Equity management

Equity management

Companies

Companies- Fund management

Funds

Funds - Fund managementFund management

- Fund managementFund management

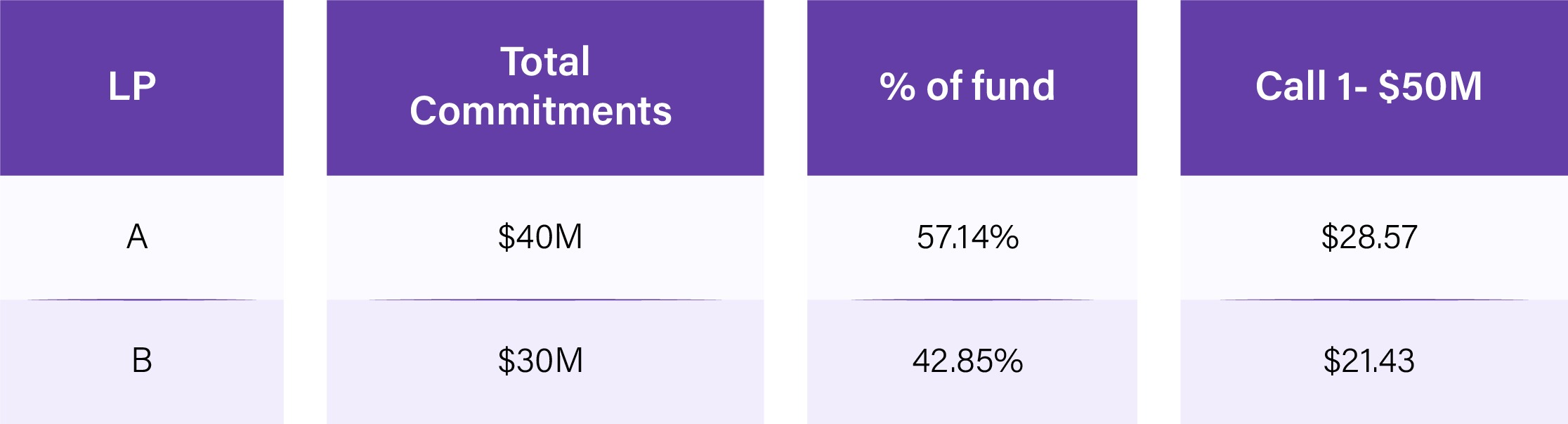

Imagine two investors commit to the same private equity fund. Investor A commits $50 million on January 1st. Investor B commits $50 million on July 1st, exactly six months later.

By July 1st, the fund has already deployed Investor A's capital. The portfolio has appreciated 10%. The fund is now worth $55 million.

Investor B arrives at this junction. Should they benefit immediately from the appreciation that Investor A funded and waited for? Or should the gains belong exclusively to Investor A for bearing the temporal risk?

Without adjustment, Investor B would receive the same ownership percentage as Investor A but would immediately benefit from six months of appreciated value they didn't finance. This is fundamentally inequitable.

Equalization is the mechanism that addresses this fairness issue. It ensures that regardless of when an LP commits to the fund, their economic exposure and return attribution remain equivalent. Early investors are compensated for the time value of their capital. Late investors pay for the privilege of joining an appreciated fund.

This blog explores equalization comprehensively: what it is, how it's calculated, why it matters, and how it protects both early and late investors through rigorous fairness mechanisms.

Private equity and venture capital funds are not static pools of capital. They are dynamic entities where capital is deployed sequentially over time, and returns accumulate continuously.

First Close: January 1, 2024 - $200M raised

At Second Close, the fund's deployed capital ($50M) is valued at approximately $57.5M (reflecting the 15% appreciation on Investment A and B).

The equity question: If Investor B (who committed in July) makes their first capital call alongside Investor A (who committed in January), should they:

The answer is: Investor B must effectively "catch up" to Investor A's position through equalization mechanisms.

When a subsequent-close investor joins a fund, three adjustments typically occur:

Rebalancing ensures that all investors, regardless of entry date, have contributed proportionally to all capital called to date.

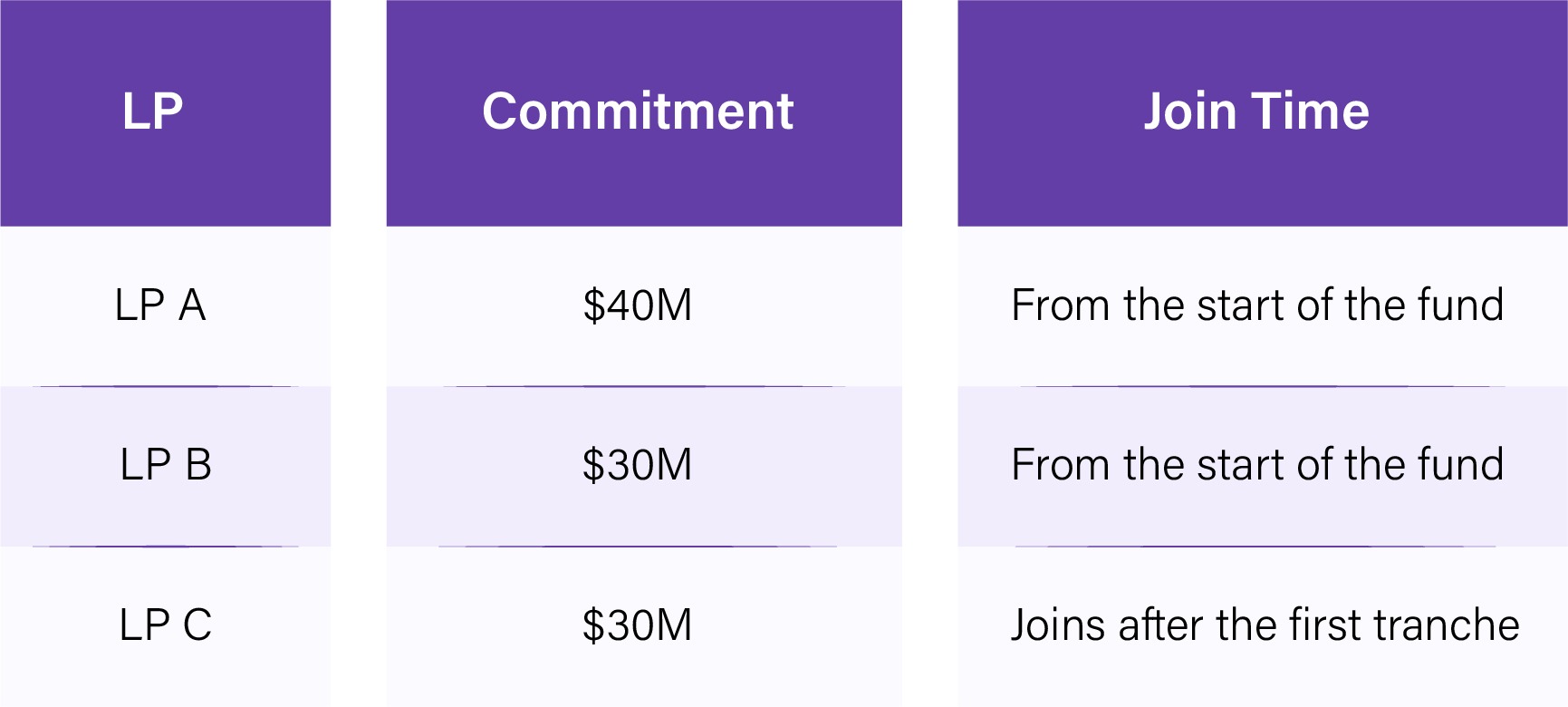

Fund Commitment: $100M total ($70M First Close + $30 M Second Close)

New LP ‘C’ has joined.

LP ‘C’ must bring 30M which contains cap call 1& 2.

LP ‘A’ & ‘B’ has already invested LP ‘C’ portion, so these amounts are adjusted in Capital Call #2.

This ensures Investor B has "caught up" to Investor A's capital contribution position.

Equalization alone is insufficient. Investor A deployed capital in February; Investor B deployed in July. Investor A's capital earned appreciation and returns for five months. Investor B is now participating in those gains without having funded them or borne the risk.

Equalization interest compensates Investor A for this time-value differential.

Equalization Interest = (Rebalancing Amount) × (Interest Rate) × (Days Between Calls / 365)

Equalization Amount: $15M, Interest Rate: 8% (typically specified in LPA); Days between: 150 days (approximately 5 months)

Equalization Interest = $15M × 8% × (150/365) = $15M × 8% × 0.411 = $493200

Investor B pays this $493,200 to Investor A (typically collected and distributed by the fund administrator).

The equalization interest rate is defined in the fund's LPA and typically equals:

Different fund types use different rates:

Higher rates reflect the riskiness and opportunity cost of earlier deployment.

Beyond capital contributions, subsequent-close investors must receive attribution adjustments for all profits and losses since fund inception, and this is a profit & loss true-up.

All profit and loss items allocated between inception and the subsequent close must be reallocated based on new ownership percentages.

Fund inception (January)

Investor A commits $50M, which is 100% ownership at inception.

Portfolio performance (January - June)

The portfolio earns $10M, giving 20% return on the $50M deployed.

Second close (July)

Investor B commits $50M. Ownership after B joins: 50% each.

The problem here is that investor ‘B’ missed out on the first $10M, even though their capital now represents 50% of the fund.

The true-up mechanism ensures that ownership percentage drives profit allocation, not chronological entry date.

Funds implement equalization through two main methodologies:

The most common approach in PE and VC funds.

Less common in PE/VC but used in some hedge funds and open-end structures.

The fund’s NAV is $20M

The Existing Investor A has invested $2M

New Investor B: $1M wants to join

The NAV per $1 of investment is equal to $20M ÷ $2M = $10 per $1 invested.

Investor B contributes $1M gets 1,00,000 units (1,000,000 ÷ 10)

An equalization account tracks that Investor B only participates in future gains, not the $20M already in the fund.

Fund grows to $25M, in which:

Investor A’s share = proportion of $20M grew to $25M.

Investor B’s share = proportion of growth after their entry, ensuring fair treatment.

Most PE and VC funds use interest-based equalization due to its clarity and alignment with traditional fund structures.

For a fund administrator or GP calculating equalization for a subsequent close, here's the systematic approach:

Step 1: Identify all capital called to date

Sum every capital call issued since fund inception.

Step 2: Calculate each investor's proportional share of called capital

For each investor (early and new), calculate: (Investor's commitment % of total commitments) × (Total capital called)

Step 3: Determine the catch-up amount (Rebalancing)

For new investors: Total called - what they've already paid = catch-up amount

Step 4: Calculate equalization interest

Use the formula: (Catch-up Amount) × (Rate) × (Time) / 365

Step 5: Account for multiple capital calls

If multiple capital calls occurred between closes, calculate equalization interest on each call separately (because each was called at a different time).

Step 6: Adjust for interim returns

If fund performance generated gains between calls, implement P&L true-up based on new ownership percentages.

This is complex and typically automated by fund administrators (Carta, Allvue).

Step 7: Net equalization against first subsequent-close capital call

Rather than requiring a separate equalization payment, most funds net this against the first capital call from the investor closing subsequent.

Equalization is theoretically straightforward but practically complex. Common disputes arise from:

Dispute: What interest rate should apply?

If the LPA specifies an 8% preferred return but market rates are 4%, first-close investors argue for 8%. Subsequent-close investors argue for 4%.

Resolution: The LPA should specify the interest rate methodology with precision. Most sophisticated funds use a fixed rate (e.g., "8% fixed") to eliminate ambiguity.

Dispute: How are "days between calls" calculated?

The industry uses several conventions:

Resolution: The LPA should specify the day count method. Most use Actual/365.

Example of variation:

The difference appears small but compounds across large funds and multiple calls.

Dispute: Should equalization include all profits, or only certain profit categories?

Some LPs argue that subsequent investors should not pay for future carry allocations they haven't participated in.

Resolution: LPAs typically specify. Common structures:

Option A: Full equalization (all profits since inception)

Option B: Partial equalization (only investment returns, not carried interest)

Option C: No equalization into certain profit lines (some funds don't equalize management fee savings)

Dispute: How do equalization calculations cascade through multiple subsequent closes?

Each new investor must catch up on all prior calls but also must account for previous subsequent-close investors' positions.

Example:

The third-close investor must equalize on capital called Months 1-12. But the second-close investor must receive equalization interest on the third-close investor's catch-up payment, further complicating calculations.

Resolution: Sophisticated fund administrators implement cascading equalization formulas that track ownership transitions across multiple closes.

Dispute: If a portfolio company exits between first and second close, should subsequent-close investors participate in those gains, or only in unrealized appreciation?

Different LPAs approach this differently:

Some funds treat exits as distributions and allocate to early investors. Others allocate based on ultimate ownership percentages.

Resolution: The LPA should explicitly specify treatment of interim exits.

Equalization serves multiple critical functions:

Without equalization, early investors bear all deployment risk with no explicit compensation. They fund capital when the fund's trajectory is uncertain. If the portfolio performs poorly, they absorb losses. If it performs well, late investors benefit immediately.

Equalization interest explicitly recognizes and compensates this risk.

Economic impact: On a $10M catch-up with 8% equalization interest over 6 months, the early investor receives $400,000 in direct compensation. This properly reflects the economic cost of earlier capital deployment.

Without equalization, subsequent-close investors would simply wire capital and immediately benefit from accumulated gains. This creates incentive for LPs to join late (minimum risk, benefit from prior appreciation).

Equalization makes late entry costly (you must pay for the privilege), which preserves fund economics for early committed LPs. This incentivizes committed capital, not opportunistic capital.

Equalization with P&L true-up ensures that each investor's economic return is proportional to their ownership percentage, regardless of entry timing. This achieves horizontal equity all investors with equivalent ownership percentages receive equivalent economic returns.

Without this, a late investor with 10% ownership might receive 15% of returns due to timing advantages.

In funds without equalization, late investors are "free riders”. They commit capital but participate in returns generated by earlier capital. Equalization eliminates this by making late entry costly.

When LP secondary sales occur (an LP sells their interest to another investor mid-fund), equalization calculations determine the purchase price. The secondary buyer prices based on the equalization adjustment understanding that they'll catch up on prior capital calls and pay equalization interest.

Without equalization, secondary market pricing would be highly ambiguous.

Equalization affects how fund performance appears to different investor cohorts:

First-close investor IRR: Calculated from their initial commitment date

Second-close investor IRR: Calculated from their commitment date, but adjusted downward for equalization costs

Example:

This differential is economically justified but should be transparent.

TVPI is calculated identically for all investors (total value distributed and unrealized divided by capital paid). However, the timing of payments varies due to equalization.

Investors should account for this temporal difference when comparing TVPI across cohorts.

Sophisticated GPs implement equalization through these practices:

The LPA should define:

Example LPA language: "Equalization interest shall be charged on catch-up contributions at an annual rate of 8%, calculated on an Actual/365 day count basis. Interest shall be calculated on each capital call separately; from the date such call was made to the date the subsequent-close investor makes their proportional contribution."

Before a subsequent close, provide prospective LPs with:

This enables informed decision-making and reduces disputes post-close.

For funds with multiple subsequent closes, implement formulas that automatically cascade equalization calculations through each new close. This reduces manual error and ensures consistency.

Include equalization calculations in quarterly LP reporting. Show:

This transparency builds LP confidence in the fairness of the process.

Equalization is one of the most important yet least understood mechanisms in private fund accounting. It bridges the fundamental tension between early and late investors: early investors bear temporal risk and deserve explicit compensation; late investors benefit from proven track record but must pay for that privilege.

The mechanism itself is mathematically sound: rebalancing ensures equal capital contribution positions; equalization interest compensates for time-value; P&L true-up aligns returns with ultimate ownership.

Implementation complexity arises from multiple variables (interest rates, day counts, multiple closes, interim exits) that must be precisely specified in fund documentation and calculated by fund administrators.

For GPs: Implement equalization through the LPA with precision, use professional administration, and provide clear transparency to LPs. This builds trust and eliminates post-close disputes.

For LPs: Understand equalization before committing. Request detailed calculations before subsequent closes. Include equalization in your total-cost-of-ownership analysis. Recognize that equalization interest is not a penalty—it is the economic cost of timing optionality, correctly allocated between early and late investors.

For fund administrators: Implement cascading formulas, validate calculations through independent review, and provide detailed documentation in LP reporting. The operational rigor that equalization requires is worth the effort—it ensures fairness and builds institutional credibility.

When implemented rigorously and transparently, equalization achieves its objective it's designed to accomplish it, protects early investors from timing risk while enabling late investors to join at a price that accurately reflects the value they're entering. This creates a system where all investors, regardless of timing, are treated equitably.

Because this would be inequitable to early investors. Early investors funded and bore risk to generate current value. Late investors would immediately benefit without paying for that value creation. Equalization corrects this.

Yes. Equalization is separate from management fees. Late investors pay:

You can try, but sophisticated GPs will resist. The 8% rate reflects market standard and is aligned with preferred return hurdles. Negotiating below-market rates signals weak fund demand. However, if no appreciation has occurred between closes, equalization interest is lower (interest only accrues on the catch-up, not on gains).

Yes. Late investors pay management fees retroactively to the fund inception date, as if they had been committed from the beginning.

Hedge funds often use NAV-based equalization (share adjustment) rather than cash-based. They also have more frequent closures (sometimes monthly) which changes the complexity. PE and VC typically use interest-based equalization. Both achieve the same goal through different mechanisms.

Commit at first close if you believe in the fund. The equalization cost is the explicit economic cost of timing optionality. It reflects the value you would forego by waiting. If the fund performs well, the equalization cost is trivial relative to returns. If it performs poorly, you've avoided additional losses by waiting. The trade-off is intentional and fair.

-T.jpeg)