Equity management

Equity management

Equity management

Equity management- Fund management

Fund management

Fund management - Fund managementFund management

- Fund managementFund management

Mutual Funds are a popular investment choice for people and contrary to popular perception, not all mutual funds are the same. Equity and debt funds are two primary types of investment funds. The key difference between equity and debt funds boils down to their investment target, that is where the money goes.

Investing can be challenging due to the range of options available. Investing feels like a high-stakes competition, where you need to choose the option with the best chance of success. Both equity funds and debt funds offer different avenues and possibilities for your money to grow.

Let's break down their strengths, weaknesses, and ideal investors to help you decide which fund aligns best with your financial goals.

Debt funds, also known as income funds, are investment options that prioritize stability and income generation. These funds primarily invest in debt instruments like government bonds, corporate bonds, and treasury bills, with less than 65% of their portfolio allocated to riskier equities (stocks).

Debt funds lend money to governments and companies through these securities, offering the potential to preserve your initial investment while generating regular interest income. This makes them suitable for investors seeking predictable returns and a steady stream of income, particularly for short- or long-term goals.

Taxes on debt fund returns in India depend on when you invested. If you made the investment before April 1, 2023, holding the units for over 3 years (long-term) offered a benefit of indexation that reduced taxable gains. However, this benefit has been removed for investments made after April 1, 2023. Now, regardless of the holding period, any capital gains from debt funds (both short-term within 3 years and long-term after 3 years) are simply added to your taxable income and subject to taxation at your standard income tax bracket.

Remember, debt funds don't involve any tax deduction at source (TDS) when you redeem your units.

Equity funds provide investors with the opportunity to own a diversified portfolio of companies by pooling capital. This pooled money is used to acquire shares in various listed companies. As these underlying companies grow and their stock values rise, the potential for the equity fund to generate significant returns increases.

However, equity funds are subject to market volatility, meaning their value can fluctuate substantially in response to changes in the broader stock market.

Equity funds provide everyday investors an accessible entry point to the stock market without requiring in-depth knowledge of individual stocks. By pooling funds, equity funds offer a convenient way for new investors to participate in the growth potential of publicly traded companies.

Selling units within a year (short-term) triggers a flat 15% tax on your gains, irrespective of your income tax bracket. This applies to all equity fund redemptions.

For long-term capital gains (LTCG), the tax treatment depends on when you invested: pre-April 1, 2018, enjoys complete exemption up to Rs. 1 lakh annually, while post-April 1, 2018, incurs a 10% tax on gains exceeding Rs. 1 lakh, without any inflation adjustment

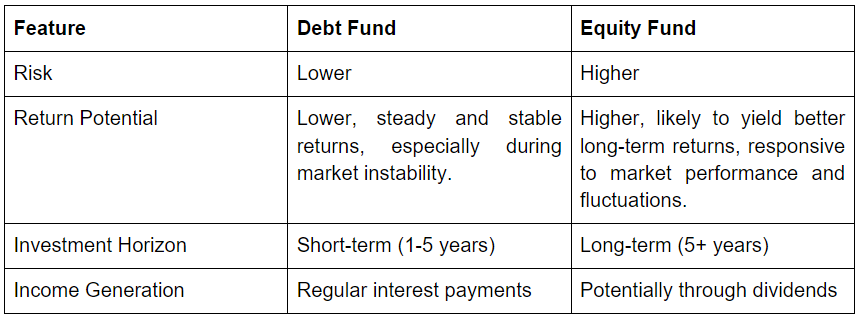

Choosing between equity and debt funds boils down to understanding your investment goals, risk tolerance, and investment horizon. Here's a detailed breakdown:

In conclusion, the decision between equity funds and debt funds hinges on the investor's individual financial goals, risk tolerance, and investment timeline. Equity funds offer the potential for higher returns by participating in the growth of publicly traded companies, while debt funds provide a more stable income stream through interest payments.

Investors should carefully assess their financial goals, such as capital appreciation or regular income, and align their investment strategy accordingly. A balanced portfolio that incorporates both equity and debt funds may offer diversification benefits and help mitigate overall risk.

It is strongly recommended that investors consult with a qualified financial advisor to develop a personalized investment plan. A professional can provide tailored guidance based on the investor's specific circumstances, risk tolerance, and long-term objectives.

Debt funds typically pay interest regularly, often monthly, quarterly, or semi-annually. The frequency depends on the specific fund scheme.

An exit load is a fee charged by the mutual fund house if you redeem your units (sell your investment) within a specific period from the purchase date. Some debt funds, especially short-term debt funds, may have exit loads if you redeem your units before a certain period. Always check the fund's exit load structure before investing.

Equity funds are typically recommended for long-term investment horizons (ideally 5+ years). This is because the stock market's ups and downs tend to even out over time, allowing you to ride out any short-term dips and potentially benefit from long-term growth.

Debt funds are generally safer and offer regular income, while equity funds have higher potential returns but are riskier. The choice between the two depends on your risk appetite and investment goals.