Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Designing a Phantom Option Plan for an NBFC

As a startup founder, you must navigate a complex landscape of federal regulations when issuing equity. These regulations help ensure fairness and prevent fraud; however, they can also be time-consuming and challenging to understand. This is where Rule 701 becomes invaluable.

Rule 701, an exemption under the Securities Act of 1933, allows you to offer equity-based compensation to your employees, consultants, and advisors without the need for extensive registration requirements. By avoiding the guidelines typically associated with public securities offerings, you can save time, reduce costs, and avoid potential legal challenges.

This blog explores the specifics of Rule 701, including its purpose, compliance guidelines, implications for startups, challenges and more. Read on!

Rule 701 is a federal safe harbor exemption that allows eligible private companies, including foreign private issuers, to issue equity compensation without the need for full registration with the SEC. This exemption covers stock options, RSUs, and other equity grants made to employees, consultants, advisors, and other eligible parties who provide bona fide services to the company. Notably, this includes individuals like insurance agents, general partners, and former employees who were part of the company's workforce.

This exemption also covers equity grants made to consultants and advisors. They must be natural persons and offer bona fide services to the business and its subsidiaries. Rule 701 permits eligible private companies to issue up to $10 million worth of equity compensation to employees without requiring extensive disclosures. For issuances exceeding this threshold, additional information such as financial statements and risk factors, must be provided to recipients within a reasonable period of time.

This section facilitates equity-based compensation as a means of attracting and retaining talent without the full costs and complexities associated with public offerings. This rule is particularly beneficial for smaller companies and small businesses that aim to offer competitive compensation packages.

The Securities Act of 1933 specifies that companies must register any securities offered or sold to the public with the Securities and Exchange Commission (SEC). This registration process ensures that investors receive crucial information about the company's finances and allows the SEC to review the company's disclosures. However, registering securities and preparing investor disclosures can be expensive and time-consuming. Recognizing this and the unique nature of equity compensation for employees, the SEC created Rule 701.

Under Rule 701, only private companies that are not covered under the reporting requirements of section 13 or 15(d) of the Securities Exchange Act of 1934 can issue stock options. However, the issuer of the securities should not be required to be registered under the Investment Company Act of 1940. The rule applies to various types of equity compensation, including stock options, Restricted Stock Units (RSUs), and other equity awards.

There are specific limits imposed by Rule 701. The total value of such securities issued in a 12-month period must not be more than the highest value of the following, as of last fiscal year end:

If a company exceeds $10 million in securities issued within a 12-month period, it must provide additional disclosures to the recipients, including financial statements and risk factors. Affiliates of the issuer subject to the provisions of the rule may not use this section for option grant or to sell securities.

To calculate the amount of securities that can be issued under Rule 701, companies must consider the total value of all equity awards granted in the past 12 months, including the sum of all cash and non-cash components.

If your company issues securities worth over $10 million within 12 months, you must provide additional disclosures to the recipients. These disclosure obligations include:

1. Financial Statements: You must provide the most recent financial statements of the company. These statements should be in line with the Generally Accepted Accounting Principles (GAAP). They must include financial reports like annual income statements, balance sheets, and cash flow statements. The financial records must be dated no more than 180 days before the date of sale of securities.

2. Risk Factors: You need to disclose any material risks associated with the sales of securities. This includes potential risks related to the company's business operations, financial condition, industry, and market environment. Providing a comprehensive list of risk factors helps recipients make informed decisions about their equity compensation. The financial statements required in an offering statement on Form 1-A22 under Regulation A must also be disclosed.

3. Plan Information: You must provide a copy of the equity compensation plan or a summary of its terms, known as the copy of the summary plan description. This includes details about the sale of the securities, including types of equity awards offered, the eligibility criteria, and the vesting schedule. Understanding the written compensatory benefit plan is crucial for transparency and compliance.

4. Additional Information: Depending on the specific circumstances, you may need to provide additional information to comply with Rule 701 requirements. This could include details about the company's capitalization, recent transactions, and any other relevant information that could impact the value of the securities.

Adhering to these disclosure requirements is essential for maintaining compliance with Rule 701. Failure to provide the necessary disclosures can result in legal liabilities and potential penalties under the antifraud provisions of the federal securities laws.

Rule 701 uses a 12-month rolling window to calculate the total value of securities issued under the available exemption. This means that at any given point, you must consider the total value of securities issued in the preceding 12 months to determine compliance with the rule's limits.

The 12-month rolling window affects the timing and frequency of your equity offerings. Continuous monitoring of your issuances is required to ensure that you do not exceed the thresholds set by Rule 701. Exceeding the limits can trigger additional disclosure requirements and potential legal liabilities. By keeping track of your equity offerings, you can plan and time your issuances strategically to stay within the allowed limits.

Let's consider an example to understand how the 12-month rolling window works:

Suppose your startup issued $500,000 worth of stock options in January, $300,000 in April, and $400,000 in September. By December, the total value of securities issued in the past 12 months would be $1.2 million. Since this exceeds the $1 million threshold, you would need to provide additional disclosures to the recipients, such as financial statements and risk factors.

However, if you wait until February of the following year to issue more stock options, the $500,000 issued in January of the previous year would no longer be included in the 12-month calculation. This would bring the total value of securities issued within the new 12-month window to $700,000, allowing you to issue additional equity without initiating the disclosure requirements.

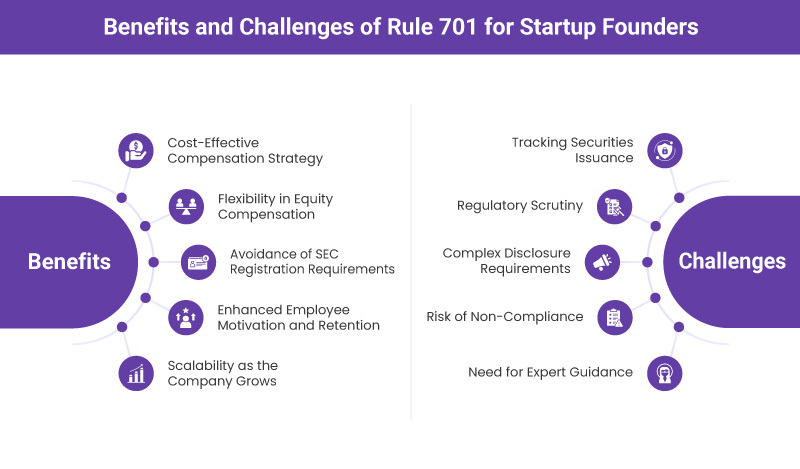

Rule 701 has significant implications for startup founders, offering both advantages and challenges. Understanding these can help you utilize the rule effectively to support your company's growth and success.

1. Cost-Effective Compensation Strategy: Rule 701 enables you to offer stock options and other equity awards as part of a compensation package without needing to register with the SEC. This helps you preserve cash while still offering interesting rewards to attract and retain top talent. By using equity as a form of compensation; you can incentivize your team without depleting your financial resources and avoiding the need for complex registration statements.

2. Flexibility in Equity Compensation: Rule 701 provides flexibility in structuring equity awards. You can issue options, restricted stock, or other types of equity without the complexity of regulatory filings. This is particularly beneficial for early-stage startups with limited resources, allowing you to tailor your equity compensation strategy to meet your specific needs and goals.

3. Avoidance of SEC Registration Requirements: Rule 701 allows you to bypass the costly and time-consuming process of registering securities with the SEC if you stay within the rule's limits. This exemption to conditions of this section significantly reduces administrative and financial burdens, enabling you to focus on growing your business rather than navigating complex regulatory requirements.

4. Enhanced Employee Motivation and Retention: Offering equity under Rule 701 can align employees' interests with the company's success. This is a powerful tool for retention, as employees are more likely to stay with a company where they hold equity. By providing a stake in the company's future, you can create a committed and motivated team.

5. Scalability as the Company Grows: Rule 701 is scalable and can accommodate the increasing equity needs of a growing company. As your startup expands and hires more employees, you can continue to use Rule 701 to offer employee stock options, keeping your compensation packages competitive. This scalability helps maintain an effective equity compensation strategy as your company evolves.

1. Tracking Securities Issuances: One of the primary challenges associated with Rule 701 is the need for accurate record-keeping. As a founder, you must carefully track the total value of securities issued to ensure you do not exceed the rule's limits, such as the $10 million threshold over 12 months. Accurate and up-to-date records are essential to maintain compliance and avoid triggering additional disclosure requirements.

2. Regulatory Scrutiny: Failing to comply with Rule 701's requirements can result in increased regulatory scrutiny. This could lead to penalties, enforcement actions, or the loss of the exemption, which could be costly and damaging to your company's reputation. Ensuring compliance with the rule is crucial to avoid these potential pitfalls.

3. Complex Disclosure Requirements: Meeting Rule 701's disclosure requirements can be challenging, especially when issuing securities that exceed $10 million in value over 12 months. You must prepare and provide detailed financial statements and risk disclosures, which can be complex and time-consuming.

4. Risk of Non-Compliance: Non-compliance with Rule 701 can have severe consequences, including fines, legal challenges, and the requirement to register securities retroactively. Additionally, non-compliance could lead to investor lawsuits and damage to your company's valuation. To mitigate these risks, it is essential to understand and adhere to the rule's requirements.

5. Need for Expert Guidance: Navigating the registration provisions of the Act and related securities laws within a reasonable time can be daunting. Seeking legal and financial advice is essential to a plan to ensure compliance with the rule. For instance, working with experts from Qapita can help ensure that your equity compensation strategy aligns with every applicable state law and federal regulatory requirement.

Failing to comply with Rule 701 can have significant legal and financial implications for your startup. Understanding these challenges is necessary to avoid potential pitfalls and ensure regulatory compliance.

Non-compliance with Rule 701 can lead to enforcement actions by the SEC, such as fines and other penalties on your company. These actions can prove to be costly, strain your resources and hinder your ability to grow and expand.

The SEC may also require you to register the securities retroactively, which can be a time-consuming and expensive process. Non-compliance with Rule 701 can also damage your company's reputation. Investors, employees, and other stakeholders may lose trust in your business if they perceive that you are not adhering to regulatory requirements. This loss of confidence can impact your ability to attract investment and retain top talent.

Failing to comply with Rule 701 can also result in legal challenges, including lawsuits from affected investors. These legal disputes can be costly and time-consuming, diverting your attention and resources away from core business operations.

Here are some steps to avoid the consequences of non-compliance with Rule 701, and adhere to the specified requirements:

1. Maintain Accurate Records: Keep updated records of all securities issuances to ensure you stay within the rule's limits.

2. Provide Required Disclosures: If you issue securities with a value of more than $10 million in a 12-month period, ensure that you provide the necessary disclosures, including financial statements and risk factors.

3. Seek Expert Guidance: Work with legal and financial experts who have experience with Rule 701 and securities law. They can help you navigate the complexities of the rule and ensure compliance.

4. Regular Compliance Reviews: Conduct regular compliance reviews to identify and resolve any issues before they become significant problems

Under Rule 701, your employees can receive various types of equity awards like stock options, RSUs, or performance shares.

By understanding how this rule works and the types of equity offerings available, your team members can make informed decisions to realize their financial goals. Here are some of the benefits your employees can avail with Rule 701:

1. Access to Equity Compensation: Rule 701 allows you to grant your employees different types of equity awards. This can be a good incentive to attract top talent and align their interests with your long-term success.

2. Financial Growth: Equity compensation can be a significant source of wealth creation, especially if your startup achieves its targets. By participating in the company's growth, your employees can take advantage of the appreciation in their equity holdings.

3. Tax Advantages: Rule 701 offers certain tax advantages for your company and its employees. For example, employees may be able to defer capital gains taxes on their equity compensation until they sell their shares.

Your employees must understand the terms and conditions associated with their equity offerings. This includes the vesting schedule, exercise price, and any potential tax implications.

Over time, Rule 701 has undergone significant changes to accommodate the needs of startups better. Let's explore some of the key amendments and their impact on equity compensation:

1. 2018 Amendment Overview: In 2018, a significant amendment to Rule 701 was mandated by the Economic Growth, Regulatory Relief, and Consumer Protection Act. This amendment was designed to accommodate the evolving needs of private companies, particularly startups that rely heavily on equity compensation. The change aimed to modernize the rule and make it relevant to the current business environment.

2. Increased Disclosure Threshold: The most notable change in the 2018 amendment was the increase in the threshold for mandatory disclosures under Rule 701(e) from $5 million to $10 million in any 12-month period. This change in the aggregate sales price allows private and public companies to issue securities without triggering strict disclosure requirements. In this context, the aggregate sales price includes the sum of all cash, property, notes, and cancellation of debt.

3. Impact on Startups: This amendment has particularly benefited startups by enabling them to allocate a larger amount of equity to employees and contributors without the burden of detailed disclosures. This has helped startups conserve resources and streamline their equity compensation processes, making it easier to attract and retain talent.

Understanding Rule 701 is crucial for effectively managing your startup's equity compensation strategy and ensuring compliance with regulatory requirements in the United States. At Qapita, we are providing services to founders to help manage their equity compensation plans and ensure compliance with Rule 701, securities exemptions like Regulation D, and the Employee Retirement Income Security Act of 1974.

Our platform offers comprehensive cap table and equity management tools, making it easier for you to issue stock options and other equity awards. We also provide expert guidance on navigating the complexities of securities law, helping you avoid potential legal pitfalls.

Rated as the #1 Equity Management Software by G2, we are committed to supporting your startup's growth by providing the tools and expertise you need to manage your equity compensation effectively.

Contact us today to learn more about how our experts can help manage your equity compensation plans and ensure compliance with Rule 701.