Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

In the extremely competitive startup ecosystem, securing the best talent is essential for driving growth. As many startups operate with limited funds, they turn to innovative strategies to compete with established companies. One such strategy is offering equity compensation, such as Employee Stock Purchase Plans (ESPP), to reward qualifying employees with a stake in the company's future success.

An ESPP is a program initiated by an enterprise that allows its employees to purchase the company stock at a discounted price. ESPPs create a beneficial scenario for both parties - startups can secure and retain high-quality talent without overextending their financial resources, while employees gain the chance to participate in the company's success.

With this blog, we will explore the essential aspects of Employee Stock Purchase Plans, including their types, working, benefits, tax implications, and others.

An Employee Stock Purchase Plan (ESPP) is a program that allows employees to become shareholders by purchasing the company's stock, usually at a price lower than the market rate.

Employees can participate in the plan by opting for payroll deductions. These deductions accumulate during the period between the offering date and the purchase date. Then, on the purchase date, the company uses these accumulated funds to buy stocks on behalf of the participating employees.

Just like a 401(k) plan for retirement savings, an ESPP is offered as an employment benefit. The primary goal is to enable employees to buy the company's valuable stock at a lower price, setting the stage for potential profits. As the company grows and becomes successful, the stock's value increases, enhancing the benefits for the employees.

The discount rate on company shares under an ESPP can vary, but it can go up to 15% lower than the market price. Some ESPPs also feature a 'look back' provision that allows the plan to consider a previous stock price. This could be the price on the offering date or the purchase date. As a result, employees can buy the stock at an even lower cost, making the plan more beneficial for them.

Here are the important ESPP dates that you, as a startup founder, need to be aware of:

The eligibility criteria for ESPPs can vary across companies, but there are some common factors that determine whether an employee can participate in an ESPP:

You can impose certain restrictions on eligibility to maximize benefits from ESPPs. For example, an employee might need to maintain a certain level of performance for a given duration, or your company may limit the number of shares an employee can purchase.

When an employee decides to participate in an ESPP, they choose a percentage of their salary to be deducted from each paycheck. This percentage ranges between 1% and 15%, but the precise value can differ based on your company's rules for such plans.

During the offering period, the deductions are accumulated. Once this period concludes on the purchase date, these collected funds are used to acquire company shares for the employees participating in the plan. The shares are bought at a price lower than the market rate, offering a potential financial advantage to the employees.

Understanding these deductions is crucial for your employees, as participating in an ESPP means committing a portion of their monthly salary for a considerable duration. Hence, employees must consider their personal goals to decide how much they can contribute to the plan.

Here is a step-by-step explanation of how ESPPs function:

Let's illustrate this process with an example. As a founder, you offer an ESPP for an important employee. The employee decides to enroll in the plan and starts contributing 10% of the salary. Over the six-month offering period, these deductions accumulate, and at the end of the offering period, you use these funds to purchase shares on the employee's behalf. The shares have been bought at a 15% discount from the market price, giving the employee an immediate return on their investment.

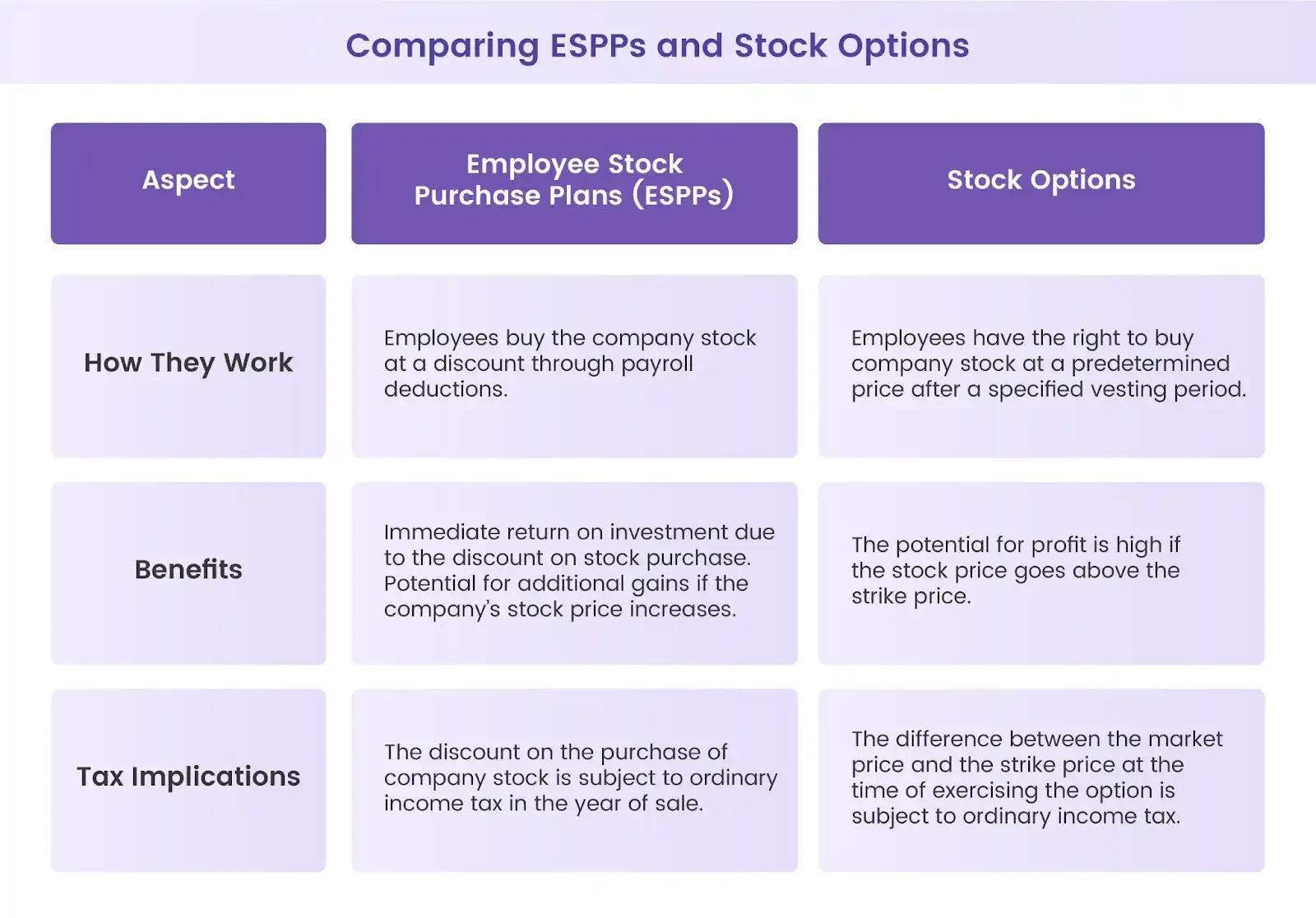

ESPPs and stock options may seem similar, but they are fundamentally different in how they work and in terms of benefits and tax implications.

Employee Stock Purchase Plans (ESPPs) can be broadly categorized into two types: Qualified ESPPs and Non-Qualified ESPPs. Here are important details related to both these options:

Qualified ESPPs are the most popular type of plan, and they must comply with certain criteria established by the Internal Revenue Service (IRS). For example, before they can be put into action, qualified plans must receive approval through a shareholder vote, and all participants in the plan have equal privileges. The duration of these plans' offering periods cannot go beyond 27 months, and the discount on the stock price is capped at 15%.

One of the key advantages of qualified ESPPs is the tax benefits they offer to employees. The discount received on the purchase of company stock is not taxable until the stock is sold. Any additional gain may be subject to capital gains tax.

On the other hand, Non-Qualified ESPPs do not meet the IRS criteria and offer higher flexibility in how a non-qualified plan can be designed. For example, they may offer a discount of more than 15% from the current Fair Market Value (FMV) of the stock.

However, non-qualified plans do not offer the same tax advantages as qualified plans. The discount received on the stock at purchase is taxed as ordinary income, whether or not the employee sells the stock in that calendar year.

ESPPs offer a range of benefits for both employees and employers. However, like any financial instrument, they also come with certain challenges.

As an employer offering ESPPs, it's important to understand that the tax treatment for ESPPs varies depending on whether they are qualified or non-qualified and on how long the employees hold the shares before selling.

In this case, employees typically do not incur taxes when they acquire the stock. Taxes come into play when they decide to sell, trade, or transfer their shares. The tax treatment depends on how long employees hold their shares:

Any additional profit between the purchase price and the sale price is subject to long-term capital gains tax.

Non-qualified ESPPs do not provide the same tax benefits. The discount received on the purchase of company stock, which is the difference between the market value and the purchase price, is treated as taxable income in the year of purchase. Any further profit made at the time of sale will be regarded as a capital gain and is taxed as such.

Understanding Employee Stock Purchase Plans (ESPPs) is crucial for you as a startup founder to make informed financial decisions and attract the best talent in the industry. However, managing ESPPs and other equity-related matters can be a complex task, and to streamline this process, you must partner with Qapita.

At Qapita, we are market leaders in automating workflows around equity processes for CapTables, ESOPs, Due Diligence, and Transactions. With in-house experts possessing multiple years of experience in equity management, Qapita offers a one-stop solution for all your equity management needs.

We have recently achieved an incredible milestone and have been named the #1 Equity Management Software Platform by customers on G2. This recognition is a testament to the remarkable satisfaction ratings their customers have given Qapita across all aspects of our platform and services.

Get in touch with our experts, and let's explore how we can help streamline your equity matters.

Employee Stock Purchase Plans (ESPPs) can be highly beneficial. They offer the opportunity to purchase company stock at a discounted price, typically up to 15% below market value. This built-in discount provides an immediate potential for profit, making ESPPs a valuable addition to the compensation package

A good percentage for an ESPP is usually the maximum allowed by the company, often 10-15% of an employee's salary. This maximizes the benefit of the discounted stock purchase. However, it's important for employees to consider their overall financial situation and ensure they are not overextending themselves here.

After leaving your job, you generally stop contributing to the ESPP. Any contributions made during the current offering period are typically refunded. You usually retain ownership of shares already purchased through the plan. However, specific rules can vary, so it is essential to review your company's ESPP policy.

Investing in an ESPP can be a smart financial move. The discounted purchase price offers an immediate potential return. However, it is important to consider it as part of your overall investment strategy. Ensure you are not overexposing yourself to your company's stock and maintain a diversified portfolio.

No, ESPP and SIP are different. An ESPP allows employees to purchase company stock at a discount. A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly in mutual funds. While both are investment tools, they operate differently and serve distinct purposes in financial planning.