Equity management

Equity management

Companies

Companies- Fund management

Funds

Funds - Fund managementFund management

- Fund managementFund management

The valuation announced during a funding round and the amount stakeholders receive during an exit are often very different numbers. A startup exit is not a simple equity split between investors and founders. Once a company enters an acquisition, merger, or liquidation event, the distribution of proceeds follows a predefined order shaped by investor agreements, liquidation preferences, debt obligations, and shareholding rights.

Liquidation waterfall is a type of scenario modeling to estimate a payout for each individual investor upon a liquidation event. Naturally by having many different classes of shares, each with their own sets of unique rights and preferences, it results in an extremely complex task for your company to try and model it out efficiently and accurately.

For companies, it is simply not worth the time and effort to properly maintain their liquidation waterfall model till the time they absolutely require it, such as needing it for their next financing round. Thus, employees holding equity awards or existing investors find it hard to determine what is their payout till the company decides to commission their next liquidation waterfall.

In this article, we will understand what a liquidation waterfall is, how liquidation preferences work, and the different ways these structures can influence founder payouts, investor returns, and equity outcomes during a startup exit.

A liquidation waterfall is the order in which proceeds are distributed among stakeholders during a liquidation event such as an acquisition, merger, asset sale, or company shutdown. The term “waterfall” refers to how funds move sequentially across different stakeholders based on contractual rights and payout priority.

In most venture-backed startups, proceeds do not get distributed equally across all shareholders at the same time. Before founders or common shareholders receive payouts, obligations such as debt repayments, liquidation preferences, and investor rights are typically settled first. The remaining amount, if any, then flows down to common shareholders and stock option holders based on ownership structure.

The exact payout sequence depends on factors such as the following:

A liquidation preference is a contractual right that gives preferred shareholders priority over common shareholders during a liquidation event. It determines how much investors are entitled to receive before proceeds are distributed to founders, employees, or other common equity holders.

Liquidation preferences are commonly negotiated during venture capital funding rounds and are included in investment agreements or term sheets. Their primary purpose is to protect investor capital during low-value exits, distressed acquisitions, or company shutdowns.

The liquidation preference structure agreed upon during fundraising can directly influence how proceeds are distributed during an acquisition, merger, or liquidation event. These clauses determine investor payout priority, recovery amount, and participation rights before proceeds move to common shareholders.

Anti-dilution provisions can also adjust the conversion ratio, indirectly affecting the liquidation waterfall in down-round scenarios.

A liquidation multiple defines how much capital an investor is entitled to recover before common shareholders participate in the remaining proceeds.

The most common structure is a 1x liquidation preference, where investors can recover an amount equal to their original investment. Some agreements may include 2x or 3x liquidation multiples, particularly in high-risk or later-stage financing rounds.

For example, if an investor invests ₹20 crore with a 2x liquidation multiple, they may receive up to ₹40 crore before proceeds are distributed to common shareholders.

Higher liquidation multiples can significantly reduce founder and ESOP payouts during lower-value exits.

This structure determines whether investors participate in the remaining proceeds after recovering their liquidation preference amount.

Participating Liquidation Preference

Under a participating preference structure, investors:

This is often referred to as a “double-dip” structure because investors receive proceeds twice during the distribution process.

Non-Participating Liquidation Preference

Under a non-participating structure, investors must choose between:

Seniority determines the order in which different investors receive payouts during a liquidation event.

In startups with multiple funding rounds, certain investors may hold senior liquidation rights over others. Senior preferred shareholders recover proceeds before junior investors and common shareholders.

Common seniority structures include:

Capped participation places a limit on the total payout that participating preferred shareholders can receive. For example, an investor with a 3x cap may stop participating once the total proceeds received reach three times the original investment amount. This structure creates a balance between investor downside protection and founder payout preservation during larger exits.

A preference stack refers to the combined liquidation preferences accumulated across multiple funding rounds. As startups raise additional capital, each funding round may introduce new investor preference rights. Over time, these layered preferences can significantly affect how proceeds are distributed during an exit.

In low or moderate-value acquisitions, a large preference stack can result in the following:

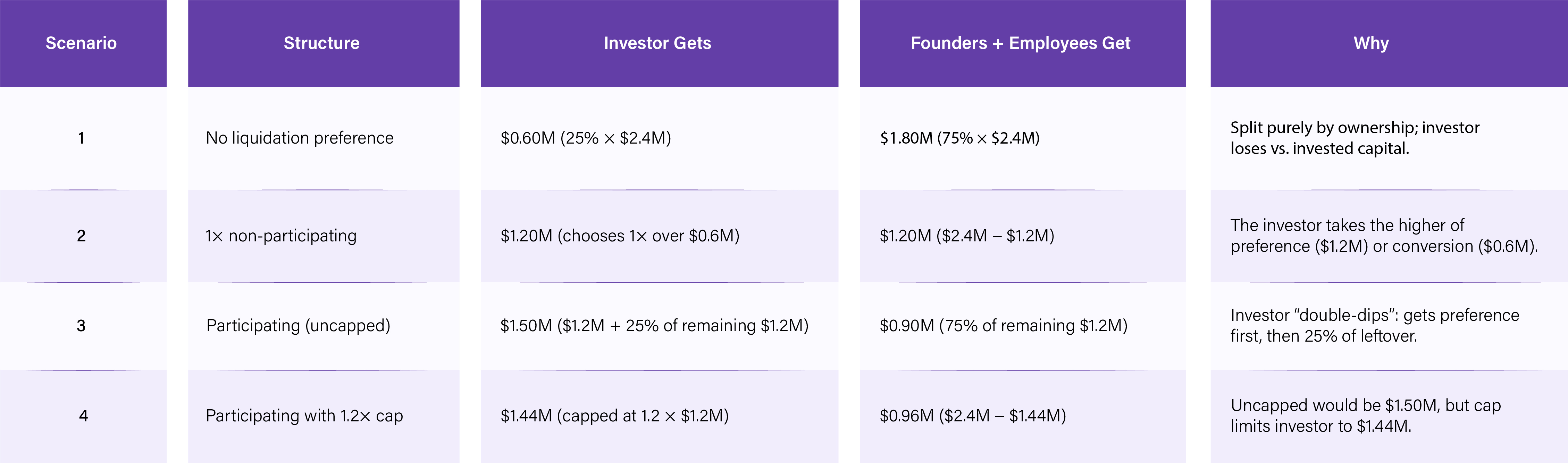

Assume an investor puts in $1.2 million for 25% of the company. Founders and employees own the remaining 75%. The company is later acquired for $2.4 million. Below are four common liquidation structures and the resulting payouts.

What this means:

A liquidation preference defines the investor’s payout rights during an exit or liquidation event. A liquidation waterfall refers to the sequence used to distribute proceeds among creditors, investors, founders, and employees.

The preference determines who gets paid first and how much they are entitled to receive. The waterfall shows how the remaining proceeds move across stakeholders after each obligation is settled.

A term sheet is a non-binding agreement that outlines the key terms of an investment before lawyers draft the final legal contracts. Think of it as the blueprint for your exit payouts: the liquidation multiple, participation rights, cap, and seniority rules are all negotiated here.

Once signed, these terms become part of the official legal documents (such as the charter and stock purchase agreement). At the time of an exit, you cannot renegotiate them, you must work with the terms that were agreed upon.

An investor converts preferred shares into common shares when the value from conversion is higher than the value from taking the liquidation preference. In simple terms, this decision depends on whether the exit price is high enough for an ownership-based payout to beat the fixed preference payout.

Also read: Preferred stock vs common stock: Understanding stock ownership options

A cap table waterfall is a model that shows how exit proceeds move through different stakeholder layers based on share classes, preferences, and rights. A liquidation waterfall is the actual payout order used during a liquidation or exit event.

Important points for liquidation waterfalls:

In startups, outcomes are shaped as much by structure as by success itself. A business can grow, scale, and reach an exit, and yet the distribution of that success can look entirely different depending on terms agreed upon years before the deal was ever on the table. The real economics of an exit are often determined long before the acquisition happens, through financing clauses that influence how value moves across stakeholders. Liquidation preferences, participation rights, and seniority structures do not wait until exit day to matter. They are already working in the background, shaping who benefits and by how much.

Understanding liquidation waterfalls is ultimately about understanding how ownership, risk, and negotiation intersect long before liquidity ever arrives. The founders and employees who navigate exits well are rarely the ones who got lucky. They are the ones who read the structure before they needed to.

At Qapita, we understand how complex liquidation events can be for founders, employees, and investors. Our cap table management platform gives you a single platform of truth for your ownership structure, models exit scenarios across share classes, and tracks how proceeds flow across stakeholders.

Trusted by 2,400+ companies across 60+ countries. Book a demo to learn more.

The liquidity waterfall approach is the method used to distribute proceeds from a liquidity event, such as an acquisition or merger, in a structured, sequential order. Proceeds first cover outstanding debts and obligations, then flow through investor liquidation preferences by seniority, and finally reach common shareholders and stock option holders with whatever remains.

The waterfall mechanism defines the exact payout sequence during a liquidation event. Proceeds are distributed tier by tier: secured creditors first, then preferred shareholders in seniority order (senior → pari passu → junior), then participating investors take their second dip if applicable, and common equity holders split what remains proportionally.

In an insolvency scenario, the waterfall follows a legally mandated order: secured creditors (banks, lenders) are paid first, followed by unsecured creditors, then preferred shareholders, and finally common shareholders. In most insolvency scenarios, common shareholders and equity holders receive nothing because proceeds are rarely sufficient to clear senior obligations.

List C refers to a category of contributories under Indian insolvency law, specifically those members who transferred shares within a defined period before winding up. They may be called upon to contribute to the company's assets if the current members cannot meet outstanding liabilities. This is distinct from the standard investor waterfall in a VC-backed startup exit.

Yes. Liquidation proceeds are generally subject to capital gains tax, with rates varying by jurisdiction and how long the shares were held. Equity holders typically face two tax events, one at exercise and one at sale. The transaction structure (asset sale vs. share sale) also affects tax treatment. Consult a local tax advisor for jurisdiction-specific guidance.