the strike price of employees' stock options was set below the fair market value, it can trigger severe tax consequences.

Under the Non-qualified Deferred Compensation (NQDC) plan, employees might have to pay income tax on all amounts that are vested but deferred as of the final day of the vesting year. This means that employees could be taxed on income they have not yet received.

A 20% penalty tax is also levied on all deferred vested amounts. This penalty is over and above the regular income tax and increases the tax liability of employees.

For example, if an employee has $100,000 in deferred vested amounts, they will owe income tax on this amount plus an additional $20,000 in penalty taxes. This does not include any interest or additional penalties that may be assessed.

An accurate valuation ensures fairness in the stock option process and protects employees from unexpected tax liabilities. By ensuring an IRS-compliant 409A valuation, companies can ensure transparency in the process and avoid putting employees at risk of potential tax penalties.

Section 409A of the US IRC has a global reach, applying to worldwide income earned by US citizens working abroad (expatriates), resident aliens, and US source income earned by foreign employees working temporarily in the United States (non-resident aliens).

Section 409A interacts with foreign employees in the following ways:

Resident aliens working for a US company are treated the same way as US citizens regarding stock options and 409A valuation. They will benefit from the tax advantages associated with Incentive Stock Options (ISOs) if the plan meets IRS requirements and the valuation is compliant.

While a 409A valuation itself might not be mandatory for non-resident alien employees receiving stock options, it becomes important if the options are considered US-source income. This can happen if the employee performs a substantial portion of their work in the US or the stock options relate to a US subsidiary. In such cases, a proper 409A valuation helps determine the taxable income for the employee and ensures compliance with US tax regulations.

If non-compliance with Section 409A is identified, it can result in significant tax penalties. For example, under the NQDC plan, employees might have to pay income tax along with a 20% penalty on all amounts that are vested but deferred by the end of the vesting year.

When it comes to selecting a 409A valuation firm, look for an entity with a proven track record in handling 409A valuations for startups, as experience translates to a deeper understanding of the specific challenges faced by early-stage companies. Also, the firm must utilize reputable valuation methodologies accepted by the IRS with a transparent approach. Choose a firm that offers clear communication and is readily available to answer your questions throughout the process.

Don't underestimate the power of a well-designed stock option plan with a compliant 409A valuation. Partnering with Qapita ensures a smooth and transparent process, allowing you to attract and retain top talent with a compelling equity incentive.

At Qapita, we take pride in helping global companies manage their CapTables, ESOPs, valuations, and liquidity solutions.

Connect with our experts today to know how we can help you with equity management!