Dec 15, 2021

The Top 30 Venture Capitalist Firms for Early-Stage Startups in India

In this post, we have discussed some of the prominent VCs who invest in early and growth-stage startups in India.

Startups raise venture capital to drive growth, but equity dilution can hurt founders and early employees. That’s where venture debt financing comes in—a non-dilutive capital source designed specifically for VC-backed companies looking to extend their runway, reach milestones, and defer larger equity raises.

But what is venture debt, and why do startups use it? This guide explores the mechanics, benefits, and considerations of venture debt, helping founders make informed decisions about their capital stack.

Venture debt is another form of debt financing designed for early-stage startups, high-growth companies that are already backed by venture capital. Unlike traditional loans, venture debt is tailored for startups that may lack positive cash flow or significant assets but have strong growth potential and venture backing.

It serves as an additional source of capital, typically used alongside equity financing to fund operations, purchase equipment, or support expansion without immediate equity dilution.

Specialized lenders typically issue venture debt to startups that have recently raised equity funding. These lenders evaluate the startup’s financial health, business model, growth potential, and investor backing to determine eligibility, loan amount, and terms.

The capital is usually provided as a term loan or line of credit, with the loan size often capped at 30% of the last equity round.

The loan term generally spans 1 to 3 years and is often structured as interest-only payments initially, followed by principal repayment. Interest rates are tied to benchmarks like the prime rate, with an added margin.

Beyond capital, venture debt lenders often provide strategic support, offering operational guidance or connecting founders with key resources. The startup, in return, must adhere to the agreed terms, including covenants or reporting requirements, and ensure timely repayments over the loan's 1–3 year term.

Unlike traditional loans, venture debt decisions focus less on profitability or collateral and more on the startup’s growth trajectory, existing investor backing, and business fundamentals.

Venture debt is uniquely designed to meet the needs of high-growth startups, setting it apart from traditional financing options. Unlike conventional bank loans, which require substantial collateral and consistent positive cash flow, venture debt lenders focus primarily on the startup’s growth potential and recent venture capital backing. This makes venture debt accessible to companies that may not yet have significant assets or steady revenue but have strong investor confidence.

Another difference is the risk and return profile. Traditional loans are repaid with fixed interest, and lenders usually have no claim to the company’s equity upside. In contrast, venture debt often includes warrants or equity kickers, giving lenders a potential stake in the company’s future success. This hybrid approach balances the lender’s risk with the startup’s growth prospects.

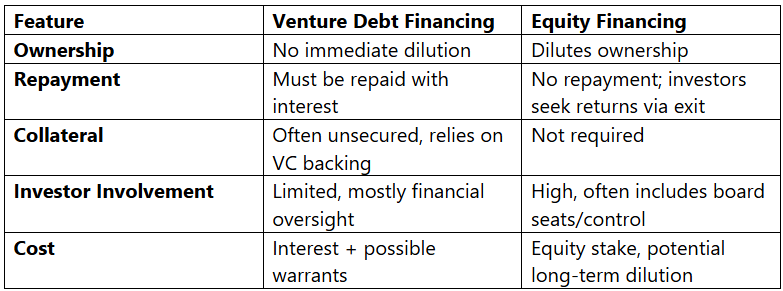

Compared to equity financing, venture debt does not immediately dilute ownership, enabling founders and early investors to retain control. Equity investors, however, take an ownership stake and often seek active involvement in company decisions. Venture debt lenders typically have limited influence beyond financial oversight, making it a less intrusive form of capital.

Lastly, venture debt is generally used as a complementary tool alongside equity rounds, providing additional runway and flexibility without the complexities of negotiating new ownership stakes. This strategic positioning makes venture debt a valuable option for startups looking to optimize their capital structure while minimizing dilution.

The primary advantage of venture debt lies in its non-dilutive nature, allowing founders and existing shareholders to retain ownership percentages while accessing growth capital. This preservation of equity becomes increasingly valuable as companies mature and their valuations appreciate, potentially saving millions in dilution costs compared to raising equivalent amounts through equity financing.

Venture debt extends cash runway significantly, providing companies with additional time to achieve key milestones, weather market uncertainties, or bridge between equity funding rounds. This extended runway can be critical for startups operating in competitive markets where timing and execution speed determine success.

The flexibility offered by venture debt enables companies to pursue aggressive growth strategies without the immediate pressure of raising equity at potentially unfavorable valuations. During market downturns or periods of reduced investor appetite, venture debt provides alternative access to capital that can maintain growth momentum while waiting for more favorable equity market conditions.

Venture debt can often be secured more quickly than traditional loans because it involves less stringent collateral requirements, allowing startups to access funds with greater speed and flexibility.

Despite its benefits, venture debt comes with notable risks:

1. Repayment Obligation: Unlike equity, venture debt must be repaid regardless of business performance, increasing financial pressure.

2. Shorter Terms: Repayment periods are typically shorter than traditional loans, requiring careful cash flow management.

3. Higher Interest Rates: Rates are generally higher than bank loans due to the perceived risk.

4. Potential for Default: Missing covenants or failing to meet milestones can trigger penalties or default, jeopardizing company assets or future fundraising.

5. Warrants: Lenders may receive rights to purchase equity at a discount, leading to some dilution if exercised.

Review the key terms of the debt facility, including interest rates, repayment schedules, warrant coverage, and financial covenants. These terms directly affect both your near-term cash flow and long-term ownership. A well-negotiated term sheet balances flexibility with financial discipline.

Venture debt introduces fixed repayment obligations. Assess your projected cash flow carefully to ensure the business can meet interest and principal payments without compromising operations or strategic initiatives.

Debt should fund initiatives that clearly advance business milestones—whether it’s extending runway, accelerating go-to-market execution, or bridging to the next funding round. Avoid using debt to cover structural cash burn or unresolved business model risks.

Align with your existing equity investors before proceeding. Venture debt adds leverage and introduces new rights and preferences that may impact future funding or exit scenarios. Investor support can also strengthen lender confidence.

Select a lender with experience in your stage and sector, and a strong reputation for working constructively with high-growth companies. A collaborative, flexible lending partner can add significant strategic value beyond capital.

Venture debt is a strategic financing tool for VC-backed startups seeking to extend runway, fund growth initiatives, or bridge to a future round—without significant dilution. It offers a more cost-efficient alternative to equity when used strategically, especially in capital-efficient business models with clear growth visibility.

However, unlike equity, it introduces fixed repayment obligations, interest costs, and covenants that may limit operational flexibility. Founders must carefully assess their company’s stage, cash flow predictability, and strategic roadmap before taking on debt.

When thoughtfully structured and aligned with near-term milestones, venture debt can enhance financial agility and position the company for stronger valuation in future equity rounds. But it must be approached with discipline, strong investor alignment, and a clear plan for repayment—especially in volatile or uncertain markets.

Startups that have recently secured or are currently in the process of securing funding from well-known venture capital firms usually qualify. Lenders look for strong investor backing, a scalable business model, and a clear plan for growth.

Venture debt is tailored for high-growth, VC-backed startups with higher interest, warrants, and flexible terms. Traditional loans depend on cash flow and collateral, with stricter covenants and lower rates.

-min.png)